1031 Exchange Rules for Rental Properties: The Complete Investor Guide

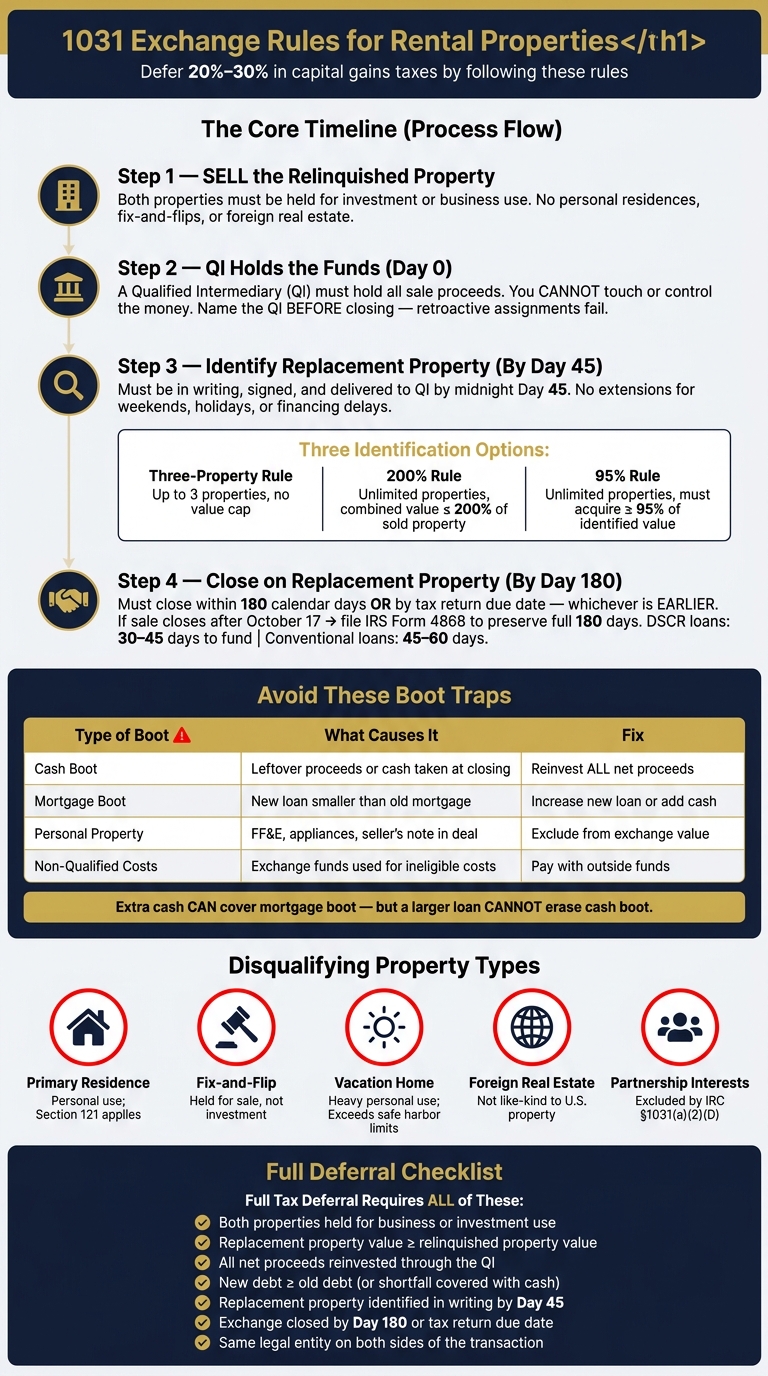

Sell a rental the normal way, and you could lose 20% to 30% of the gain to taxes. A 1031 exchange lets you defer that tax if you follow the IRS rules with care.

If I had to sum up the whole guide in a few lines, it would be this:

- Both properties must be held for investment or business use

- You have 45 days to identify and 180 days to close

- A Qualified Intermediary must hold the sale funds

- You must reinvest all net proceeds for full deferral

- Your new debt must match the old debt, or I need to add cash

- If I take cash, reduce debt, or mishandle title, part of the deal may become taxable

That’s the core issue. A 1031 exchange does not erase tax. It pushes tax into the next property. And if I keep exchanging over time, the deferred gain may stay deferred for years.

Here’s the short version of what matters most:

| Rule | What I need to know |

|---|---|

| Property use | Both the sold and bought property must be for investment or business |

| Like-kind | Most U.S. investment real estate can be exchanged for other U.S. investment real estate |

| Day 45 | I must identify replacement property in writing by midnight |

| Day 180 | I must close by the 180th day or my tax filing deadline, if earlier |

| QI | I cannot hold or control the sale money myself |

| Boot | Cash out, debt reduction, or non-real-estate value can trigger tax |

| Same taxpayer | The same legal owner generally must sell and buy |

The guide also covers where investors slip up: vacation homes with too much personal use, fix-and-flips, late identification, loan shortfalls, related-party deals, and closing costs paid the wrong way.

So if you want the plain answer: a 1031 exchange can keep more equity in play, but only if the property use, timing, money flow, debt, and title are all handled the right way.

1031 Exchange Rules: Step-by-Step Process for Rental Property Investors

How to Sell a Rental and Pay ZERO Taxes (1031 Exchange Step-by-Step)

Rule 1: Like-Kind and Investment-Use Standards for Rental Properties

For rental investors, the first thing to check is simple: do both properties count as investment real estate?

Before you worry about deadlines, a qualified intermediary, or loan details, both the property you sell and the one you buy need to meet the investment or business-use test. If they don't, the exchange doesn't work. After that, timing becomes the next hurdle.

What Counts as Like-Kind Real Estate

Most investors think "like-kind" means similar in style or quality. It doesn't.

It refers to the nature of the property, not whether one asset looks like the other. So a single-family rental can be like-kind to an apartment building, raw land, or even a commercial property. That's a lot broader than people expect.

You can also exchange into a Delaware Statutory Trust (DST) or Tenant-in-Common (TIC) interest. For 1031 purposes, those count as direct ownership of real estate.

There is one clear line you can't cross: U.S. real property is not like-kind to foreign real property under IRC §1031(h).

How the IRS Evaluates Investment Intent

Property type is only half the story. The IRS also cares about why you held the property.

Both the relinquished property and the replacement property must be held for business or investment use. That means not for personal enjoyment, and not for resale.

The IRS looks at the full picture, including lease history, operating records, your plans for the property, and how long you held it. There isn't a set minimum holding period in the statute. Still, 12 to 24 months is a common benchmark people use to help show investment intent.

If you bought the property mainly to resell it, the IRS may treat it as dealer property. If that happens, it won't qualify.

Properties That Do Not Qualify for a 1031 Exchange

Some property types are simply out, no matter how good the numbers look.

| Property Type | Qualifies? | Why Not |

|---|---|---|

| Primary residence | No | Personal use; Section 121 applies |

| Fix-and-flip | No | Held for sale, not investment |

| Vacation home (heavy personal use) | Conditional | Must meet safe harbor limits |

| Foreign real estate | No | U.S. real property is not like-kind to foreign real property |

| Partnership interests | No | Explicitly excluded by IRC §1031(a)(2)(D) |

Vacation homes qualify only under Rev. Proc. 2008-16. The property must be rented at fair market value for at least 14 days in each of the two prior 12-month periods. Personal use must also stay within the safe harbor limit: the greater of 14 days or 10% of rental days.

If the property clears this test, the exchange then shifts to the 45-day identification deadline and 180-day closing deadline. Once the investment-use rules are met, the next question is whether you identify and close on time.

Rule 2: Deadlines, Identification Rules, and Qualified Intermediary Requirements

Once the properties clear the investment-use test, the exchange comes down to two hard deadlines. After the relinquished property closes, the clock starts ticking: you get 45 days to identify replacement property and 180 days to close. At that point, success mostly comes down to timing and paperwork.

The 45-Day Identification Deadline and How to Meet It

You have 45 calendar days to identify replacement properties in writing, signed, and delivered to your QI by midnight on Day 45. The identification needs to be clear enough that there’s no confusion, so use a street address, legal description, or another exact identifier. And yes, the rule is strict. Weekends, holidays, and financing delays do not give you extra time.

The IRS gives you three ways to handle identification:

| Identification Rule | Number of Properties | Value Restriction |

|---|---|---|

| Three-Property Rule | Up to 3 | No cap on total value |

| 200% Rule | Unlimited | Combined value cannot exceed 200% of the relinquished property's value |

| 95% Rule | Unlimited | No value cap, but you must acquire at least 95% of the total identified value |

The Three-Property Rule is the one many investors use because it’s simple. You can list up to three possible replacement properties, with no limit on total value. And it gives you some breathing room. If your first deal falls apart during inspection or appraisal, you’re not left scrambling at the last minute.

After identification, the next pressure point is closing on time while also handling debt replacement and boot.

The 180-Day Closing Deadline and Tax Return Timing

You must close on the replacement property within 180 calendar days, or by your tax return due date, including extensions, whichever comes first. That last part trips people up all the time.

Here’s where it gets sneaky: if your rental sale closes after October 17, the normal April 15 tax deadline can shorten your 180-day exchange window. The usual fix is simple: file IRS Form 4868 so you can keep the full 180 days.

Why a Qualified Intermediary Is Required

A Qualified Intermediary, or QI, is required because you can’t take control of the sale proceeds yourself. The sequence is pretty direct: the sale closes, the QI holds the funds, you identify the replacement property, and then you close before the deadline.

One detail matters a lot here: name the QI before closing. You can’t patch this up after the fact, and retroactive assignments fail. Also, the QI can’t be someone who acted as your agent during the last two years, so your current attorney, CPA, or agent is off the table.

Once the QI is in place and the deadlines are under control, the next issue is taxable boot.

sbb-itb-e7c549b

Rule 3: Boot, Debt Replacement, and Mistakes That Trigger Tax

Once you meet the deadlines, boot becomes the main tax trap.

What Taxable Boot Means in a Rental Property Exchange

Boot is any non-like-kind value you receive. Put simply, if part of the deal gives you something other than qualifying real property, that piece can be taxed.

Gain is recognized to the extent of boot received, up to your total realized gain. Common examples include:

- Cash you pocket at closing

- Leftover sale proceeds held by the Qualified Intermediary that aren't reinvested

- Debt relief when the replacement mortgage is smaller than the relinquished mortgage

- Non-real property such as FF&E, appliances, or a seller's note

Only real property qualifies for 1031 treatment, so receiving personal property can trigger taxable boot at fair market value.

Boot is taxed first as depreciation recapture, then as capital gain. NIIT may also apply.

Debt replacement is the next spot where investors often lose deferral.

How to Avoid Boot When Buying the Replacement Property

To fully defer gain, the replacement property must be equal to or greater than the relinquished property's value, debt, and proceeds.

If the replacement debt is lower, the shortfall becomes taxable unless you add cash or increase financing. Any shortfall on value, debt, or proceeds is boot.

| Type of Boot | What Causes It | Practical Fix |

|---|---|---|

| Cash Boot | Leftover proceeds or cash taken at closing | Reinvest all net proceeds into the replacement property |

| Mortgage Boot | New loan is smaller than the old mortgage payoff | Increase the new loan amount or add fresh cash to the purchase |

| Personal Property | FF&E, appliances, or a seller's note included in the deal | Exclude personal property from the exchange value |

| Non-Qualified Costs | Using exchange funds for ineligible costs | Pay those costs with outside funds, not exchange equity |

Here's the key point: extra cash can cover mortgage boot, but a larger loan cannot erase cash boot.

Mistakes That Can Disqualify a 1031 Exchange

Even when the exchange looks fine on paper, title, funds, or related-party errors can blow it up.

Taking constructive receipt of sale proceeds triggers immediate tax. If sale proceeds land in your personal account, even for a moment, the IRS treats it as constructive receipt and the full gain becomes taxable right away.

The same taxpayer must hold both titles. If a different entity takes title to one side of the exchange, the deal can be voided.

Related-party deals can fail too. Under IRC §1031(f), both parties must hold the properties for at least two years.

Applying 1031 Rules to Real Investment Decisions and Financing

Once the rules make sense, the next step is putting them to work. That usually comes down to three goals: improving cash flow, cutting down on management headaches, or changing how debt sits across the portfolio.

How Investors Use 1031 Exchanges to Reposition a Rental Portfolio

A 1031 exchange lets investors move equity from one property to another without giving up tax deferral. One of the most common plays is to scale up. For example, someone selling a single-family rental might exchange into a duplex, triplex, or small apartment building, as long as both the old and new properties are held for investment.

Investors also use exchanges to shift into markets that better fit their numbers. One California investor sold a $2 million multifamily property and exchanged into two Arizona single-family rentals, increasing net monthly rent while significantly reducing annual property taxes.

Another common move is consolidation. If an investor owns several scattered rentals, exchanging into one larger asset can make life easier. Fewer roofs, fewer addresses, fewer moving parts. It can also improve unit economics. That said, the replacement property still has to meet the investment-use rules and work with the financing plan.

For investors who want less day-to-day involvement, a Delaware Statutory Trust (DST) can offer a passive path that still fits within a compliant exchange. Under Revenue Ruling 2004-86, a DST qualifies as like-kind replacement property. A DST can cut management work and close fast when timing gets tight, which makes it a solid backup if a main financed purchase starts to wobble near the deadline.

After the replacement property is lined up, financing becomes the next pressure point.

Coordinating Financing So Debt Replacement Does Not Create Boot

Financing is not a side issue in a 1031 exchange. It is part of the deal itself.

DSCR lenders usually need 30 to 45 days to fund, while conventional investment loans often take 45 to 60 days. That means the practical timeline can feel much shorter than the full 180 days. Investors may have less room than they think to find the property, get it under contract, and close.

To keep full tax deferral in place, the replacement loan has to cover the debt being given up. If it doesn't, the gap can create boot. That's why it helps to work backward from the 180-day deadline when building the financing schedule. In plain English: don't wait until the last minute to talk to a lender.

A cleaner approach looks like this:

- Start the lending process before the relinquished property closes

- Confirm the new loan amount will cover the prior mortgage balance

- Build in time for underwriting, appraisal, and closing delays

If the main purchase falls apart late in the exchange window, a DST that was identified early may close fast enough to keep the exchange alive.

Using LoanGuys.com for 1031 Replacement Property Financing

Debt replacement is often the toughest part of a 1031 exchange for self-employed investors, retirees, and borrowers whose tax returns don't show their full financial picture. That's where many deals get stuck, especially when the clock is ticking.

LoanGuys.com qualifies replacement property purchases based on the property's rental income and the borrower's credit profile, not pay stubs or W-2s. With closings in as little as 14 business days and 4,000+ funded loans, LoanGuys.com is built for the speed and flexibility a 1031 replacement purchase demands.

Conclusion: The Core 1031 Rules Rental Investors Must Get Right

A compliant 1031 exchange works ONLY when both properties are U.S. real estate held for investment or business use. Personal residences and fix-and-flip properties don't qualify.

The timing rules are strict. You must identify the replacement property by Day 45 and close by Day 180 - or by your tax return due date if that comes first.

The money can't pass through your hands. A Qualified Intermediary (QI) has to hold the sale proceeds, and you can't receive or control those funds at any point in the exchange.

If you want full tax deferral, you need to reinvest all net proceeds and replace the old debt with equal or greater debt. If the new loan comes up short, you'll need to add cash to make up the gap.

Use this checklist before closing:

| Rule | Requirement for Full Deferral |

|---|---|

| Property Use | Both properties must be held for business or investment use |

| Property Value | Replacement must be equal to or greater than the relinquished property |

| Equity/Cash | All net proceeds from the sale must be reinvested through the QI |

| Debt/Mortgage | New debt must replace the old debt, or any shortfall offset with cash |

| Identification | Must be in writing and delivered to the QI by midnight of Day 45 |

| Closing | Must be completed by Day 180 or the tax return due date, whichever is earlier |

| Same Legal Entity | The legal entity selling must be the same entity buying |

When the rules and financing line up, the exchange keeps more equity working in your next property instead of losing part of it to taxes.

FAQs

How long should I hold a rental before a 1031 exchange?

Section 1031 doesn't set a fixed holding period. But the IRS does require you to hold the property for investment or business use, not for resale.

That distinction matters. The IRS looks at your intent, and it judges that intent based on the facts and circumstances. So while there's no hard deadline written into the rule, the safer move is to hold the property for at least one to two years.

Why does that matter? Because a longer hold can help show that you bought and kept the property as an investment. That can come through in your rental activity, your records, and your tax filings.

Can I move into the replacement property later?

Generally, no - not right away. For a 1031 exchange to qualify, the replacement property must be held for investment or business use.

If you move into that property and treat it as your main home, you could put the exchange’s tax-deferred status at risk. There’s no fixed IRS holding period, but the IRS does expect a good-faith intent to hold the property for investment or business purposes.

What closing costs can I pay without creating boot?

To avoid taxable boot, use exchange proceeds only for costs tied directly to the sale of the relinquished property or the purchase of the replacement property.

These costs usually include:

- Broker commissions

- Qualified intermediary fees

- Escrow fees

- Transfer taxes

- Title insurance

- Recording fees

- Transaction-related attorney’s fees

Don’t use exchange funds for financing costs. That includes appraisal fees, loan origination fees, mortgage insurance premiums, and prepaid interest.

Also be careful with rent or tax prorations. In some cases, they can be treated as taxable cash distributions.