DSCR Loan for Multifamily Properties: What Every Investor Should Know

If the rent can cover the payment, a DSCR loan may work even when your tax returns do not. For 2–4 unit rentals, lenders usually size the deal off gross rent ÷ PITIA, and many want at least 1.00x DSCR, about 25% down, 620–660+ FICO, and 3–12 months of reserves.

Here’s the short version:

- DSCR loans focus on property income, not your W-2s or tax returns

- For duplexes, triplexes, and fourplexes, lenders often use gross monthly rent ÷ PITIA

- Many lenders use the lower of lease rent or appraised market rent

- Common caps are about 75% LTV on purchases and 65%–70% LTV on cash-out refis

- Cash-out deals often need 1.10x to 1.25x DSCR

- 2–4 unit rates are often a bit higher than single-family rental DSCR rates

- Late issues often come from low DSCR, high post-close taxes, weak reserves, bad property condition, or unit-count problems

If I were screening a deal fast, I’d check these first:

- Can the property hit at least 1.00x to 1.25x DSCR?

- Will the deal still work if I use higher taxes after closing?

- Do I have enough cash for the down payment, closing costs, and reserves?

- Are the rents supported by leases and the appraisal?

- Is the property rent-ready and legally the same unit count shown on the rent roll?

DSCR Loans for 2-4 Units

sbb-itb-e7c549b

Quick Comparison

| Item | 2–4 Unit DSCR Loan |

|---|---|

| Main approval test | Gross rent ÷ PITIA |

| Common minimum DSCR | 1.00x |

| Best pricing tier | 1.25x+ |

| Purchase LTV | Up to 75% |

| Cash-out refinance LTV | About 65%–70% |

| Credit score range | 620–660+ minimum in many programs |

| Reserves | 3–12 months of PITIA |

| Income docs | Often no tax returns or W-2s |

| Common closing timeline | 21–30 days |

| Main tradeoffs | Higher rates, lower leverage, prepay penalties |

Bottom line: I’d use a multifamily DSCR loan when the property cash flow is solid, but my personal income paperwork makes a bank loan hard. It can be a good fit for buying, refinancing, or pulling out cash - as long as the numbers still hold up after a tougher rent and tax check.

DSCR Basics for 2–4 Unit and Small Multifamily Properties

The DSCR Formula and How to Calculate It

With small multifamily, the math is pretty simple. For 2–4 unit rentals, DSCR usually equals gross monthly rent ÷ PITIA.

PITIA means Principal, Interest, Taxes, Insurance, and Association dues (HOA). So if a fourplex brings in $4,800 in gross monthly rent and the PITIA is $3,600, the DSCR comes out to 1.33. In plain English, the property brings in $1.33 in rent for every $1.00 of debt service.

What Lenders Count as Income on a Multifamily DSCR Loan

Once you know the formula, the next step is figuring out which rent number the lender will use. In most cases, lenders use the lower of:

- Signed lease rent

- Appraised market rent

That lower figure is the one that counts.

For vacant units, lenders use projected market rent and may apply a 5%–10% vacancy factor. Documented ancillary income, like parking or laundry, may also count.

How Multifamily DSCR Standards Differ from Single-Family Rentals

Compared with single-family rentals, 2–4 unit DSCR loans often come with a 0.125%–0.375% higher interest rate for the same borrower profile. They also usually have lower LTV caps.

But there’s a clear upside. A vacant unit in a fourplex cuts income by 25%, not 100% like a vacant single-family rental. That cushion matters.

| Metric | 2–4 Unit Multifamily |

|---|---|

| Formula | Gross Monthly Rent ÷ PITIA |

| Max LTV (Purchase) | 75% |

| Max LTV (Refinance) | 70% |

| Min. DSCR | 1.00 |

| Reserves | 3–12 months of PITIA |

| Appraisal Type | Residential income form |

Those coverage rules shape the credit, reserve, and leverage standards that come next.

Qualification Standards for Multifamily DSCR Loans

Minimum DSCR, Credit Score, and Reserve Requirements

Once you’ve worked out rent coverage, lenders usually look at three things: DSCR, credit score, and reserves.

For purchases, most lenders want at least 1.00x DSCR. For cash-out refinances, the bar is often higher at 1.10x to 1.25x. If you can get to 1.25x or more, you’ll usually qualify for the best pricing and the most leverage.

If the DSCR drops below 1.00x, some lenders still have low-DSCR options. But there’s a catch: you’ll often pay a 100 to 200 basis point rate premium. That same tiering also affects how much money you need to bring in.

| DSCR Value | Underwriting Tier |

|---|---|

| 1.25x+ | Strongest pricing / maximum leverage |

| 1.00x–1.24x | Standard pricing |

| Below 1.00x | Limited programs / higher cost |

DSCR, credit, and reserves shape both approval and pricing. Most loan programs start around 620 to 660 FICO. But better scores usually mean better terms. Borrowers in the 720 to 740+ range often get pricing that’s 25 to 75 basis points lower than a 660-score borrower on the same property.

Reserve rules usually call for 3 to 12 months of PITIA in liquid accounts. On larger loans above $1,000,000, lenders often want 6 to 12 months in reserves.

Down Payment, LTV, and Rate Factors

For 2–4 unit properties, expect to put down about 25%. That lines up with a 75% LTV cap on purchases. Cash-out refinances are usually tighter, with caps around 65% to 70% LTV.

Your rate mostly comes down to four factors:

- Credit score

- DSCR

- LTV

- Property type

Higher leverage and lower DSCR tend to push rates up. Credit matters a lot too. A borrower with a 760+ credit score may be about 75 basis points cheaper than a 660 borrower on the same property.

Documents Lenders Typically Request

After the ratio and leverage checks, lenders usually move to property-level paperwork. In many DSCR programs, personal tax returns and W-2s are not required. For a 2–4 unit deal, lenders often ask for:

- Appraisal with rent schedule or market rent survey

- Signed leases or rent roll

- Bank statements for reserves and funds

- LLC documents, EIN letter, and government-issued ID

One detail can trip people up: use projected post-close property taxes, not the seller’s current tax bill. If the property gets reassessed after closing, the higher tax bill can reduce DSCR.

Buying, Refinancing, and Scaling with a Multifamily DSCR Loan

Once the DSCR math is clear, the next step is knowing when to use this kind of loan to buy, refinance, or add more doors to your portfolio.

When a DSCR Loan Makes Sense for a Multifamily Purchase

A DSCR loan tends to make the most sense when the property looks strong on paper, but your tax returns do not. That happens a lot with real estate investors. Depreciation can cut taxable income, and the conventional 10-mortgage cap can shut the door on more financing. So even if the deal works, a lender using DTI may still say no because your tax returns don’t show the whole story.

For 2–4 unit properties, lenders usually underwrite the loan by dividing gross monthly rent by PITIA. In plain English, the property can qualify based on its own projected rental income instead of your personal tax returns.

How DSCR Refinances Work on Duplexes Through Fourplexes

Most investors refinance into a DSCR loan for one of two reasons:

- to improve loan terms

- to pull out equity for the next purchase

A rate-and-term refinance can cut the monthly payment or reset the loan terms. A cash-out refinance lets you tap equity and use that money for another duplex, triplex, or fourplex.

For cash-out refinances on 2–4 unit properties, LTV often falls between 65% and 75%. Lenders also tend to want at least 180 days of title seasoning. And cash-out rates usually come in 25 to 75 basis points above purchase rates. To support the file, lenders order a new 2–4 unit appraisal along with a rent schedule to verify projected rents.

That’s the tradeoff. Refinance rules are tighter, but the approval process is often faster and tied more to the property than to your personal income docs.

Growing a Rental Portfolio Without Tax Return Underwriting

One of the biggest draws of DSCR financing is that each property is judged on its own. Conventional loans often cap investors at 10 financed properties. DSCR loans, on the other hand, look at the asset’s cash flow instead of the borrower’s full debt-to-income picture.

Timing matters too. DSCR loans often close in 21 to 30 days, while agency debt can take 60 to 90 days. That shorter timeline, paired with deal-by-deal underwriting, can make it easier to keep buying duplexes, triplexes, and fourplexes as your portfolio grows.

That room to grow helps, but the approval hurdles below still count.

Approval Obstacles, Tradeoffs, and Key Takeaways

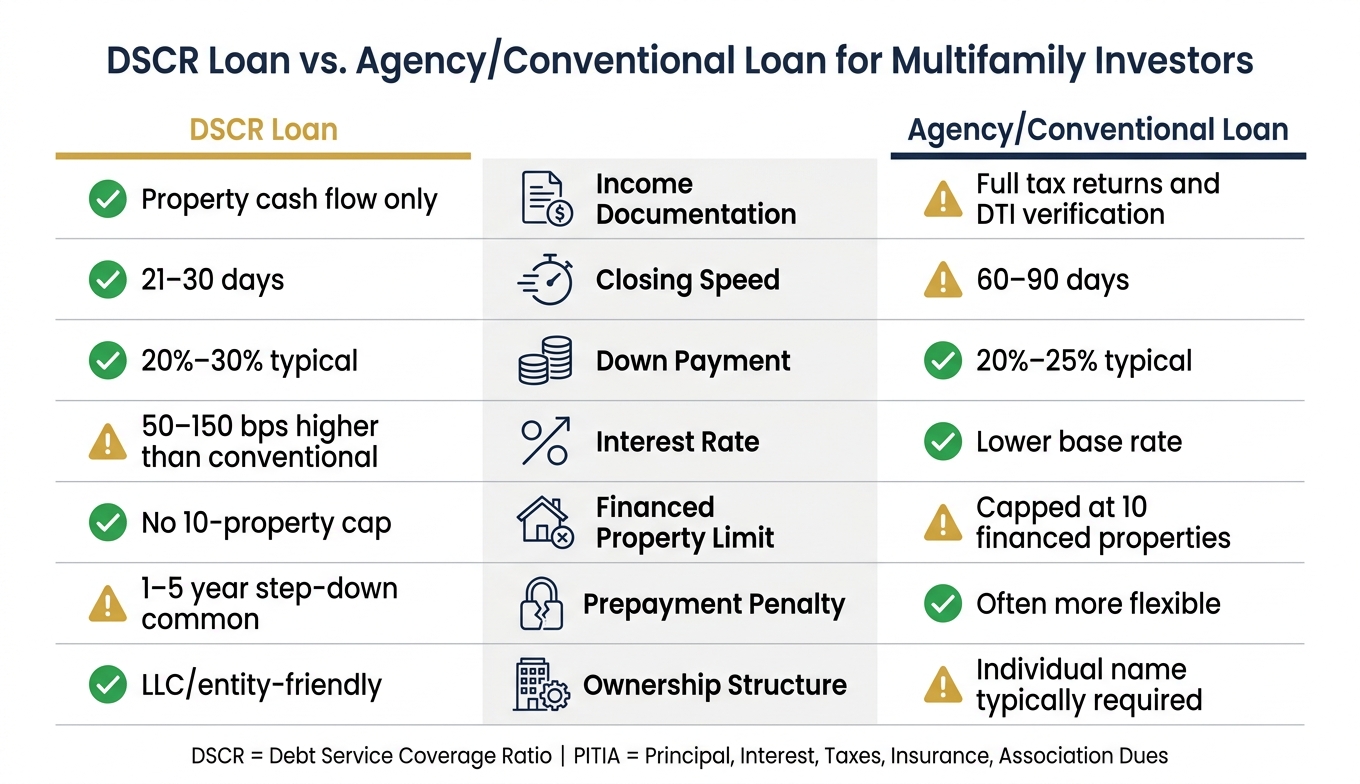

DSCR Loan vs. Conventional Loan for Multifamily Investors

Common Reasons Multifamily DSCR Loans Get Declined

Even solid deals can fall apart when the rent roll, reserves, or unit count don't match what the lender expects.

Low DSCR is the most common reason a file gets turned down. If the rent doesn't cover PITIA, the lender will usually lower leverage or decline the deal.

Overstated rents also cause problems all the time. Lenders use the lower of the lease rent or the appraiser's market rent. So if a pro forma is too aggressive, it gets trimmed back. That's why it helps to ask for the rent schedule early and check market rents before you get too far into the process.

Property condition can also stop a deal. Most DSCR loans require the property to be stabilized and rentable at closing. If the building still needs major repairs or hasn't stabilized yet, investors often use bridge debt first and then refinance into a DSCR loan once the property is ready.

Two late-stage problems are easy to miss: higher taxes after closing and illegal units. Lenders underwrite based on the reassessed tax bill, not the old one. And if the legal unit count is lower than what's shown on the rent roll, many lenders will deny the file.

| Common Decline Reason | How to Fix Before Applying |

|---|---|

| Low DSCR ratio | Increase the down payment or negotiate a lower purchase price |

| Overstated rents | Request the appraiser's rent schedule early to verify market rents |

| Insufficient reserves | Make sure you have the lender's required liquid PITIA reserves, often 3–12 months |

| Property condition | Address deferred maintenance before appraisal, or use bridge debt first |

| Illegal units | Verify the legal unit count with the city before ordering the appraisal |

Pros and Cons of DSCR Financing for Multifamily Investors

Those hurdles are the price you pay for faster, asset-based underwriting.

For many investors, the big draw is simple: no tax returns and a faster close. DSCR loans can also help when you're trying to grow and don't want to hit the same financed-property limits tied to agency debt. But there are tradeoffs. Rates are often higher, down payments are often larger, and prepayment penalties can make it harder to sell or refinance early without taking a hit.

| Feature | DSCR Loan | Agency/Conventional Debt |

|---|---|---|

| Income documentation | Property cash flow only | Full tax returns and DTI verification |

| Closing speed | 21–30 days | 60–90 days |

| Down payment | 20%–30% typical | 20%–25% typical |

| Interest rate | 50–150 bps higher | Lower base rate |

| Financed property limit | No 10-property cap | Capped at 10 financed properties |

| Prepayment penalty | 1–5 year step-down common | Often more flexible |

| Ownership structure | LLC/entity-friendly | Individual name typically required |

What to Remember Before Applying for a Multifamily DSCR Loan

Before you submit anything, stress-test the deal.

The basic idea is simple: the property qualifies the loan, not your personal income. But that doesn't mean every file gets through. Lenders still look hard at cash flow, reserves, credit, and property condition. The difference is that they judge those items through the asset, not through your tax returns.

A smart move is to run the DSCR with 8% vacancy and operating expenses 10% above your estimate. If the ratio falls below 1.10, the deal is thin and may get pushback. Verified DSCR, confirmed reserves, clean credit, and a legal unit count put you in a much better spot before the first document goes in.

FAQs

Can I qualify with vacant units?

Yes. For a DSCR loan, lenders usually don’t look only at current leases. They often use the appraiser’s market rent schedule to estimate the property’s expected monthly gross rent, even when some units are vacant.

If leases are already in place, underwriters generally use the lower of the actual lease amount or the appraised market rent when they review cash flow.

What counts against DSCR?

Several issues can drag down your DSCR or lead to a loan denial.

- Owner-paid utilities that cut into net operating income

- Below-market rents, since lenders usually look at current lease rates

- Deferred maintenance, like an aging roof

- Insurance risks, such as old wiring or a poor claims history

- Zoning or unit-count mismatches and environmental red flags, like buried tanks

Even small problems can snowball here. A property might look fine at first glance, but if expenses are too high, rents are too low, or the building has repair or insurance trouble, the deal can start to fall apart fast.

Are prepayment penalties common?

Yes. Prepayment penalties are common with DSCR loans, and they often follow a step-down schedule like 3-2-1, 5-4-3-2-1, or use yield maintenance.

Pick the structure that lines up with your hold plan. A longer prepayment term may help you get a lower rate. On the flip side, a shorter term can limit penalty costs if you expect to sell or refinance within three years.