DSCR Loans in California: Rates, Requirements, and Top Markets

California DSCR loans can work - but many deals fail on cash flow, not credit. As of July 11, 2026, rates in California are often around 6.125% to 9.125%, most lenders want at least 1.00 DSCR, and lower-ratio deals usually need more money down, better credit, or both.

If I had to boil this down for you, it’s this:

- Best pricing usually goes to borrowers with 740+ FICO, 1.25+ DSCR, and 25% to 30% down

- Most programs look for 620 to 640+ credit, 20% to 25% down, and 6 to 12 months of reserves

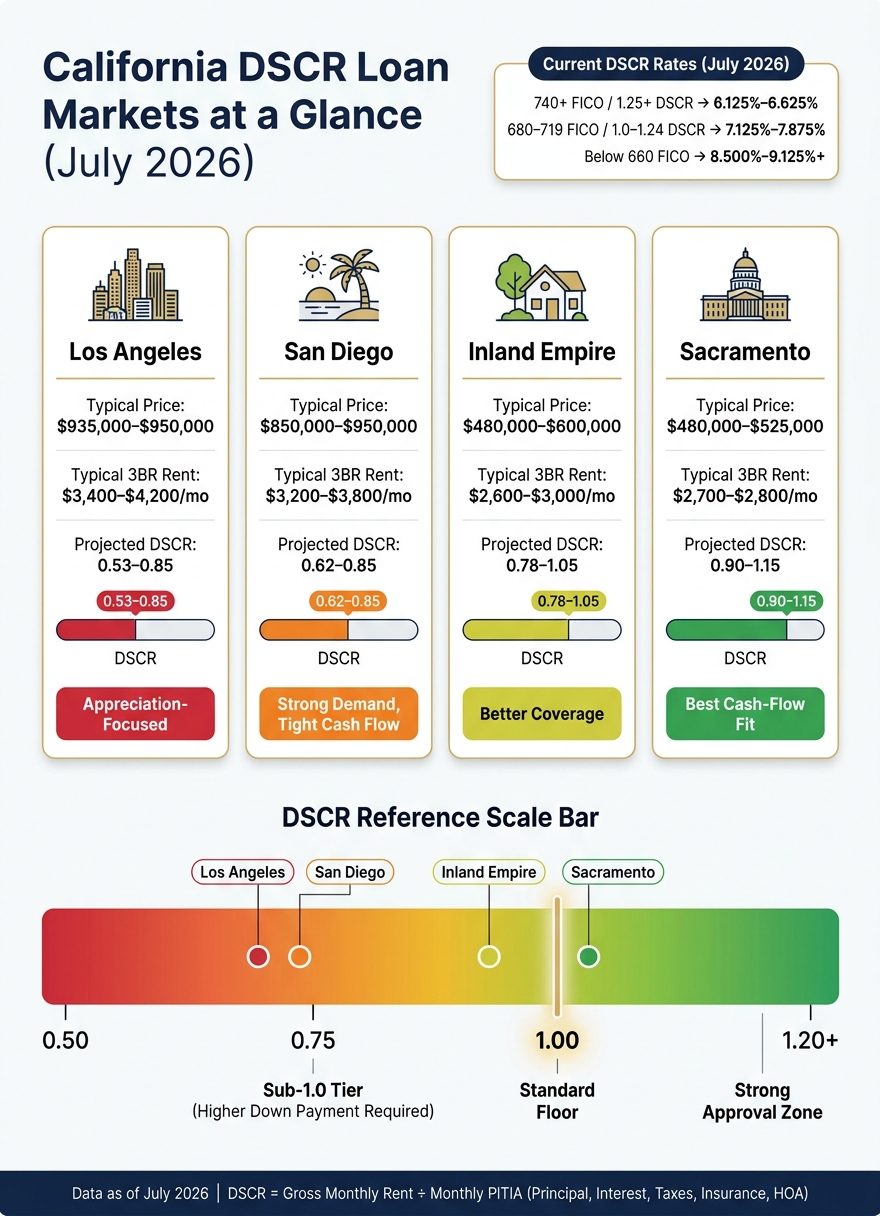

- Los Angeles and San Diego often have strong rent demand, but cash flow is tight because prices are high

- Sacramento and the Inland Empire tend to have better rent-to-price ratios, so DSCR approval is often easier

- Taxes, insurance, and HOA dues can make or break a California DSCR deal

- In wildfire areas, FAIR Plan insurance can push a file from workable to below 1.0 DSCR

Here’s the plain-English version: a DSCR loan is a rental property loan that leans on the property’s rent instead of your W-2s or tax returns. That’s why these loans get a lot of attention from self-employed borrowers, 1099 earners, and investors with multiple properties.

A fast way I’d screen a deal is simple: take the expected rent, divide it by the full monthly payment (principal, interest, taxes, insurance, and HOA), and see where it lands. Around 1.20+ is strong, 1.00 is the usual floor, and below 1.00 gets tighter.

| Market | Typical Price | Typical 3BR Rent | Usual DSCR Range | General Fit |

|---|---|---|---|---|

| Los Angeles | $935,000–$950,000 | $3,400–$4,200 | 0.53–0.85 | More price-growth focused |

| San Diego | $850,000–$950,000 | $3,200–$3,800 | 0.62–0.85 | Strong demand, tight cash flow |

| Inland Empire | $480,000–$600,000 | $2,600–$3,000 | 0.78–1.05 | Better coverage for many deals |

| Sacramento | $480,000–$525,000 | $2,700–$2,800 | 0.90–1.15 | Often the best fit for cash flow |

Bottom line: if you want a DSCR loan in California, focus on the math first. A deal with solid rent, enough down payment, and clean insurance numbers usually has a much better shot than one with high hopes and thin coverage.

DSCR Loan Requirements: What Lenders ACTUALLY Check

Current DSCR Loan Rates in California

As of July 2026, 30-year fixed DSCR rates in California range from 6.125% to 9.125%. That’s a pretty big gap, and there’s a reason for it: pricing in California tends to shift fast based on credit, property cash flow, leverage, and insurance costs.

Key Factors That Drive DSCR Loan Rates

Borrowers with a 740+ credit score and a 1.25+ DSCR can often land in the 6.125% to 6.625% range. Drop below a 1.0 DSCR, and the rate often picks up an extra 0.50% to 0.75% compared with deals at 1.0+ DSCR.

Property type plays a big part too. Two- to four-unit properties often come with a 0.125% to 0.25% add-on versus single-family rentals. Short-term rentals also tend to price above long-term rentals. On the refinance side, rates can start around 6.25% for well-qualified borrowers.

Insurance can change the math in a hurry. In wildfire-prone areas, a property may need FAIR Plan coverage, and the higher premium can push a deal that looked fine on paper to below 1.0 DSCR. In high-cost California markets, that matters a lot because rent often doesn’t rise as fast as debt service.

How California Property Values Affect Cash Flow and Eligibility

Home prices are one of the main pressure points for DSCR loans in California. In Los Angeles, the median purchase price is about $950,000, and rents around $3,500 to $4,200 per month can still leave a property with a DSCR of just 0.70 to 0.85. That means many deals need either stronger rent, a larger down payment, or both.

Once loan sizes move above about $1.5 million to $3 million, they usually fall into jumbo DSCR territory. Those loans often call for 25% to 30% down.

By contrast, inland markets such as Sacramento and the Inland Empire often work better on cash flow. Median purchase prices there run about $480,000 to $520,000, and DSCRs are often close to break-even, around 0.90 to 1.05.

California also tends to price a bit above the U.S. norm. Because of tenant laws and slower eviction timelines, lenders may add about 0.125% to 0.25% over typical national pricing for California properties.

Rate Drivers by Credit Tier and DSCR Level: Comparison Table

Use these bands as a quick screen before moving into full loan requirements.

| Credit Tier (FICO) | Typical DSCR Range | Approximate Rate Band | Common Pricing Notes |

|---|---|---|---|

| 740+ | 1.25+ | 6.125% – 6.625% | Best pricing tier; often 30%+ down |

| 720–739 | 1.25+ | 6.625% – 7.125% | Strong tier; often 25% down |

| 680–719 | 1.0 – 1.24 | 7.125% – 7.875% | Standard investor tier; often 20%–25% down |

| 660–679 | 0.75 – 0.99 | 7.875% – 8.500% | Moderate/low-DSCR tier; often 20% down |

| Below 660 | Below 0.75 | 8.500% – 9.125%+ | Challenging tier; higher equity required |

Source: Compiled from July 2026 market data

Rates vary based on credit, leverage, cash flow, property type, and market.

DSCR Loan Requirements for California Rental Properties

In California, DSCR approval usually comes down to four things: rental income, credit score, leverage, and cash reserves. After investors look at rates, this is usually the next step: figuring out whether a rental will actually make it through underwriting.

DSCR, Credit Score, Down Payment, and Reserve Benchmarks

Most standard programs want a minimum DSCR of 1.00. In plain English, that means the property's gross rent needs to cover the full monthly payment, including principal, interest, taxes, insurance, and HOA dues. Some lenders will go below that and allow DSCR as low as 0.75, but there's usually a catch. You may need a higher credit score, a larger down payment, or both to make that deal work.

Credit score minimums often begin around 620 to 640 for entry-level programs. But that doesn't mean every borrower in that range gets the same deal. For high-balance loans, lenders often want 700+, and the best pricing tiers usually start at 760+.

Down payments tend to land in the 20% to 25% range for many standard DSCR loans. If you're dealing with a sub-1.0 DSCR property or a jumbo loan above $1 million, expect the down payment to move up. In those cases, 30% to 35% is more common.

Reserves matter too. Many lenders want 6 to 12 months of PITIA reserves in liquid accounts. And in California, that bar can move higher when insurance costs are steep, which happens more often than many investors expect.

In this market, taxes, insurance, and leverage can matter just as much as the DSCR number itself.

Eligible Property Types and Ownership Structures

Eligible properties usually include single-family rentals, condos, townhomes, 2–4 unit properties, and PUDs. Some lenders will also allow non-warrantable condos and short-term rentals (STRs). With STRs, though, lenders often want more backup. That can mean documented income history or third-party rent data to support the rent figure used in underwriting.

One rule is pretty simple: primary residences and second homes do not qualify.

For ownership, investors can usually close in their individual name or through an LLC, corporation, or partnership. A lot of California investors use an LLC for liability reasons. Still, lenders will want entity documents, and they typically require a personal guarantee from the main member.

Core Requirements for California Investors: Comparison Table

| Requirement | Typical DSCR Standard | California-Specific Notes |

|---|---|---|

| Minimum DSCR | 1.00 – 1.25 | Sub-1.0 DSCR tiers can go as low as 0.75 with a larger down payment or stronger credit |

| Credit Score | 620 – 640 minimum | 700+ is often needed for high-balance loans, and 760+ is typically needed for best-tier pricing |

| Down Payment | 20% – 25% | 30%–35% is more common for sub-1.0 DSCR deals or jumbo loans over $1 million |

| Cash Reserves | 6 – 12 months PITIA | Coastal properties with higher insurance costs can require stronger reserves; California property taxes are underwritten at roughly 1.1%–1.25% of purchase price, not the seller's Proposition 13 bill, which can push the monthly payment calculation higher than expected |

| Property Types | SFR, 2–4 units, condos, townhomes, PUDs | Some lenders also accept non-warrantable condos and STRs, subject to permit and history review |

| Ownership Structure | Individual, LLC, corporation, or partnership | LLC vesting requires entity documents and a personal guarantee; California LLCs also owe the $800 annual franchise tax |

| Documentation Focus | No tax returns or W-2s | Underwriting centers on the 1007 rent schedule, lease agreements, appraisal, and insurance quotes |

| Max LTV | 75% – 80% | LTV can drop to 65%–70% in high wildfire-risk zones |

These benchmarks are usually the first screen in underwriting. After that, lenders look at the numbers on the actual property and calculate DSCR on the live deal.

sbb-itb-e7c549b

How DSCR Qualification Works in Practice

The DSCR Formula and What Lenders Actually Review

Once you know the rate and program rules, the next hurdle is simple: does the property cash flow?

The basic formula looks like this:

DSCR = gross monthly rent ÷ monthly PITIA

PITIA includes:

- principal

- interest

- taxes

- insurance

- HOA dues

In California, taxes and insurance often swing the numbers. Lenders usually underwrite property taxes based on the reassessed value after the transfer, and they want a final insurance quote before signing off. If the home sits in a wildfire-risk area, higher premiums can cut into the DSCR in a big way.

On the rent side, lenders usually rely on the appraiser's Form 1007 rent schedule, not the borrower's own estimate. And if the property is in a rent-controlled city, underwriters may use the legally registered rent instead of a higher market rent.

One more lever here: an interest-only payment structure can improve the ratio because it lowers monthly debt service.

A Quick Pre-Screening Method for California Rentals

Before you apply, do a simple pre-screen.

Start with market rent backed by the appraiser's Form 1007 rent schedule. Then estimate post-transfer property taxes at about 1.2% of the purchase price, add the final insurance quote, and compare that total against the projected monthly PITIA.

As a rule of thumb:

- 1.20+ is strong

- 1.00 is the baseline

- Below 1.00 is a tighter fit and may call for stronger credit or a bigger down payment to fit lower-DSCR programs

That same rent-versus-payment math is often what separates stronger California rental markets from weaker ones.

LoanGuys.com: From Pre-Qualification to Closing

If the property clears the cash-flow test, the next move is a fast pre-qualification review.

LoanGuys.com reviews DSCR loans based on property cash flow, credit profile, and reserves - not tax returns, W-2s, or pay stubs. That makes the process simpler for self-employed borrowers, 1099 earners, foreign nationals, and investors who already have multiple financed properties.

Top California Markets for DSCR Loans and Key Takeaways

California DSCR Loan Markets Compared: Rates, DSCR & Cash Flow (2026)

Los Angeles and San Diego: Strong Rental Demand, Higher Prices

Once your rate and underwriting terms are set, market selection tends to decide how workable the deal is. In California, the rent-versus-PITIA test from the previous section is often the line between a property that qualifies and one that doesn’t.

Los Angeles County is California’s highest-volume DSCR market, with San Diego County right behind it. Both markets have strong rental demand. The catch is simple: prices are high, cash flow is tighter, and rent-to-price ratios are lower, which makes DSCR approval tougher.

In Los Angeles, median single-family home prices sit around $935,000 to $950,000, while typical 3-bedroom rents land near $3,400 to $4,200. That puts projected DSCR at about 0.53 to 0.85. San Diego looks similar. Prices are roughly $850,000 to $950,000, typical 3-bedroom rents are about $3,200 to $3,800, and projected DSCR usually falls between 0.62 and 0.85.

That gap matters. Even with solid demand, many investors in these markets need to lean on a larger down payment, an interest-only setup, or a lender program that allows ratios as low as 0.75. Insurance can also change the math fast. In wildfire-prone areas, FAIR Plan coverage may push costs up enough to squeeze a property’s DSCR before the loan even gets far in underwriting.

Sacramento and Inland Empire: Better Rent-to-Price Ratios

This is where the numbers usually get friendlier for DSCR loans. Sacramento and the Inland Empire tend to offer better cash-flow ratios because purchase prices are lower relative to rents. As a result, debt service coverage more often gets close to - or moves past - the 1.0 mark.

In Sacramento, single-family homes usually cost around $480,000 to $525,000, and DSCR ratios can reach 0.90 to 1.15. In the Inland Empire, prices often fall between $480,000 and $600,000, with DSCR ratios usually landing in the 0.78 to 1.05 range. Rents in both markets also get support from migration out of higher-cost coastal counties.

For buy-and-hold investors, that can make a big difference. These markets are often a better fit for portfolio growth because the deal is less likely to depend on heavy leverage tweaks just to make the DSCR work.

California Market Comparison Table and Final Takeaways

| Market | Typical Price Level | Typical Rent (3BR) | Projected DSCR | Investor Fit |

|---|---|---|---|---|

| Los Angeles | $935,000 – $950,000 | $3,400 – $4,200 | 0.53 – 0.85 | Appreciation-focused; cash flow tighter |

| San Diego | $850,000 – $950,000 | $3,200 – $3,800 | 0.62 – 0.85 | Demand strong; cash flow tighter |

| Inland Empire | $480,000 – $600,000 | $2,600 – $3,000 | 0.78 – 1.05 | Better coverage; workforce demand |

| Sacramento | $480,000 – $525,000 | $2,700 – $2,800 | 0.90 – 1.15 | Best cash-flow fit; value play |

FAQs

How do lenders calculate DSCR in California?

Lenders calculate DSCR by dividing a property’s gross monthly rental income by its total monthly mortgage payment, or PITIA.

PITIA includes:

- Principal

- Interest

- Property taxes

- Insurance

- HOA dues, if the property has them

For rental income, lenders usually rely on the appraiser’s market rent opinion. In California, underwriters may also account for local rent control and stress-test insurance and tax costs.

Can I qualify with a DSCR below 1.00?

Yes. Many lenders will still approve a DSCR below 1.00 - in some cases as low as 0.75. That happens most often in high-cost California coastal markets, where home prices run high and rent-to-price ratios are tighter.

The catch? You’ll usually pay for that flexibility with a higher interest rate, often 0.50% to 1.50% more than loans with a 1.00+ DSCR. Some lenders may also ask for a larger down payment and a higher credit score.

Which California markets work best for DSCR loans?

The strongest California markets for DSCR loans are usually the ones where home prices stay low enough, compared with rents, to support a healthy debt service coverage ratio.

The Inland Empire, Central Valley - especially Fresno and Bakersfield - and Sacramento tend to offer the best setup for investors. In those markets, the math often works better.

Los Angeles and San Diego can be harder to pencil out because purchase prices are much higher, and rent control rules can be stricter. That said, some investors still make those markets work by focusing on select submarkets or legal short-term rentals to improve cash flow.