Fix and Flip Financing: Best Loan Options for Real Estate Investors in 2025

Fix-and-flip profits are tighter in 2025, so the loan can make or break the deal. With national gross flip returns at 25.1% in Q2 2025, high rates, slow draws, or weak leverage can eat into your margin fast.

If I were sizing up a deal, I’d focus on six loan paths:

- Fix-and-flip loans for heavy rehab and one loan for purchase + renovation

- Bridge loans for fast closings and light property cleanup

- Hard money loans for distressed deals and weaker borrower profiles

- DSCR refinance loans for turning a completed project into a rental

- Private money for flexible terms and relationship-based funding

- Lines of credit for repeat investors who need reusable capital

The short version is simple:

- If you need to close in 5 to 14 business days, look at bridge or hard money

- If the rehab is large, fix-and-flip loans usually fit better

- If you plan to keep the property, the exit often leads to a DSCR refinance

- If you do deals over and over, a line of credit may cut borrowing cost per project

- If banks say no, private money or hard money may still work

What I like about this comparison is that it looks at the parts that matter most in a flip: close time, down payment, rehab draws, leverage, rates, and exit plan.

Fix and Flip Loan Types Compared: Rates, Speed & Best Use (2025)

How to Get Easy Loans for Fixer Properties in 2025 (Hard Money EXPLAINED)

sbb-itb-e7c549b

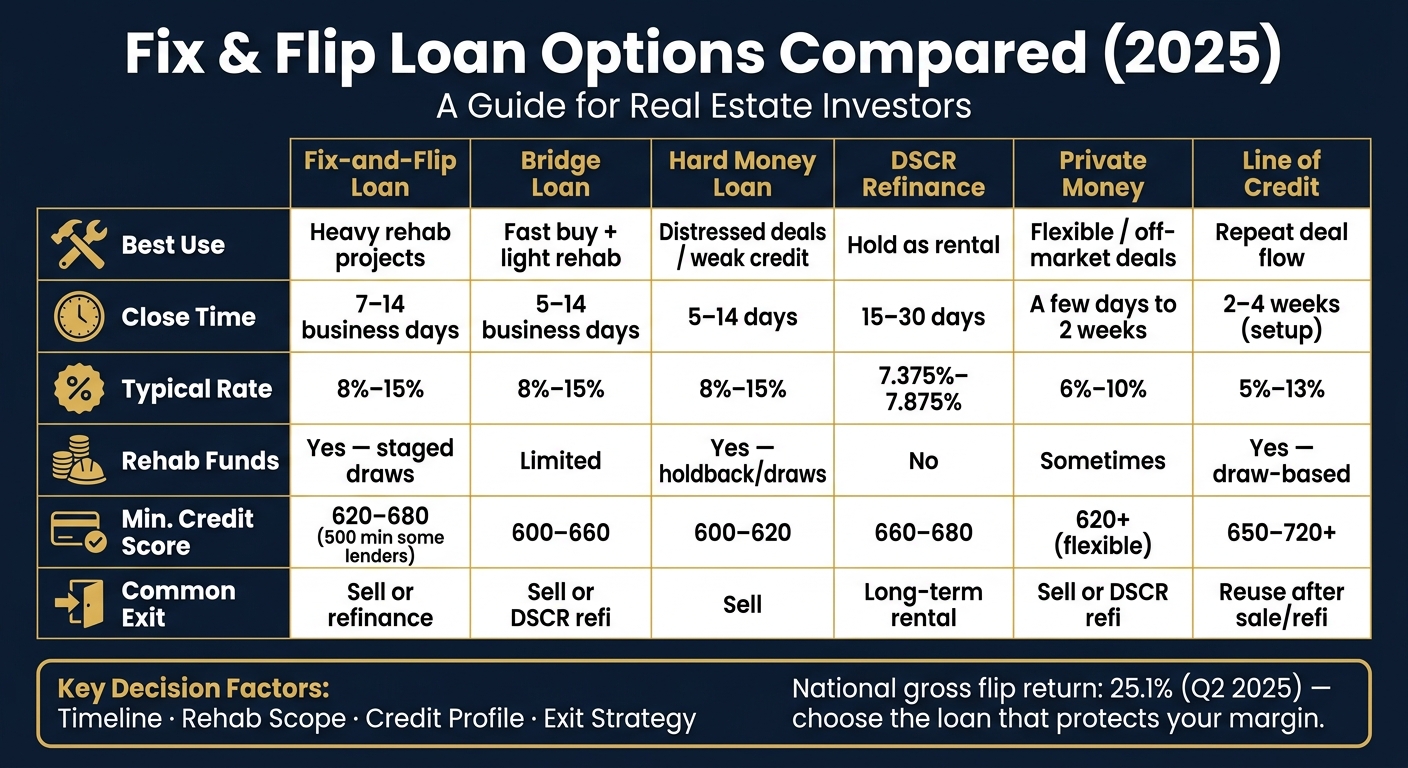

Quick Comparison

| Loan Type | Best Use | Close Time | Typical Rate | Rehab Funds | Common Exit |

|---|---|---|---|---|---|

| Fix-and-flip | Heavy rehab | 7–14 business days | 8%–15% | Yes, staged draws | Sell or refinance |

| Bridge | Fast buy + light rehab | 5–14 business days | 8%–15% | Usually limited | Sell or DSCR refi |

| Hard money | Distressed deals | 5–14 days | 8%–15% | Yes, holdback/draws | Sell |

| DSCR refinance | Hold as rental | 15–30 days | 7.375%–7.875% | No rehab focus | Long-term rental debt |

| Private money | Flexible deal terms | A few days to 1–2 weeks | 6%–10% | Sometimes | Sell or DSCR refi |

| Line of credit | Repeat deal flow | 2–4 weeks to set up | 5%–13% | Draw-based | Reuse line after sale/refi |

Bottom line: I’d pick the loan based on timeline, rehab scope, borrower profile, and exit - not just the headline rate. In a thin-margin market, that choice matters more than ever.

1. Fix-and-Flip Loans

Fix-and-flip loans roll the purchase and rehab budget into one short-term loan. That makes them a strong fit for heavy rehabs, including structural work and full gut jobs. If you need to close fast and keep rehab money under control, this is the standard option. In a tighter-margin market, speed and draw control matter more than ever.

Speed to Close

Most fix-and-flip loans close in 7 to 14 business days. On cleaner deals, with a clear scope of work and a solid borrower file, some lenders can close in as little as 5 to 7 days.

Qualification & Down Payment

Most lenders look for a 620 to 680 credit score, though some will go as low as 500. Borrowers with two or more completed flips often get better pricing and more leverage. First-time investors can still qualify, but they usually need a detailed project plan and a licensed contractor lined up before closing.

Down payments tend to fall between 10% and 25%. Lenders also want to see cash reserves at closing. That cash helps cover interest payments, closing costs, and any rehab overages that pop up during the project.

Rehab Funding & Leverage

Rehab funds are usually held in escrow and paid out through staged draws once work milestones are checked off. In many cases, lenders use virtual inspections, with turnarounds in 24 to 48 hours.

Most lenders will fund 90% to 95% of total project cost and cap the loan at 70% to 75% of ARV.

Cost & Exit Fit

Pricing changes based on leverage, borrower strength, and the deal itself. Rates currently range from 8% to 15%, and the average dropped to 10.43% in September 2025. Origination fees usually run 1 to 3 points, and terms are often 6 to 18 months. During rehab, payments are usually interest-only, which can ease monthly cash flow while the work gets done.

The most common exit is a resale. Some investors, though, refinance after the rehab instead of selling.

If you need more time on the repayment side, bridge loans are usually the next option to compare.

2. Bridge Loans

When you need to close FAST but don't need full rehab funding, bridge loans can be a good middle ground. They help cover the gap between moving on a deal fast and keeping some room to improve the property. In most cases, they're best for fast acquisitions and light repositioning, not major construction. That makes them a better fit for properties that need minor cosmetic work or are already close to stabilized condition than for heavy structural rehabs.

Speed to Close

Bridge loans usually close within 5 to 14 business days, and some lenders can fund in as little as 5 business days. That kind of speed can make all the difference when you're up against cash buyers, trying to secure an auction deal, or buying a property before another one sells.

Qualification & Down Payment

Most lenders care more about the property's value, your exit plan, and your minimum credit score than your income or DTI. Most want a minimum FICO score in the 600 to 660 range, while scores above 680 to 720 usually qualify for the best rates and more leverage.

Down payments often fall between 10% and 25%, based in part on your experience level. Lenders also tend to require reserves so you can cover carrying costs during the hold period.

Cost & Exit Fit

Rates in 2025 usually range from 8% to 15%, with origination fees from 0 to 3 points. Terms are often 6 to 18 months, and most bridge loans are set up as interest-only. That helps keep monthly payments lower while you hold the property.

Most borrowers exit with either:

- A resale

- A refinance into a long-term DSCR loan

Bridge loans stand out for speed and light repositioning. They are not built around draw-based rehab funding. If the project involves heavier renovations and you need more room around draw structures, hard money loans are the next option.

3. Hard Money Loans

Hard money is short-term private financing backed by the property itself. In plain English, the deal matters more than your income. That’s why these loans often work well for distressed homes and for lenders that look at the asset first.

Speed to Close

Hard money loans usually close in 7 to 14 days. If the file is clean, funding can happen in 5 to 7 days.

That kind of speed matters when time is tight. Think foreclosure purchases, distressed estate sales, auctions, or deals that fell apart after a conventional loan failed.

Qualification & Down Payment

Most hard money lenders care most about two things: the collateral and your exit plan. Typical minimum FICO scores fall between 600 and 620, though scores above 680 often lead to better pricing and more leverage. Many lenders also shape terms around a 24 to 36-month project track record.

Down payments depend on the lender and your experience level:

- First-time flippers often need to put down 15% to 25%

- More experienced borrowers may get deals in the 5% to 20% range

- On some projects, lenders still ask for 25% to 40% of the purchase price

Rehab Funding & Leverage

Hard money lenders size loans using LTV, LTC, and LTARV. In many cases, LTV and LTARV top out at 65% to 75%, while LTC can go as high as 90% to 100% for qualified borrowers.

Renovation money is usually kept in a construction holdback. The lender releases those funds in stages after completed work is inspected. In other words, draws are reimbursements, not upfront advances. If you’re paying for the rehab in cash, you may be able to avoid holdbacks and draw reviews altogether.

Cost & Exit Fit

In 2025, rates usually land between 8% and 15%. Origination fees are often 1 to 3 points upfront. Terms stay short, usually 6 to 24 months, and most loans are interest-only with a balloon payment due at maturity.

One thing to watch: extension fees. If the rehab drags on, those costs can pile up fast.

Hard money usually fits best when the exit is a resale. If the plan is to keep the property, a DSCR refinance is often the next loan type to compare.

4. DSCR Refinance Loans

DSCR refinance loans are usually the exit move after a rehab. They swap short-term funding for long-term rental debt based on the property’s income, not your personal tax returns or W-2s. If you’re coming out of a flip loan, bridge loan, or hard money loan, DSCR is often the main refinance route when the plan changes from selling to holding as a rental.

Qualification & Seasoning

DSCR stands for gross monthly rent divided by monthly principal, interest, taxes, insurance, and HOA dues. Most lenders want to see a ratio between 1.1 and 1.25. Put simply, rent needs to come in 10% to 25% above the monthly payment. Minimum FICO scores often start at 660 for refinances, but borrowers in the 680 to 720 range usually get better rates.

There’s also a timing issue. Most lenders want 3 to 6 months of seasoning before they’ll allow a cash-out refinance based on the new appraised value. That can push the refinance back by a few months, which means more carrying costs while you wait.

That’s why DSCR tends to work best once the rehab is done and the unit is rent-ready.

Speed to Close

DSCR refinances usually close in 15 to 30 days. That’s often faster than conventional investment loans, which commonly take 30 to 45 days.

Cost & Exit Fit

Rates for stabilized rentals run from 7.375% to 7.875%. Origination fees are usually 1 to 3 points, and most loans come with a 3- to 5-year prepayment penalty. Maximum leverage goes up to 75% LTV for cash-out refinances and up to 80% for rate-and-term refinances.

For investors who want to keep the property, a DSCR refi can make more sense than selling. A sale can trigger capital gains taxes plus about 6% in commissions and closing costs. A refinance, on the other hand, lets you pull equity out as tax-advantaged debt proceeds while still holding the asset.

Here’s where the math gets interesting: if ARV comes in at least 20% to 25% above all-in costs, a cash-out refinance at 75% LTV can return most or even all of the original capital. That leaves the property in your portfolio with little equity still tied up.

If cash-out room matters more than lender rules, private money is the next path.

5. Private Money

Private money comes from individuals or other non-institutional lenders. You work out the terms directly, so the structure can be much more flexible than what you'd get from a bank. That's why private money tends to make sense when speed and flexibility matter more than fixed pricing.

Speed to Close

Private money can often close in just a few days and usually funds within 1 to 2 weeks. The main reason is simple: underwriting is lighter, and approval often depends more on the relationship than on a rigid checklist. That makes private money a strong fit for off-market deals and for properties that banks won't touch.

Qualification & Down Payment

With private money, the lender is often more focused on the deal than on the borrower. They look closely at the property's condition, the rehab plan, and the projected ARV. They also want to see a clear exit strategy. Tax returns and W-2s usually carry less weight here.

Credit standards can vary a lot. Some lenders don't set a minimum at all, while others look for about 620+. Down payments usually fall between 5% and 25%, depending on the lender and the investor's track record.

Rehab Funding & Leverage

Private lenders may finance up to 90% LTV and, in some cases, cover the full purchase price plus rehab costs. Private money can also fill a gap by covering the down payment and reserves that a primary hard money lender requires. Some deals use holdbacks, but draw schedules are often looser than with hard money.

Cost & Exit Fit

Rates are negotiable and usually land between 6% and 10%. Origination fees are often around 0 to 1 point. Terms are short in most cases, usually 6 to 18 months.

The usual exit is a quick resale. If the plan is to keep the property as a rental, a DSCR refinance is a common next step. For investors who want capital they can reuse across repeated deals, lines of credit are next.

6. Lines of Credit

A line of credit gives you revolving capital. You can draw funds, pay them back, and use them again. That setup works best for investors doing multiple deals over time, not a one-and-done flip. In plain English: if you have repeat deal flow, a line of credit can make a lot of sense.

Speed to Close

Initial approval usually takes 2 to 4 weeks. Once the line is open, draws tend to move fast for repeat borrowers.

Qualification & Reserves

Lenders often want to see 5+ completed flips and a 650 to 720+ credit score. Some also ask for reserves equal to at least 10% of the line amount.

If you're new, this is where things get tougher. Investors without a track record often need to finish 2–3 successful flips with individual hard money loans before they can qualify for a line.

Rehab Funding & Leverage

Some lines fund up to 80% LTC. You only pay interest on the amount you draw, which can help keep borrowing costs down when you don't need the full credit limit right away.

There is a catch: renovation draws still need inspection approval before the next draw is released. Some lines can also be secured by equity in existing rental properties instead of your primary residence.

Cost & Exit Fit

| Line Type | Est. Interest Rate | Typical Term |

|---|---|---|

| HELOC | 5% – 10% | 5 – 15 years |

| Commercial Fix-and-Flip LOC | 10% – 13% | 12 – 24 months |

For BRRRR deals, the line can cover the purchase and rehab, then a DSCR refinance pays it off after the property is stabilized. For flips, the line usually resets when the property sells. Investors who want one funding source for fix-and-flip, bridge, and DSCR loans can compare those paths in the next section.

7. LoanGuys.com Fix-and-Flip, Bridge, and DSCR Investor Financing

LoanGuys.com offers fix-and-flip, bridge, and DSCR financing for U.S. real estate investors. It's most useful when a deal needs one clear path from purchase to refinance.

Speed to Close

Fix-and-flip and bridge loans can close in as little as 5 to 7 business days for straightforward deals. That's fast enough for investors who need to move before a seller loses patience or another buyer steps in.

DSCR refinance loans take longer, which is standard for a refinance exit. So if timing is tight, it helps to sort out one thing early: Is the plan to sell, or to refinance?

Qualification & Down Payment

Approval leans more on the property's ARV and the strength of the deal than on tax returns or W-2s. That's a good fit for borrowers whose income doesn't show up in a neat, bank-friendly way.

This can work well for:

- self-employed borrowers

- 1099 earners

- foreign nationals

- borrowers declined by banks

Rehab Funding & Leverage

Fix-and-flip loans use an initial advance plus rehab holdbacks tied to verified work. Put simply, the loan amount comes down to the deal's numbers and the property's ARV.

That setup tends to make sense for investors who need cash for both the purchase and the renovation, not just one or the other.

Cost & Exit Fit

This is where the loan type needs to match the business plan. For a buy-rehab-rent-refinance strategy, a fix-and-flip or bridge loan funds the project first. Then, once the property is stabilized and renting, a DSCR refinance replaces that short-term loan.

That handoff - from acquisition financing to long-term DSCR debt - is the move from purchase to refinance. The next step is to line up each loan type with the deal scenario it fits best.

Pros and Cons by Deal Scenario

Use the table below to match the loan to the deal.

| Deal Scenario | Best Fit | Key Tradeoff |

|---|---|---|

| Fast-close auction purchase | Hard money / Bridge loan | Higher rates (up to 15%) for 5- to 10-business-day closing speed |

| Heavy structural rehab | Fix-and-flip loan | Up to 95% LTC, but funds are released only after milestone inspections |

| Borrower with weaker credit | Hard money loan | Asset-based approval; minimum FICO around 600–620 |

| Flip-to-rental deal | Bridge-to-DSCR combo | Single-close convenience vs. refinance execution risk |

| Cosmetic rehab | Line of credit | Lower rates (6%–10%) but ties up personal equity |

| Repeat investor with steady deal flow | Business line of credit | Lower cost per deal, but requires a 24–36 month track record |

The table makes one thing pretty clear: the best loan depends on the deal in front of you.

If you're buying at auction and need to close in a hurry, hard money and bridge loans are often the only options that can move fast enough. But that speed isn't cheap. You're paying higher rates for a 5- to 10-business-day close.

For heavy structural rehab, fix-and-flip loans make sense because they cover both the purchase and the rehab budget. That said, the draw process can be a pain. Funds come out in stages after milestone inspections, which means you may need to front some costs before you get paid back.

Hard money can also help borrowers with weaker credit. Why? Because approval leans more on the asset than on the borrower's profile. Even so, lenders still tend to want a minimum FICO in the 600–620 range.

A lot of investors in 2025 are using short-term financing as a first step, then moving into rental debt. That's where a bridge-to-DSCR setup can work well for a flip-to-rental deal. It gives you room to buy now and decide later whether to hold. The catch is the refinance has to line up at the right time. The property needs to be stabilized and rented first, and until that happens, the short-term loan keeps piling on interest.

For cosmetic rehab, a line of credit can be a cheaper tool. Rates can land in the 6%–10% range, which looks a lot better than hard money. Still, there's a catch: you're tying up your own equity to make the deal work.

If you're a repeat investor with a steady stream of deals, a business line of credit can cut your cost per deal. But lenders usually want proof that you've been doing this for a while, often a 24–36 month track record.

The notes below show where each option starts to crack:

- Fast money costs more. Hard money and bridge loans move fast, but they charge for that speed.

- Draw-based rehab funding can squeeze cash flow. Fix-and-flip loans work for heavy projects, but staged reimbursement means you need cash ready before the lender sends funds.

- Refinance plans can slip. A bridge-to-DSCR path only works once the property is rent-ready and producing income, so delays can stretch your holding costs.

The conclusion below pulls these tradeoffs into one final recommendation.

Conclusion

After lining up each loan type side by side, the choice is about fit, not just the lowest rate in big print. The right fix-and-flip financing usually comes down to four things: timeline, rehab scope, credit profile, and exit strategy.

The best loan should match the deal itself. Fast-close projects often lean toward hard money or bridge loans. Rehab-heavy flips tend to fit fix-and-flip financing. Longer holds usually point to DSCR. And if you're doing repeat deals, credit lines can make more sense.

Before you commit, run the full math: total project cost, cash due at closing, and payoff timing against the loan's maturity date. Thin margins don't give you much breathing room if the loan doesn't line up with the deal timeline or your exit.

Before you sign, get your scope of work, contractor bids, and exit plan in order. Good prep can speed up approval and help cut avoidable pricing friction. It also helps to add a 10% to 20% contingency buffer for overruns.

FAQs

How do I choose the right loan for my flip?

Choose the loan based on your project scope, your experience, and how you plan to get out of the deal. Fix-and-flip loans are often a good fit for larger renovation projects because they can cover both the purchase price and rehab costs, with funds released in draws tied to construction milestones.

If the property needs less work, or you need to move fast, a bridge loan or hard money loan may make more sense. First-time flippers may run into 15%–25% down payments and tighter underwriting. It also helps to line up the loan term with your resale or refinance plan.

What cash should I have before closing?

Before closing, you'll usually need cash for:

- the down payment

- closing costs

- a reserve or contingency buffer

You should also budget for origination points, underwriting fees, and any required interest reserves.

One more thing: rehab funds are often paid out on a draw schedule, not all at once. That means you may need cash on hand to cover early project costs before reimbursements come in. It also helps to have extra room in your budget for surprise repairs, delays, or market changes.

When should I refinance into a DSCR loan?

Refinance into a DSCR loan once the property is stabilized, renovated, and bringing in rental income. This often makes sense when your plan changes from a quick flip to a long-term rental hold.

DSCR loans look at the property’s cash flow more than your personal income. That can make them a good fit for long-term financing. It can also help you pull out equity and put that money into your next deal without selling the property.