Fix and Flip Loans With No Money Down: 100% Financing Options Explained

“No money down” on a flip almost never means $0 out of pocket. In most cases, it means a lender may fund 100% of the purchase price and rehab budget up to a cap of about 70% to 75% of after-repair value (ARV). If your deal goes over that cap, you cover the gap - plus points, closing costs, and reserves.

Here’s the short version: if you buy for $300,000, plan $80,000 in repairs, and the ARV is $440,000, a 70% ARV cap limits the loan to $308,000. That leaves $72,000 unfunded before fees. On top of that, many borrowers still need $20,000 to $45,000 for closing costs, points, interest reserves, and draw timing.

If I were sizing up this kind of loan, I’d focus on five things first:

- ARV cap vs. total project cost

- Cash needed at closing

- Credit score and flip experience

- Liquidity for draw gaps and holding costs

- Exit plan if the sale takes longer than expected

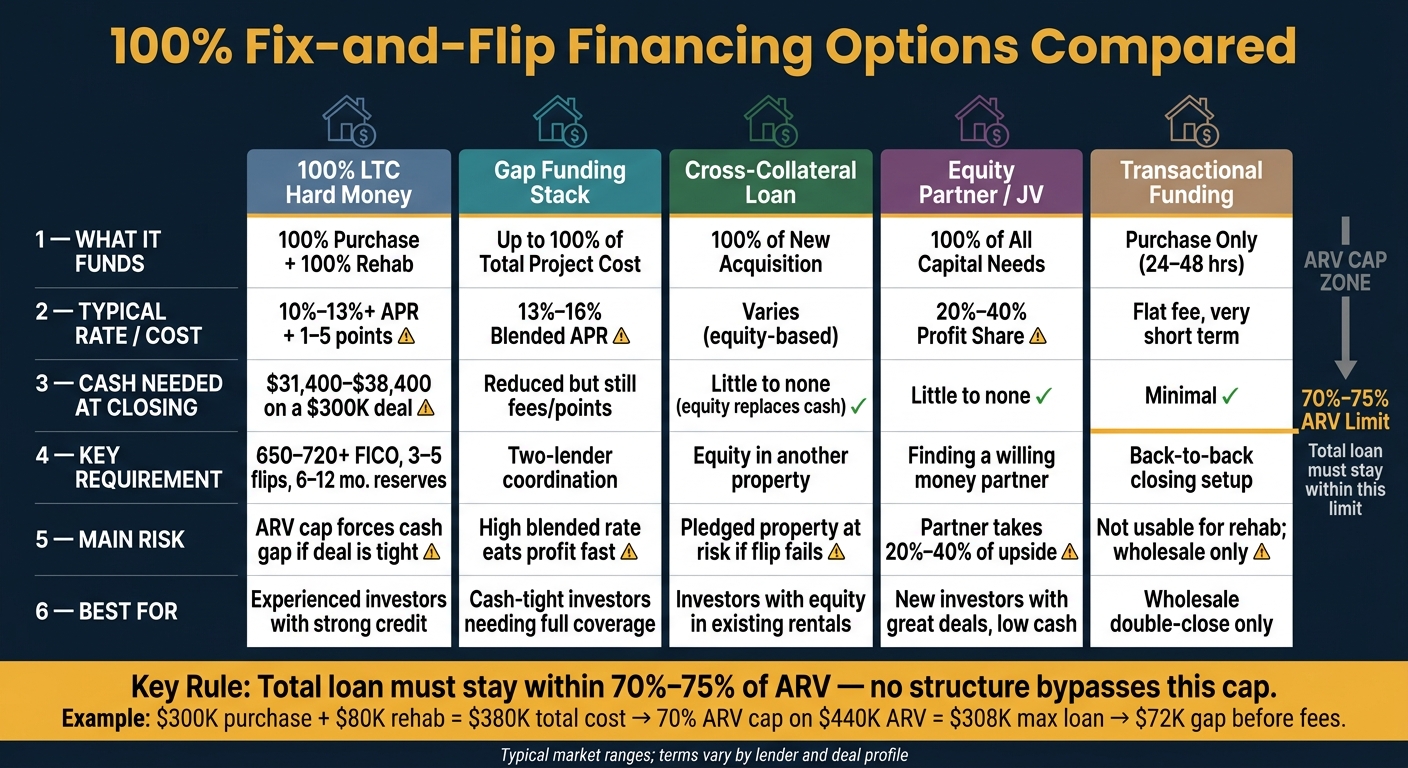

Some structures can reduce upfront cash, but each comes with a trade-off. A stacked hard money + gap loan can fill more of the project, but rates can land around 13% to 16% APR blended. Cross-collateral can remove the cash down piece, but it puts another property at risk. A money partner can fund the full deal, but often takes 20% to 40% of the profit.

How I’d Structure the Capital for This $1.8M Flip

Quick Comparison

| Option | What it can cover | Main limit | Main cost/risk |

|---|---|---|---|

| 100% LTC loan | Purchase + rehab | Usually still capped at 70%–75% ARV | Fees, reserves, and closing cash |

| Hard money + gap funding | Up to full project cost | Two-loan structure | High blended rate and points |

| Cross-collateral loan | New purchase, sometimes more | Needs equity in another property | Other property is on the line |

| Equity partner / JV | Full cash stack | You share profit | Partner may take 20%–40% |

| Transactional funding | Purchase only | Short use, no rehab funds | Works for wholesale, not a full flip |

Bottom line: I’d treat “100% financing” as a math problem, not a promise. If the deal does not leave room for fees, delays, and a 10% to 15% rehab cushion, the loan structure will not save it.

How Fix-and-Flip Loans Work and Where the Cash Gap Usually Comes From

A fix-and-flip loan is a short-term, interest-only bridge loan that usually runs 6 to 18 months. It’s asset-based, which means the lender looks hard at the property, the rehab plan, and the exit strategy. That setup explains why “no money down” often doesn’t mean no cash needed.

The loan usually covers two parts of the project: the purchase and the renovation. Purchase money is wired at closing. Rehab money doesn’t show up all at once. It’s held in escrow and released in stages, called draws, after an inspector confirms the work is done.

Purchase Price, Rehab Budget, Points, Interest Reserves, and Closing Costs

Most high-leverage programs cover most of the purchase price and 100% of the approved rehab budget, but the total loan still has to stay within the property’s ARV cap. So the shortfall often comes from costs the lender won’t pay up front, not from the purchase price itself.

| Expense | Usually Financed? | Typical Cost/Terms |

|---|---|---|

| Closing Costs | Rarely | $4,000–$8,000 |

| Interest Reserves | Rarely | $8,000–$15,000 |

| Origination Points | No - paid at closing | 2% to 5% of loan amount |

| Holding Costs | No | Monthly interest, taxes, insurance, and utilities |

Here’s where borrowers get tripped up: even “100% financing” can still mean bringing $20,000 to $45,000 in cash to close on a $300,000 deal once you add points, closing costs, and reserves.

Leverage Limits: LTC, LTV, and ARV Caps Explained

Loan-to-Cost (LTC) compares the loan amount to the total deal cost, meaning the purchase price plus the rehab budget. Loan-to-Value (LTV) here refers to the after-repair value cap, so it measures the loan against what the property is expected to be worth when the work is done.

Most lenders cap the total loan at 70% to 75% of the ARV. That cap matters more than the headline LTC in many deals. If the purchase and rehab numbers get too close to that limit, the lender cuts the loan amount, and the borrower has to cover the rest out of pocket. On paper, the leverage can look high. At the closing table, the gap still shows up.

Minimum Borrower Requirements for High-Leverage Loans

Once the leverage math makes sense, the next issue is what the lender wants from the borrower. For high-leverage deals, lenders usually want 6 to 12 months of carrying costs in liquid reserves. In plain English, they want proof that the borrower can keep the project afloat if the sale takes longer than planned.

At the deal level, lenders also tend to ask for:

- A documented rehab scope with line-item costs

- A clear exit strategy based on a realistic sale timeline or refinance plan

That’s a big reason fix-and-flip financing can sound lighter than it feels in practice. The loan may cover a large share of the deal, but the borrower still needs cash, reserves, and a plan that holds up under scrutiny.

sbb-itb-e7c549b

The Main 100% Financing Structures for Fix-and-Flip Investors

100% Fix-and-Flip Financing Options Compared: Costs, Coverage & Trade-Offs

Investors use a few different setups to cut down the cash they need at closing. Each one deals with the gap from LTC and ARV limits in its own way. The best fit comes down to a simple question: do you need money for the purchase, the rehab, or just a short-term bridge to close?

Hard Money Loans Plus Gap Funding or Dedicated 100% Products

One of the most common setups is a two-lender stack. A hard money lender covers 80% to 90% of the project cost, and a second lender fills the rest.

That extra gap money isn't cheap. It often costs 15% to 20% APR plus 2 to 3 points. Once you blend both loans together, the full stack usually lands around 13% to 16% APR.

Some lenders also offer a dedicated 100% LTC product that combines the purchase and rehab into one loan. That can make the deal simpler on paper. But the same borrower standards usually still apply, and ARV caps still control how much you can borrow.

Transactional Funding and Cross-Collateral Loans

Not every 100% structure funds the whole flip. Some only solve one part of the deal.

Transactional funding is short-term capital used for double-close wholesale deals. It usually lasts 24 to 48 hours and is meant to help with the acquisition only. It does not cover rehab.

Cross-collateral loans work differently. Instead of bringing cash for the down payment, the investor uses equity from another property as collateral. Since the lender has that extra backing, it may fund 100% of the new purchase.

That can help you close without new cash. But there's a catch: if the flip goes sideways, the property you pledged is on the line too.

Private Capital, Joint Ventures, and Partner-Backed Deals

When debt costs too much or isn't available, investors sometimes bring in an equity partner to fund the whole stack.

In this setup, a money partner pays for the deal and gets a share of the upside. That profit split is usually 20% to 40%.

You avoid piling on more loan costs, but you give up part of the profit if the flip works.

| Structure | What It Funds | Key Trade-Off |

|---|---|---|

| 100% LTC Hard Money | 100% purchase + 100% rehab | High borrower requirements; ARV caps apply |

| Gap Funding Stack | Up to 100% of total cost | Blended APR of 13–16%; coordination risk |

| Cross-Collateral | 100% of new acquisition | Pledged property is at risk |

| Equity Partner / JV | 100% of all capital needs | 20–40% profit share goes to partner |

| Transactional Funding | Purchase only, 24–48 hours | Not usable for rehab; wholesale use only |

Qualification Standards, Costs, and Risks in High-Leverage Flip Financing

Once the deal structure is in place, the next thing that matters is simple: can you qualify, and how much cash do you still need at closing?

Credit, Experience, Reserves, and Rehab Plan Requirements

True 100% financing usually goes to borrowers who already have a track record. In most cases, lenders want strong credit and 3 to 5 closed flips. For true 100% LTC approval, high-leverage lenders often look for a FICO score of 650 to 720+.

If you're a first-time investor, that doesn't always knock you out. But it does tend to lower your leverage. Many lenders cap newer borrowers at around 80% to 85% LTC unless an experienced contractor is part of the deal.

Lenders also want more than a rough rehab number scribbled on a page. They usually ask for a detailed line-item scope of work, not a lump-sum estimate. On top of that, they'll check that you're closing through an LLC or corporation and that you have builder's risk and general liability insurance in place.

And then there's reserves. Most lenders want to see 6 to 12 months of carrying costs sitting in liquid funds. That money is there to cover interest, utilities, and those annoying overruns that seem to show up right when the job should be wrapping up.

Those items don't just affect approval. They also shape what the deal costs from day one.

Rates, Points, Fees, and the Real Cost of No Money Down

“No money down” sounds great until you look at the settlement statement.

Even with a 100% LTC deal, borrowers still have to pay origination points, closing costs, and interest reserves out of pocket. On a $300,000 purchase with an $80,000 rehab budget, 3% origination points come out to about $11,400. Closing costs can add another $5,000 to $7,000. Six months of interest reserves can run $15,000 to $20,000. That puts total cash needed at closing between $31,400 and $38,400 before the first nail is pulled.

High-leverage programs often come with rates in the 10% to 13%+ range, plus 1 to 5 points in origination fees. That's the trade-off. You put less money down upfront, but the loan gets more expensive, and that cost eats into profit fast.

How High Leverage Changes the Deal

High leverage helps with upfront cash. It also makes the deal less forgiving.

If the appraisal comes in low, rehab costs jump, or the home sits on the market longer than planned, the lender's ARV cap can force you to bring in more cash and leave the project with less cushion for mistakes. That’s where a deal that looked fine on paper can get tight in a hurry.

Before signing anything, check at least five conservative comparable sales to make sure the project stays under the 70% to 75% ARV cap. It also helps to build a 10% to 15% contingency into the rehab budget. If the numbers only work in a best-case scenario, they probably don't work.

Less cash down means less room for error.

Conclusion: When 100% Fix-and-Flip Financing Makes Sense

100% fix-and-flip financing is all about structure, not free money. The best no-money-down setup protects your profit and still gives you some breathing room if the rehab takes longer, costs more, or the market cools off.

Once the ARV cap is clear, the next step is simple: figure out which structure covers the rest of the gap. That choice depends on your collateral, liquidity, and track record. If you have equity in a rental property, cross-collateralization may fit. If your credit is strong but cash is tight, gap funding may make more sense. And if you're newer to flipping and the deal has a healthy margin, bringing in an equity partner can be smarter than trying to push for a 100% LTC approval you may not get.

In most cases, the ARV cap is the part that holds everything in place. If your total project cost goes above 70% to 75% of ARV, you'll usually need to cover the difference no matter what the headline offer says.

The choice comes down to a few plain factors: deal quality, collateral strength, rehab difficulty, available cash, experience, fees, and how solid your exit plan looks.

| Decision Factor | What It Affects |

|---|---|

| ARV vs. total project cost | Whether the ARV cap means you need cash at closing |

| Experience | Access to 100% LTC programs |

| Liquidity | Lender approval and your ability to handle draw gaps and surprises |

| Collateral | Whether extra equity can reduce lender risk without bringing cash |

| Fee tolerance | Whether higher interest, points, and closing costs still leave enough profit |

| Exit plan | How closely the lender reviews your sale or DSCR refi plan |

If the deal only works under the best-case scenario, it doesn't work. Build in a 10% to 15% contingency, check conservative comps, and lock down the exit before you sign.

FAQs

Can I get a fix-and-flip loan with bad credit?

Yes, but your options may be more limited and the requirements stricter. Many 100% financing programs prefer a 720+ FICO score, but some will go as low as 620 to 650.

If your credit is on the lower side, lenders may ask for more cash reserves, steady income, or extra collateral. You’ll also need a strong project plan and a realistic ARV to show that the deal can pay back the loan.

What if the appraisal comes in below my ARV estimate?

If the appraisal comes in below your estimated ARV, your loan amount will probably shrink. Hard money lenders usually cap loans at 70% to 75% of ARV, so the appraisal often sets the ceiling on how much you can borrow.

That matters even if you have a 100% LTC deal. The lender will still use the lower ARV-based cap. When that happens, you can end up with a funding gap and may need to bring in your own cash to keep the deal alive.

How do rehab draws work during the project?

Rehab draws don't all come at closing. In most cases, the lender keeps your renovation funds in a reserve account and releases them in phases.

As the project moves forward, you send in draw requests tied to each milestone. That usually means paperwork like contractor invoices or inspection reports. Once the lender verifies the work, the money is released.

This setup helps protect the property. It also means you usually pay interest only on the funds that have already been drawn.