Hard Money Loans vs. DSCR Loans: Which Is Better for Investors?

If I need to close in days and fix a rough property, I look at hard money. If I want a long rental hold with lower monthly pressure, I look at a DSCR loan. That’s the short answer.

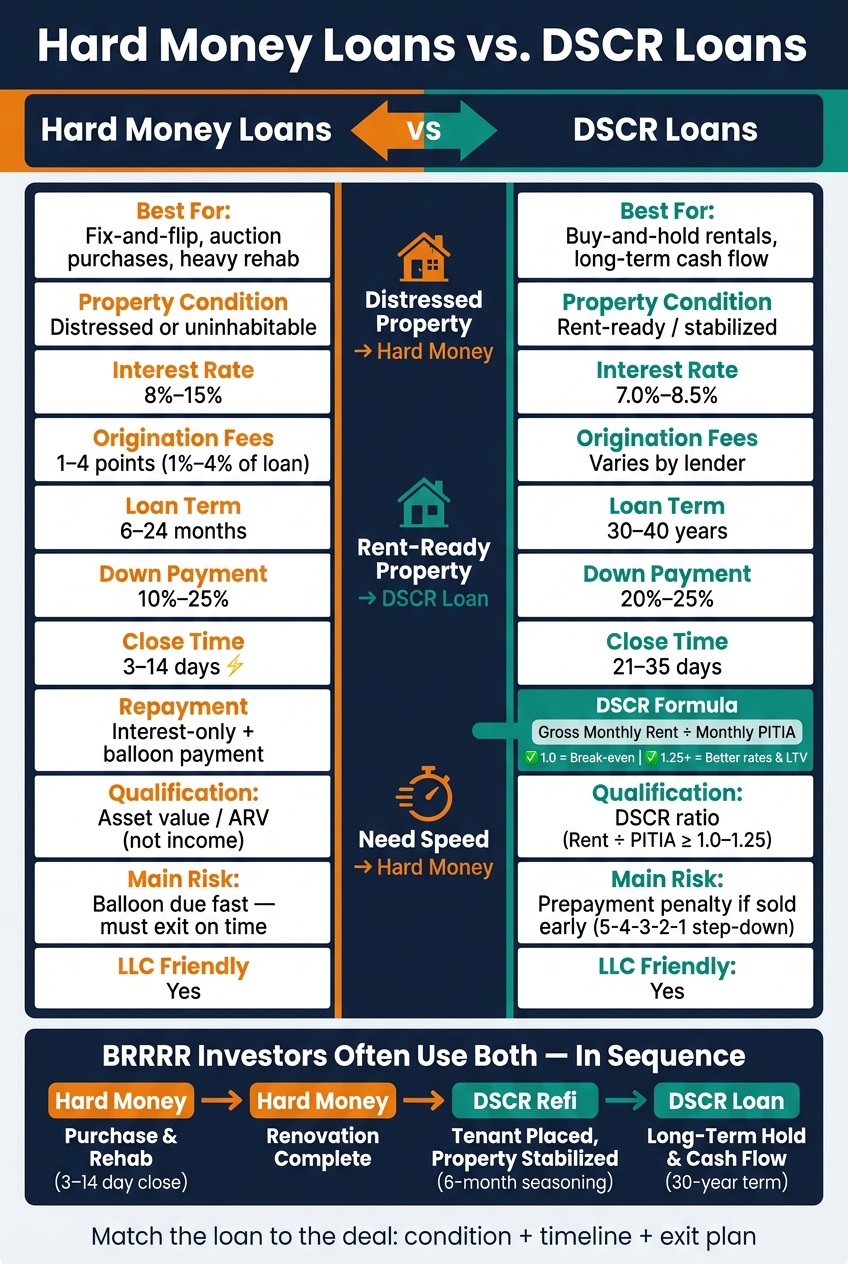

Here’s the simple breakdown:

- Hard money fits deals that need fast funding, rehab work, and a sale or refinance soon after closing.

- DSCR loans fit rent-ready properties where the monthly rent covers PITIA and I plan to hold the property.

- Hard money often comes with 8%–15% rates, 6–24 month terms, 1–4 points, and closings in 3–14 days.

- DSCR loans often come with 7.0%–8.5% rates, 30- to 40-year terms, 20%–25% down, and closings in about 21–35 days.

- The main decision points are property condition, time to close, hold period, down payment, docs, and exit plan.

- A lot of BRRRR investors use both: hard money first, then a DSCR refinance after rehab and lease-up.

Hard Money Loans vs. DSCR Loans: Side-by-Side Comparison for Real Estate Investors

COMPARE: Hard Money vs DSCR - Which is the Better Option for You?

sbb-itb-e7c549b

Quick Comparison

| Loan Type | Best For | Property Type | Close Time | Term | Main Risk |

|---|---|---|---|---|---|

| Hard Money | Fix-and-flip, auction, heavy rehab | Distressed or not rent-ready | 3–14 days | 6–24 months | Balloon due fast |

| DSCR Loan | Buy-and-hold rentals | Stabilized, income-producing | 21–35 days | 30–40 years | Prepay penalty if sold early |

My rule of thumb is simple: if the deal needs speed and work, hard money usually fits. If the property is stable and the rent works, DSCR usually fits better.

Below, I’ll break down the trade-offs in plain English so you can match the loan to the deal in front of you.

How Hard Money Loans Work for Real Estate Investors

For investors who need speed more than the lowest cost, hard money is a short-term tool. It’s property-based financing, which means lenders focus on the deal itself. They look at the as-is value, ARV, rehab budget, and exit plan - not your W-2s or tax returns.

That makes hard money a fit for properties that need heavy rehab and won’t qualify for long-term financing.

Typical Terms, Rates, Leverage, and Closing Speed

Hard money costs more than long-term financing. But that higher cost buys speed and more room to work.

| Feature | Typical Range |

|---|---|

| Interest Rate | 8%–15% |

| Origination Fees | 1–4 points (1%–4% of the loan amount) |

| Loan Term | 6–24 months |

| Down Payment | 10%–25% of the purchase price |

| Financing | Up to 90% of purchase price and 100% of approved rehab costs |

| Closing Speed | 3–14 days |

That fast closing window can make or break an auction deal or any other time-sensitive purchase. In this kind of loan, the exit plan matters just as much as the rate. A low rate won’t help much if the loan comes due before you can sell or refinance.

What Lenders Review and How Repayment Works

Underwriting usually centers on the property’s condition, the rehab budget, the ARV, the exit plan, and often your track record and available cash. Credit still plays a part, but it usually matters less than the deal itself. Some lenders accept scores near 550, while others focus almost entirely on the asset.

Rehab funds are often held in escrow and paid out through draws after inspections. That setup helps lenders check that the work is moving as planned.

Payments are usually interest-only, with the full principal due at maturity. Most investors pay off the loan through a sale or a refinance. That’s why the exit plan needs to be lined up before closing, not figured out halfway through the project.

If the property is already stable and producing rent, the next section shows how DSCR loans work.

How DSCR Loans Work for Rental Property Investors

A DSCR loan is an investment-property mortgage that qualifies the deal based on rent, not your personal income.

That can be a big deal for rental investors whose tax returns don’t show the full picture of property cash flow. It matters most when the plan is simple: hold the property, keep it rented, and let the rent cover the debt.

DSCR Formula, Loan Terms, and Down Payment Requirements

DSCR = Gross Monthly Rent ÷ Monthly PITIA

PITIA stands for Principal, Interest, Taxes, Insurance, and HOA dues. A DSCR of 1.0 means the rent covers the full monthly payment. A DSCR of 1.25 means rent is 25% higher than the payment. Most lenders want to see a minimum DSCR between 1.0 and 1.25. If the property hits 1.25 or more, you may qualify for better rates and higher LTV tiers.

Rates usually fall between 7.0% and 8.5%, and terms often include 30- to 40-year fixed options, ARMs, and in some cases interest-only setups.

Down payments are often 20% to 25%. Many programs also come with prepayment penalties, often in a 3- or 5-year step-down format. So if you may sell early, it’s smart to read that part closely.

Property Types and Borrower Profiles That Fit DSCR Loans

DSCR loans can be used for stabilized rental properties, including:

- 1–4 unit properties

- Condos

- Townhomes

- Small multifamily

- Some short-term rentals

This is one area where DSCR loans can give investors more room. Conventional loans are usually capped at 10 financed properties. DSCR loans, on the other hand, generally don’t limit how many financed properties you can have. You can also close in the name of an LLC or another business entity, which many investors use for liability protection.

For BRRRR deals, DSCR loans usually make sense after the rehab is done and the property is rented and stabilized. Cash-out refinances often call for 6 months of seasoning. That’s the point where DSCR loans often start to look better than hard money for longer holds and steadier payments.

With both loan types defined, the next section compares cost, speed, and exit strategy head-to-head.

Hard Money Loans vs. DSCR Loans: Side-by-Side Comparison

Here’s the direct comparison.

Comparison Table: Rates, Terms, Speed, Documentation, and Exit Strategy

| Feature | Hard Money Loan | DSCR Loan |

|---|---|---|

| Qualification Method | Asset value / ARV | Property cash flow (DSCR ratio) |

| Property Condition | Distressed / Uninhabitable | Rent-ready / Stabilized |

| Time to Close | 3–14 days | 21–35 days |

| Repayment Structure | Interest-only with balloon payment | Fully amortizing over 30 years |

| Exit Strategy | Fast exit - sell or refinance | Long-term ownership / cash flow |

The key difference comes down to hold period.

And the gap between these loan types isn’t just about rate. It’s about how the loan works as time passes.

How Cost and Risk Shift Based on How Long You Hold the Property

Hard money can make sense when speed matters more than rate. But there’s a catch: these loans come with firm maturity dates. If you miss your exit window, you may get hit with extension fees or even default.

DSCR loans bring a different kind of risk. On that side, the issue is often prepayment penalties. Many use a step-down setup like 5-4-3-2-1 over five years. So if you sell a rental too soon, that penalty can take a noticeable bite out of your proceeds.

Put simply, short-hold risk tends to sit with hard money, while early-sale penalty risk tends to sit with DSCR.

That’s why a lot of investors use both loan types on the same deal, just at different stages.

Using Both Loan Types Together: Rehab First, DSCR Refinance Later

BRRRR investors often start with hard money for the rehab phase, then refinance into a DSCR loan once the property is stabilized. Hard money covers the value-add stage. DSCR takes over for the rental hold.

That handoff is the whole play: short-term rehab financing first, long-term rental financing second.

Which Loan Fits Your Deal? A Simple Decision Framework

Now that both loan types are on the table, the decision gets pretty simple: look at the property’s condition, your timeline, and how you plan to exit the deal.

Choose Hard Money When Speed, Rehab, or a Fast Exit Is the Priority

Hard money makes sense when you need to close fast and a conventional or DSCR loan just won’t move in time. It also fits deals where the property isn’t ready for long-term rental financing yet. That can happen when you’re buying at auction, taking over an assigned contract, or picking up a foreclosure that needs major repairs.

If the property is already stabilized, that’s usually when the choice starts leaning toward DSCR financing.

Choose a DSCR Loan When Stable Cash Flow and Long-Term Ownership Are the Goal

A DSCR loan makes more sense once the property is producing steady rent and you plan to keep it for the long haul. These loans are built for long-term ownership, usually with 30-year terms and no personal income verification.

Key Takeaways for Investors

The choice mostly comes down to property condition and how long you plan to hold.

Here’s the simplest way to match the loan to the deal:

| Situation | Best Fit |

|---|---|

| Distressed property or fast close | Hard money |

| Flip or sale within 12 months | Hard money |

| Rent-ready property, long-term hold | DSCR loan |

| BRRRR rehab-to-rent strategy | Hard money → DSCR refinance |

FAQs

Can I use a DSCR loan for a property that still needs repairs?

Generally, no. DSCR loans are built for stabilized rental properties that are already bringing in steady income. If a property needs major repairs, it often isn’t habitable and usually isn’t collecting steady rent. That means it often won’t qualify.

Most investors use hard money loans to buy the property and pay for the rehab. Once the work is done, the property is leased, and the rental income is steady, they often refinance into a long-term DSCR loan.

What happens if I can’t refinance or sell before a hard money loan comes due?

If you can’t refinance or sell before your hard money loan matures, you could end up in default or even foreclosure. That’s because hard money loans are short-term bridge financing, and the clock moves fast.

To lower that risk, reach out to your lender as early as possible. Some lenders may offer an extension or another bridge option. Hard money loans are built for quick turnarounds, so any delay can put serious pressure on your finances and eat into your equity.

When should I switch from hard money to a DSCR loan in a BRRRR deal?

In a BRRRR deal, you usually move from a hard money loan to a DSCR loan after the property is fixed up, rented out, and has met the lender’s seasoning rule.

Hard money pays for the purchase and rehab at the start. Then, once the property is stable and producing rent, a DSCR loan can step in with long-term, fixed-rate financing to pay off the hard money loan.

Most lenders want a seasoning period of 3 to 6 months.