How to Get a DSCR Loan: A Step-by-Step Guide for Real Estate Investors

A DSCR loan comes down to one thing: does the property’s rent cover the monthly payment? If the answer is yes, you may qualify without using your W-2s or tax returns as the main approval test.

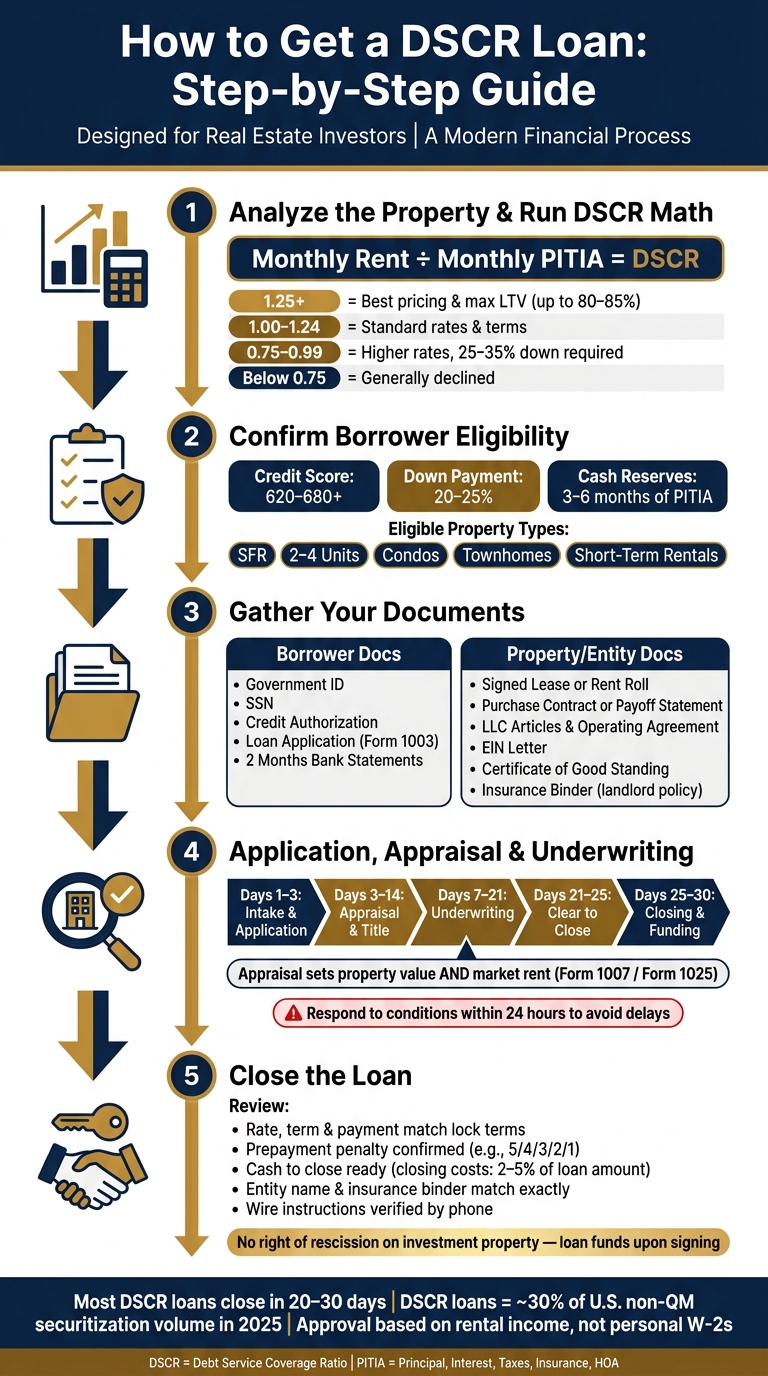

Here’s the short version: I’d check the property’s DSCR ratio, make sure my credit score, down payment, and cash reserves fit lender rules, gather my lease, bank statements, LLC documents, and insurance, then stay on top of appraisal, underwriting, and closing conditions. In many cases, DSCR loans close in about 20 to 30 days, and these loans made up about 30% of U.S. non-QM securitization volume in 2025.

Before I apply, I’d want these points lined up:

- Property type: non-owner-occupied rental only

- DSCR target: often 1.00+, with 1.25+ getting better pricing

- Credit score: often 620 to 680+

- Down payment: often 20% to 25%

- Reserves: often 3 to 6 months of PITIA

- Rent support: lease, rent roll, or appraisal rent forms like 1007 or 1025

- Common delays: LLC issues, expired statements, slow insurance, title mismatches

If I were sizing up a deal fast, I’d start here: monthly rent ÷ monthly PITIA. That single number tells me whether the file is likely to work before I spend money on appraisal and underwriting.

The rest of the guide walks through that process from first deal review to funded loan.

How to Get a DSCR Loan: Step-by-Step Process for Real Estate Investors

📊How to Get a DSCR Loan for Your First Rental Property | Daily Rates LIVE

sbb-itb-e7c549b

1. DSCR Loan Basics and Who Can Qualify

A DSCR loan is a non-QM mortgage that’s underwritten based on a rental property’s cash flow, not the borrower’s personal income. Instead of digging into W-2s or tax returns first, lenders look at how the property performs. They compare gross rent to monthly PITIA: principal, interest, taxes, insurance, and HOA dues.

That comparison helps lenders decide a simple but big question: Does this property bring in enough rent to support the loan? The answer affects both approval and loan terms.

Most lenders also want to see a few baseline items from the borrower, including:

- A 620–680 credit score

- 20%–25% down

- 3–6 months of PITIA reserves

Here’s how DSCR levels usually line up with approval status and pricing:

| DSCR Ratio | Qualification Status | Typical Terms |

|---|---|---|

| 1.25 or higher | Excellent | Best pricing and max LTV (up to 80–85%) |

| 1.00 – 1.24 | Standard | Standard market rates and terms |

| 0.75 – 0.99 | Specialty | Higher rates; requires 25–35% down payment |

| Below 0.75 | Generally Declined | Rarely qualifies without significant compensating factors |

A 1.25+ DSCR usually gets the strongest terms. A 1.00 DSCR is often still financeable. If the ratio falls in the 0.75–0.99 range, lenders often want more money down and charge higher rates.

What counts as an eligible investment property

DSCR loans are for non-owner-occupied investment properties only. You can’t use one for a primary home.

Eligible property types usually include single-family rentals (SFR), 2–4 unit small multifamily, condos, townhomes, and short-term rentals like Airbnb or Vrbo. If the property is vacant, lenders may use an appraisal-based market rent estimate, such as Form 1007 for single-family homes or Form 1025 for 2–4 unit properties.

Who DSCR loans work best for

DSCR loans tend to work well for self-employed investors, 1099 earners, and portfolio landlords who want underwriting tied to the property rather than personal income.

Before you apply, it helps to pin down the property type, estimate the rent, and run the DSCR. That gives you a much clearer read on whether the deal works on paper.

2. How to Analyze a Property and Estimate DSCR Before You Apply

Before you pay for an appraisal, run a conservative DSCR estimate:

Monthly Gross Rental Income ÷ PITIA

It’s a simple way to screen a deal before you spend money on underwriting and appraisal. Use a realistic PITIA number. Call the county assessor for the current tax bill, get a preliminary insurance quote, and add HOA dues if the property has them. A 1.0x DSCR means the property is breaking even. A 1.25x DSCR will often get you better pricing. If the deal falls short of your target, change the price, down payment, or rent assumptions before you apply.

Here’s what that looks like in practice. Say you’re buying a single-family rental for $320,000 with a $240,000 loan at 7% interest. Your monthly principal and interest would be $1,594. Add $285 for taxes and $125 for insurance, and your total PITIA becomes $2,004. If the appraiser’s market rent comes in at $2,000, your DSCR is 1.0x exactly, which is the floor for many lenders.

That small gap can change your loan cost in a big way. A 1.0x DSCR might come with rates around 8.5%–9.5%, while a 1.25x DSCR can bring rates down to 7.0%–8.0%. On a $400,000 loan, that difference can mean $200–$400 less per month in interest costs.

How lenders calculate rental income for DSCR

Occupied, vacant, and short-term rentals are not treated the same way.

For occupied properties, lenders usually use the lower of:

- The actual signed lease

- The appraiser-backed market rent estimate on Form 1007 for single-family properties or Form 1025 for 2–4 unit properties

If the tenant is paying under market, the lower lease amount is usually the number that counts.

"Actual lease income often results in a more favorable DSCR calculation than appraiser estimates. And if the Form 1007 rent is within 20% of your actual lease, we might be able to use the higher figure." - Eric Krattenstein, AHL

For vacant or newly acquired properties, lenders lean on the appraiser’s market rent schedule because there’s no current lease to use. If the appraised rent lands below your estimate, your DSCR drops with it.

Short-term rentals like Airbnb or Vrbo are often underwritten more cautiously. Many lenders apply a 20% haircut to gross booking revenue, so they use only 80% of projected income in the DSCR calculation. Some also want 12 months of payout history from a platform like Airbnb or VRBO to confirm the income.

| Income Source | What Lenders Use | Typical Income Adjustment |

|---|---|---|

| Long-term lease (at market) | Lesser of lease or appraiser's rent | 5%–10% |

| Vacant property | Appraiser's market rent (Form 1007/1025) | 10%–15% |

| Short-term rental with history | 12-month average net income | 20%–30% |

| Short-term rental with AirDNA estimate | AirDNA net income projection | 25%–35% |

How to decide if the deal is financeable

Once you’ve run the DSCR estimate, use it as a first-pass filter.

A deal at 1.25x or above is in good shape and is more likely to qualify for better pricing. If it comes in between 1.0x and 1.24x, many lenders may still look at it, but pricing can get tighter. If it’s below 1.0x, you’ll likely need to rework the deal before applying.

The most practical fixes are pretty straightforward:

- Put more money down

- Negotiate a lower purchase price

- Show higher actual rents with a signed lease

It also helps to use conservative rent comps from the start. That lowers the chance of a weak appraisal and a DSCR that falls apart at underwriting.

Once the numbers make sense, the next step is reviewing investor loan programs and the entity paperwork the lender will check.

3. Documents You Need to Apply for a DSCR Loan

Once the rent math checks out, the lender moves on to the rest of the file. They want to verify the borrower entity, cash reserves, lease terms, and insurance. So when your DSCR estimate looks good, start pulling documents right away. Getting organized early helps you stay on that usual 20- to 30-day closing timeline.

Most DSCR files need the same core paperwork:

- A government-issued ID

- Your Social Security number

- A signed credit authorization

- A completed loan application, either Form 1003 or the lender’s version

- Two full months of bank or brokerage statements, including every page, to verify your down payment and reserves

You’ll also need deal-specific items. If you’re buying, include the executed purchase contract. If you’re refinancing, provide your current mortgage statement and payoff demand. It also helps to order a landlord policy early with at least six months of rental loss coverage.

For occupied properties, include the signed lease. For multi-unit properties, include a rent roll with tenant names, lease dates, and monthly rents.

The file needs to tell one clear story: lease, rent roll, appraisal rent, insurance, taxes, and DSCR all need to line up.

Entity vesting and LLC paperwork

If you plan to close in an LLC or corporation, the lender will usually ask for:

- Articles of Organization

- A fully signed Operating Agreement

- An EIN confirmation letter

- A Certificate of Good Standing from the Secretary of State

If your operating agreement doesn’t spell out borrowing authority, add a borrowing resolution too. In most cases, the managing member will still need to sign a personal guarantee.

One thing that trips people up? Timing. Form the LLC before you apply, and settle the vesting structure at the start. Changing title from your personal name to an LLC after submission can slow the file down for no good reason.

Common issues that delay approval

Most approval delays are easy to spot ahead of time. The usual culprits are late deposits, weak reserves, lease income that doesn’t match the file, missing signatures, and slow insurance quotes.

If you want the process to move, clean those up early. Source any large unexplained deposits. Make sure the lease matches the rent schedule. And order insurance as soon as you’re under contract.

With the file in place, the lender can move into appraisal and underwriting.

4. Application, Underwriting, and Appraisal

Once you have the rent estimate and property details, the lender moves the file from early screening into formal underwriting. At that point, the deal starts to look much more like a live transaction than a rough pre-check.

First, the lender gets the file organized, reviews the deal, pulls credit, and gives initial pricing before formal submission. Then comes the full application packet based on the lender's required format.

After submission, the lender pulls credit and orders the appraisal. Underwriting usually focuses on three things:

- borrower qualification, including credit and liquidity

- property value, condition, and DSCR

- document completeness

If any part is missing or doesn't line up, you'll get a condition that has to be cleared before the file can move ahead.

What happens during appraisal and rent review

This is the stage where the appraisal does a lot of heavy lifting. It sets the property's value and supports the market rent figure. That rent then feeds straight into the DSCR calculation.

If the appraisal comes in weak, the deal can change fast. You might need more cash down, get less leverage, or lose the deal altogether. Property condition matters just as much. Most DSCR lenders want a C4 condition rating or better, and deferred maintenance can knock a property out of the running until repairs are done.

Short-term rental income also gets a stricter look. When lenders use AirDNA data, they often apply a vacancy factor of about 25% to 35%.

Typical timeline from application to approval

Appraisals usually take 7 to 14 days, though that depends on the market. Underwriting runs at the same time when it can, and many files reach conditional approval in 14 to 21 days. Common conditions include updated bank statements, a final insurance binder, or clear title.

One small delay can throw off the whole closing calendar. Responding within 24 hours after you get conditions is critical, since slow replies are a common reason investors miss the closing date.

| Stage | Typical Timeline |

|---|---|

| Intake & Application | Days 1–3 |

| Appraisal & Title | Days 3–14 |

| Underwriting | Days 7–21 |

| Clear to close | Days 21–25 |

| Closing & Funding | Days 25–30 |

At this point, any open item usually ties back to appraisal, title, insurance, or reserve verification. Title and insurance must clear before the loan can fund. Once underwriting signs off on those last issues, the file moves to final document review and closing.

5. Closing the Loan and Avoiding Last-Minute Problems

Once underwriting clears the last conditions, the file moves to closing. At this point, the main job is simple: make sure the documents you sign match the loan that was approved. If something still goes sideways here, it usually ties back to title, insurance, entity paperwork, or a cash-to-close mismatch.

The Closing Disclosure must arrive at least three business days before closing. Don’t just glance at it. Read it line by line before you sit down to sign. With a DSCR loan on an investment property, there is no three-day right of rescission like there is with a primary residence refinance, so the loan can fund as soon as you sign. That puts a lot more weight on the review you do before closing day.

What to review before signing

This is the time to catch errors before money moves. Focus on these items:

- Rate, term, and payment: Check that the interest rate matches your locked rate, the loan term is right, and the monthly payment lines up with what you were quoted. Put the final terms next to the lock terms and compare them directly.

- Prepayment penalty: DSCR loans often come with step-down prepayment penalties, such as 5/4/3/2/1 or 3/2/1. Make sure the setup on the Closing Disclosure matches what you saw at application.

- Cash to close: Review the full amount due at closing, including your down payment and closing costs. DSCR loan closing costs usually land between 2% and 5% of the loan amount. Have the full wire ready 24 to 48 hours before closing.

- Entity and insurance match: If you’re closing in an LLC, confirm the entity name matches the legal registration exactly. Even a small mismatch can slow things down. Also check that the authorized signer is correct, the Certificate of Good Standing is dated within 90 days of closing, and the insurance binder matches the loan file and closing date.

- Wire verification:

"Verify wire instructions by phone using a known number." - Eric Krattenstein, American Heritage Lending

If the Closing Disclosure matches the approved terms and your title, insurance, and cash-to-close items are in order, the loan can fund without delay. After funding, confirm the recording, save the final loan package, and leave your reserve balance alone so you have cash on hand for repairs or vacancy.

Conclusion: From Rental Analysis to Funded DSCR Financing

Getting a DSCR loan follows a pretty direct path: confirm the property is eligible, run the DSCR math before you apply, gather documents early, stay on top of appraisal and underwriting requests, and keep your funds and title paperwork clean all the way through closing. Most delays don’t come out of nowhere. They usually start with something small that got missed earlier.

The main draw of this loan type is simple. Approval leans on the property’s rental income and your credit profile, not your personal income documents. For investors with a deal backed by solid rental cash flow, that can make DSCR financing a practical way to get to the closing table.

FAQs

Can I get a DSCR loan with no current tenant?

Yes. You can qualify for a DSCR loan on a vacant property.

If there isn’t a tenant in place, lenders will usually look at a market rent analysis or rental survey to estimate the property’s income. In many cases, that comes from an appraiser’s Form 1007. They use that estimate to calculate the DSCR.

It’s smart to tell your lender early if the property is vacant. Some lenders ask for specific paperwork or lease schedules during underwriting.

What if my DSCR is below 1.00?

A DSCR below 1.00 means the property’s rental income doesn’t fully cover the mortgage payment.

Most lenders want to see at least 1.00. That said, some specialty programs may go as low as 0.75.

In practice, a lower DSCR usually leads to stricter loan terms. That can mean:

- A larger down payment

- Higher interest rates

- More cash reserves

- Prior investment property experience

You may be able to improve your DSCR with a larger down payment, a rate buydown, or higher rent.

Can I close a DSCR loan in an LLC?

Yes. Most lenders want to close a DSCR loan in an LLC. The main reason is asset protection. It also helps keep personal and business finances separate, which makes the setup cleaner from the start.

In most cases, you’ll need a few core documents:

- Articles of organization

- Operating agreement that shows ownership percentages

- EIN confirmation letter

- Certificate of good standing

One thing catches many borrowers off guard: even when the LLC is the borrower, many lenders still ask for a personal guarantee from the managing member.