Interest-Only DSCR Loans: How They Boost Cash Flow on Rental Properties

An interest-only DSCR loan can lower your monthly payment by 20% to 30%, which may improve cash flow and help a rental deal qualify. But there’s a tradeoff: when the interest-only period ends, the payment can jump by 25% to 55%, and you won’t build equity through principal paydown during that time.

Here’s the short version:

- I use interest-only DSCR loans when the goal is to keep monthly payments lower early in the hold

- They can improve DSCR because lenders compare rent to monthly PITIA

- On a $500,000 loan at 6.5%, the gap can be about $452 per month or $5,424 per year

- In one sample deal, cash flow after PITIA went from $239 to $417 with an IO structure

- The setup can fit buy-and-hold, BRRRR, and short-term rental deals

- The main risk is the reset payment after the IO window ends

- I’d only use it if the deal still works on the later principal-and-interest payment, not just the lower starting payment

If you want the plain-English takeaway, it’s this: IO DSCR loans can give you more cash now, but they push part of the bill into the future. That can help in a tight deal, but only if you’ve already checked reserves, rent growth, prepayment terms, and your refinance or sale plan.

Interest-Only vs. Fully Amortizing DSCR Loans: Cash Flow & Cost Comparison

What is an Interest-Only DSCR Loan?

Quick Comparison

| Loan Type | Monthly Payment at Start | DSCR Effect | Equity Build During Early Years | Payment Later | Best Use Case |

|---|---|---|---|---|---|

| Interest-Only DSCR | Lower | Often higher | No principal paydown | Higher after IO period ends | Tight cash-flow deals, rehab/lease-up, seasonal rent |

| Fully Amortizing DSCR | Higher | Often lower | Principal paid from month one | More stable | Long holds where payment stability matters most |

Bottom line: I’d look at an interest-only DSCR loan as a cash-flow tool, not a long-term fix.

How DSCR and Interest-Only Payments Work

What DSCR Means on a Rental Property Loan

To understand why IO loans can help, start with the way lenders judge a property's ability to carry its debt.

DSCR, or Debt Service Coverage Ratio, shows whether the rental income is enough to cover the loan payment. Lenders use it to see if the property can pay for itself. With DSCR loans, the focus is more on the property's cash flow than on personal income paperwork.

The formula is simple:

DSCR = Gross Monthly Rental Income ÷ Total Monthly PITIA

PITIA stands for principal, interest, taxes, insurance, and HOA dues. A DSCR of 1.00 means the rent exactly matches the monthly debt service. Most lenders want to see a ratio between 1.00 and 1.25, although some loan programs will go lower if the borrower puts more money down.

That last part matters. If monthly debt service drops, the DSCR goes up. And when that happens, more cash stays in your pocket after the mortgage is paid.

Fully Amortizing vs. Interest-Only DSCR Loan Payments

A fully amortizing 30-year DSCR loan includes both principal and interest in every payment from the start.

An interest-only DSCR loan works another way. During the IO period, the payment covers only the interest. That cuts monthly debt service. Once the IO period ends, the loan resets, and the remaining balance gets paid off over the rest of the term. For a property that needs better month-to-month cash flow, that shift can make a big difference.

Interest-only payments are usually 20% to 30% lower than fully amortizing payments on the same loan amount.

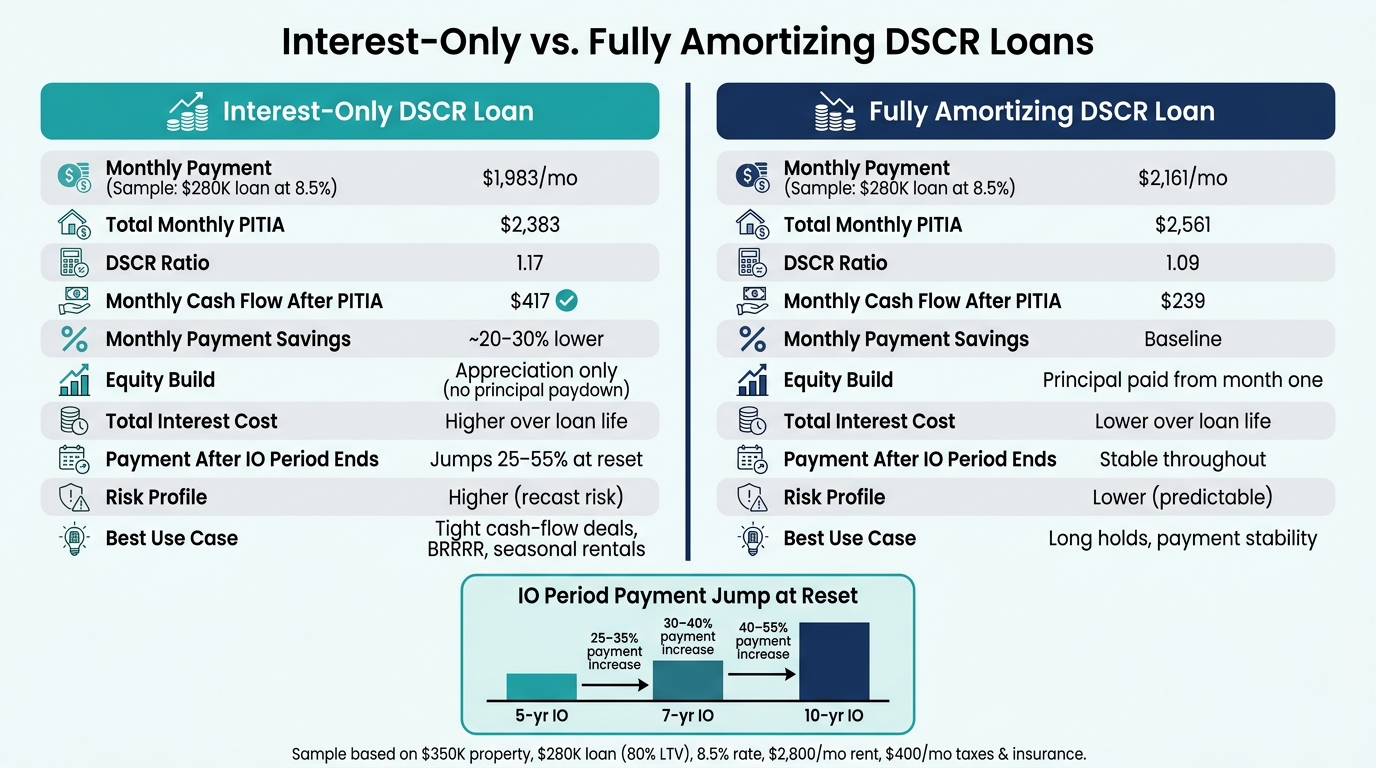

| IO Period | Remaining Amortization | Typical Payment Increase |

|---|---|---|

| 5 Years | 25 Years | ~25–35% |

| 7 Years | 23 Years | ~30–40% |

| 10 Years | 20 Years | ~40–55% |

There is one catch: not every lender looks at the payment the same way. Some underwrite based on the IO payment itself. Others use a stress test with a fully amortizing payment instead. That lower IO payment is what sets up the cash-flow example in the next section.

sbb-itb-e7c549b

How Interest-Only DSCR Loans Increase Monthly Cash Flow

Payment and Cash-Flow Example for a Long-Term Rental

Here’s the cleanest way to look at it. In this sample single-family rental, the purchase price is $350,000, the loan amount is $280,000 at 80% LTV, and monthly rent is $2,800:

| Feature | Interest-Only (10-yr IO) | Fully Amortizing (30-yr) |

|---|---|---|

| Interest Rate | 8.5% | 8.5% |

| Monthly Payment | $1,983 | $2,161 |

| Taxes + Insurance | $400 | $400 |

| Total Monthly PITIA | $2,383 | $2,561 |

| DSCR Ratio | 1.17 | 1.09 |

| Cash Flow After PITIA | $417 | $239 |

Note: Both columns use the same interest rate so the comparison isolates the effect of the IO structure, not a rate difference.

With the interest-only loan, the property throws off $178 more per month.

That’s the main draw. The payment is lower, so more rent stays in your pocket during the IO window. On the flip side, the fully amortizing loan starts paying down principal from month one, while the IO loan does not. So this is a trade: more cash now versus faster equity build-up now.

That extra monthly room can make a big difference when a rental needs a little breathing space early on.

Why the DSCR Can Improve During the Interest-Only Period

DSCR improves when debt service drops and rent stays the same. Pretty simple.

For example, a property with a 0.94 DSCR on a standard amortizing loan can jump to a 1.16 DSCR with an IO setup. That kind of shift can move a shaky deal into a lender’s approval range.

Of course, lenders don’t ignore the risk. Some may balance out the lower payment by asking for stronger borrower stats, such as credit scores around 680–720+, lower leverage, or a higher minimum DSCR target.

How Investors Can Use the Monthly Payment Savings

The smartest way to view IO savings is as reserve money, not spare cash to burn.

That lower payment can help investors:

- build cash reserves

- cover rehab carry costs

- handle seasonal dips in income

- set aside funds for future down payments or portfolio growth goals

For buy-and-hold investors, keeping a 6–12 month PITIA cushion can help cover vacancies and surprise repairs without reaching for outside capital.

For BRRRR investors, lower IO payments cut carrying costs during rehab and lease-up. That leaves more money available for the renovation budget.

For short-term rental owners, the lower payment can act like a buffer during slow seasons, when occupancy falls and income gets less steady.

The key point is simple: IO can give a deal more room upfront. What matters next is whether the numbers still hold up once the interest-only period ends.

When This Strategy Works and What to Watch For

If the lower payment helps get the deal done, the next step is simple: check whether the loan still makes sense once the IO period ends.

Best-Fit Scenarios: Buy-and-Hold, BRRRR, and Short-Term Rentals

Use IO when the lower payment solves a thin deal or helps protect cash flow in the near term.

Buy-and-hold investors: IO can help keep DSCR above the lender’s minimum without burning through reserves.

BRRRR investors: IO often fits during rehab and lease-up, when income hasn’t stabilized yet. Some investors also use IO on the refinance step to keep debt service low and increase cash-out proceeds.

Short-term rental owners: IO can help when seasonal income makes a fixed monthly payment feel too tight.

Eligible properties include SFRs, 2–4 units, condos, and townhomes.

Of course, that lower payment comes at a price.

Tradeoffs: Higher Total Interest Cost, Slower Principal Paydown, and Payment Increases

The big risk is the recast payment jump when the IO period ends. That’s the moment the loan switches to principal-and-interest payments on the remaining balance over a shorter timeline. On a 10-year IO loan, for example, you’re left with 20 years of amortization instead of 30. That can drive payments up by 40% to 55%. If rents don’t grow enough to cover that jump, cash flow can get squeezed fast.

A fully amortizing loan chips away at principal every month. IO doesn’t. So if you choose IO, your equity growth depends on appreciation or extra principal payments you make on your own.

| Feature | Interest-Only DSCR | Fully Amortizing DSCR |

|---|---|---|

| Monthly Cash Flow | Higher; payments are typically 20% to 30% lower | Lower; includes principal paydown |

| Total Interest Cost | Higher over the life of the loan | Lower |

| Equity Build | Appreciation only; no amortization | Passive build through monthly payments |

| Risk Profile | Higher; recast payment jump at reset | Lower; predictable payments |

That’s why the upfront payment isn’t the only thing that matters. Qualification rules and exit timing matter just as much.

Qualification Standards and Exit Plan Stress-Testing

IO DSCR loans often call for a stronger borrower profile, especially if you want a longer IO period. In plain English, expect better credit, lower leverage, and 6–12 months of PITIA reserves.

The most important stress test is simple: run the deal using the fully amortizing payment, not just the IO payment. If the numbers only work during the IO window and fall apart once amortization starts, that’s a shaky deal.

It also pays to review the prepayment schedule before you line up a refinance or sale. Many investors start looking at refinance paths 12–18 months before the IO window closes.

For the exit plan, model 2% to 3% rent growth and factor in higher taxes and insurance too.

Conclusion: Deciding if an Interest-Only DSCR Loan Fits Your Property

An interest-only DSCR loan is a cash-flow tool, not a permanent fix. It can cut monthly debt service by 20% to 30%, which can help keep more cash in the deal for buy-and-hold, BRRRR, and seasonal rental plays.

But here's the catch: the setup only makes sense if the payment still works after the IO period ends. That reset is where plenty of deals start to look less comfortable.

A Short Decision Checklist Before You Choose

Use these five checks before you lock the loan:

- Compare the payments side by side. Run the IO payment and the fully amortizing payment. If the deal only works during the IO window, pause and look at it hard before closing.

- Run DSCR on the lender's qualifying rent. Make sure you know whether the lender underwrites the loan using the IO payment, a fully amortizing payment, or both.

- Model the reset payment before closing. Know exactly what the payment becomes once amortization kicks in, and make sure the deal still holds up at that figure.

- Check reserve requirements before closing. Plan for that cash need well ahead of time.

- Match the IO period and prepayment terms to your hold period. IO tends to work best when the loan setup lines up with your timeline for a refinance or sale.

If all five checks hold up, IO may be the right fit for this deal. If not, a fully amortizing DSCR loan offers more predictable payments and passive equity growth from day one.

FAQs

Are interest-only DSCR loans harder to qualify for?

Not always. In many cases, interest-only DSCR loans are easier to qualify for than fully amortizing loans because the lower monthly payment can improve your DSCR.

That said, some programs set a higher minimum FICO score for interest-only options. They may also add a small rate premium, usually 0.125% to 0.375%.

How do I know if the payment reset will work for my deal?

Model the amortizing payment that kicks in when the interest-only period ends. Since the loan balance doesn’t shrink during that stretch, the payment goes up when the loan resets.

That jump can sneak up on people. So run the numbers now and make sure the property still cash-flows once the higher payment starts. It also helps to budget for that increase ahead of time and go in with a clear exit plan, like selling or refinancing.

Two habits can make the shift easier:

- Track rent growth

- Keep cash reserves

Those steps can give you more room to handle the reset without getting squeezed.

Should I choose interest-only or fully amortizing for a rental property?

It depends on your goals and how much risk you can live with.

Interest-only can help in the early years. It may boost cash flow, cut debt service, and improve DSCR. That can be useful if you expect to sell or refinance before the interest-only period ends.

Fully amortizing is usually the better fit for a steady long-term hold. You pay down principal over time, build equity, and avoid the payment jump that often hits when the interest-only period expires.

Before you choose, calculate DSCR both ways.