Investment Property Loan Requirements: What Lenders Actually Look For

Most investment property loan denials come down to four things: low credit, not enough cash, weak rent coverage, or a property that isn’t ready to rent.

If I had to boil this article down to one takeaway, it would be this: lenders are not just asking whether you can buy the property. They’re asking whether you, the property, and the loan setup all make sense together.

Before I apply, I’d want to check these points first:

- Credit: many programs start around 620 to 680

- Down payment: often 20% to 25%

- Reserves: often 3 to 12 months of PITIA after closing

- Cash flow: many lenders want around 1.00 to 1.25 DSCR

- Property condition: standard rental loans usually want the home rent-ready

- Loan fit: full-doc, DSCR, bank statement, bridge, and flip loans all use different rules

A deal can look fine at first and still fail if several weak spots stack up at once. A lower score, thin reserves, and a high LTV may each be workable alone, but together they can kill approval.

Here’s the short version of what lenders check:

| Area | What they focus on | Common problem |

|---|---|---|

| Borrower | Credit, cash, reserves, income | Low FICO, thin liquidity |

| Property | Appraisal, rent, DSCR, condition | Low rent estimate, DSCR under 1.00 |

| Deal | LTV, rehab scope, exit plan | Too much leverage, weak refinance or sale plan |

If I’m trying to judge approval odds fast, I’d start there before filling out any application.

How to Qualify for an Investment Property Using Rental Income

Understanding the fundamentals of investment property loans is the first step toward leveraging rental income for qualification.

sbb-itb-e7c549b

Borrower Strength: What Lenders Check First

Borrower strength is the first screen. If the borrower gets through that step, the lender moves on to the property's value, rent, and cash flow.

Credit Score, Credit History, and Recent Negative Marks

For conventional investment loans, the starting point is often a 680 credit score. DSCR and non-QM loans usually begin at 640 for purchases and 660 for refinances or cash-out deals.

Your score doesn't just affect approval. It also shapes LTV and pricing. Borrowers with 740+ can often get up to 85% LTV on a single-family rental. Drop below 680, and many DSCR programs pull back to around 65% to 70% LTV, which means bringing more cash to closing.

Lenders also take a harder look at recent credit issues on investment properties. That includes:

- Late payments

- Collections

- Charge-offs

- Bankruptcies

- Foreclosures

- Judgments and liens

If two borrowers are on the loan, underwriters usually use the lower of the two middle scores to set the rate and LTV tier. So a co-borrower with a lower score can weaken the file instead of helping it.

Liquidity, Reserves, and Down Payment Requirements

Lenders want to see money left after closing. Why? Because rentals come with vacancies, repairs, and the occasional surprise that shows up at the worst time. Better credit and stronger property cash flow can sometimes reduce how much cash you need on hand at the start.

The down payment is just one part of the cash needed. Most DSCR and non-QM programs ask for 20% to 25% down. On top of that, closing costs often add $4,000 to $8,000, depending on loan size and state. Many lenders also want 3 to 6 months of PITIA in reserves after closing. For loans above $2.5 million, that can increase to 12 months.

Extra liquidity can help when a file is close to the line. In many cases, lenders will count funds from checking and savings accounts, money market accounts, stocks, bonds, and retirement accounts like 401(k)s or IRAs.

Income Documentation vs. Cash-Flow Qualification

This is where investment loans split into two main paths.

Conventional investment loans use full income documentation. That usually means W-2s, tax returns, pay stubs, and a debt-to-income ratio that often falls in the 43% to 50% range. If the borrower's personal income and current debts don't support the new payment, the deal can fall apart even when the rental income looks strong.

DSCR loans work differently. They qualify the property's cash flow, not the borrower's personal income.

That's a big deal for self-employed borrowers and 1099 earners. On paper, their tax returns can show lower income than what they actually bring in. In those cases, bank statement loans - a type of non-QM loan - can use 12 to 24 months of deposits to estimate qualifying income instead of relying on tax returns.

Here's how the two paths compare:

| Feature | Conventional Investment | DSCR / Non-QM |

|---|---|---|

| Income Verification | W-2s, tax returns, pay stubs | Property rental income; no personal income docs |

| DTI Limit | Typically 43%–50% | None |

| Min Credit Score | 680 | 640–660 |

| Down Payment | 15%–25% | 20%–25% (up to 35% for lower FICO) |

| Reserves | 2–6 months PITIA | 3–12 months PITIA |

Source ranges for the table: [4][6][7][5][8][9][10][11].

Next, lenders test the property's rent support, condition, and DSCR.

Property, Cash Flow, and Collateral: What Lenders Check Next

Next, the lender looks at the deal itself: the property's value, rental income, condition, and how you plan to get out of the loan. This review gets a lot tighter when the property needs work or when the rent barely covers the payment.

Appraisal, Rent Analysis, and Market Rent Support

With DSCR loans, the appraisal does more than set a market value. It also includes a rent schedule that lenders use to qualify the income. To estimate market rent, appraisers usually look at recent lease comps from nearby properties.

If the property already has a tenant, lenders usually use the lower of:

- the actual lease rent

- the appraiser's market rent estimate

That matters more than many investors think. If the current lease is below market, it can pull down the qualifying DSCR.

A low appraisal or soft rent estimate can reduce the loan amount, force you to bring more cash to closing, or knock the deal out on DSCR altogether. That's why it's smart to pull your own rent comps before you apply. It gives you a clear read on whether the deal works on paper before the lender does.

DSCR, Cash Flow, and Key Underwriting Ratios

DSCR stands for Debt Service Coverage Ratio. The formula is simple:

DSCR = Monthly Gross Rental Income ÷ Monthly PITIA

PITIA includes principal, interest, taxes, insurance, and HOA dues. A ratio of 1.00 means the rent covers the debt service exactly. A ratio of 1.25 means the income is 25% higher than the debt service.

Most lenders want at least 1.20 to 1.25 if you want standard pricing and the highest LTV. Ratios from 1.00 to 1.24 can still work, but they often come with a rate add-on of 0.50% to 0.75%.

| DSCR Ratio | Lender Interpretation | Typical Response |

|---|---|---|

| 1.25+ | Strong cash flow | Best rates; up to 80–85% LTV |

| 1.00–1.24 | Breakeven/standard | Standard terms; may require 25% down |

| 0.75–0.99 | Negative cash flow | Specialty programs only; higher rates and 30–35% down |

| Below 0.75 | High risk | Most lenders decline; requires 60–65% LTV |

Two costs get missed all the time: insurance and HOA fees. Both count in PITIA, and rising insurance premiums can push an otherwise workable deal below 1.00 late in the process. An early insurance binder can save you from getting blindsided right before closing.

If the property doesn't cash flow cleanly, lenders pay even more attention to condition and repair scope.

Property Condition, Repair Scope, and Exit Strategy

Long-term rental loans usually require a rent-ready property. If the property is distressed, you'll often need bridge or fix-and-flip financing first. "Rent-ready" generally means the major systems work, the property is safe, and there isn't major deferred maintenance. If the appraisal points to serious habitability issues, the lender may decline the DSCR loan outright.

Bridge and fix-and-flip loans work differently. Instead of leaning on current rental income, lenders focus on the After-Repair Value (ARV), or what the property should be worth after the renovation is done. They review the scope of work, the rehab budget, the timeline, and the borrower's exit plan.

And that's the key point: lenders underwrite the exit, not just the rehab. They want to know what happens next. Will you sell the property after the work is done? Or will you refinance into a long-term DSCR loan once the home is rented? For buy-rehab-rent-refinance deals, lenders usually want 3 to 6 months of seasoning before they use the new value instead of the original purchase price.

How hard they press on these points comes down to the loan program.

How Loan Requirements Differ by Loan Type

Investment Property Loan Types: Requirements at a Glance

Loan programs don't all look at the same thing first. Each one puts the spotlight somewhere else: income, rent coverage, or the risk tied to a rehab project.

Rental Property and DSCR Loans

DSCR loans care more about rent coverage than personal income. That changes the whole approval test. Instead of leaning on W-2s or DTI, the lender looks at whether the property's cash flow can carry the payment.

That doesn't mean the rest disappears. Lenders still check credit score, down payment, reserves, and property condition. But the main question becomes simple: what can the rent support? Better credit can help you get better pricing and more leverage. Lower credit usually cuts into both. DSCR loans can also be titled in an LLC, which makes them a good fit for investors who want entity ownership.

If the rent works but your tax returns don't, a bank statement loan may make more sense.

Non-QM Loans for Self-Employed and 1099 Borrowers

Bank statement loans use deposits instead of tax returns to qualify self-employed and 1099 borrowers. In plain English, the lender shifts from tax-doc income to deposit history.

There's a catch, though. Lenders still apply an expense factor to those deposits before they calculate qualifying income. For business accounts, that figure is often 50%. So if your actual expenses are higher than that, the income number the lender uses may come in lower than you'd expect. Credit, reserves, down payment, and property quality still play a part.

If the property needs major work too, the focus shifts again - from income review to rehab risk and exit risk.

Bridge and Fix-and-Flip Loans

These loans are underwritten around renovation risk, not stabilized cash flow. With bridge and fix-and-flip loans, the rehab plan can make or break the deal.

Common reasons for denial include:

- An inflated ARV

- A rehab budget that doesn't line up with the scope of work

- Reserves that are too thin for cost overruns

- No clear exit plan

First-time flippers also tend to face lower leverage caps - around 70% to 75% of total project cost - than investors with more experience.

How to Check Your Approval Odds Before You Apply

Use the borrower, property, and deal tests above as a last filter before you apply.

Before you send anything in, do a quick self-check. A lot of denials come from a small set of problems that can be fixed. Catching them early can save time, stress, and money.

A Borrower and Property Readiness Checklist

Run through these six variables before you apply. They line up with the three buckets lenders look at: borrower strength, property performance, and deal structure. If one bucket is weak, fix that part first instead of trying to squeeze the deal into the wrong loan program.

- Credit score: Are you at 660, 680, or 740+? If you're close to a pricing cutoff, it may make sense to wait and improve the file before applying.

- Down payment plus closing costs: Can you cover the down payment and closing costs? For most investment loans, that usually means 20% to 25% down, plus closing costs.

- Post-closing reserves: Will you still have 3 to 6 months of liquid personal reserves after closing?

- DSCR estimate: Aim for 1.25+ DSCR. Below 1.00 usually fails.

- Property condition: Will the property be rentable at closing? Standard DSCR and conventional rental loans usually require that.

- Income method: Are you qualifying with W-2s and tax returns, bank statements, or property cash flow alone? Match the file to the loan type that fits.

If reserves are tight, check whether the lender lets you use cash-out refinance proceeds to meet part of the reserve rule for 1- to 4-unit properties.

Loan Type Requirements and Denial-Risk Tables

Use this matrix to compare the loan type with the file you actually have.

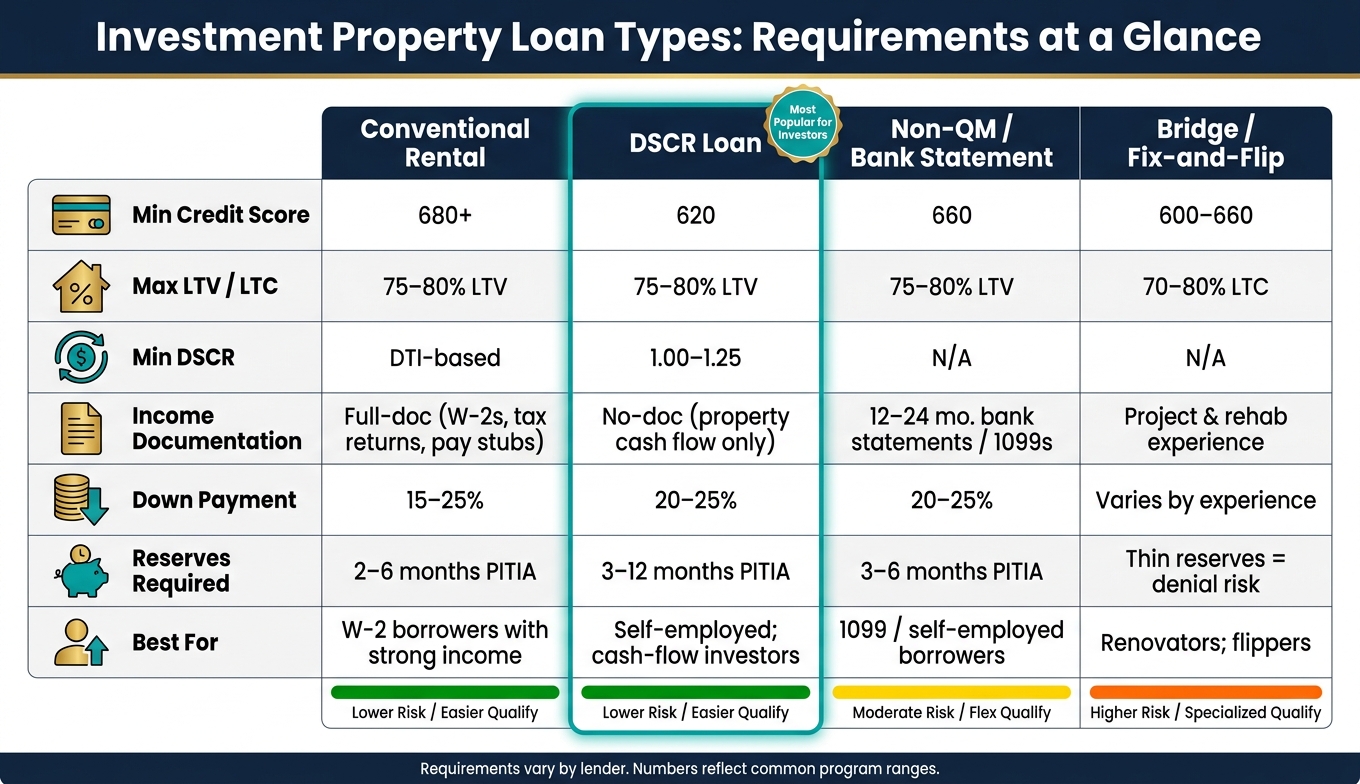

| Loan Type | Min FICO | Max LTV/LTC | Min DSCR | Income Doc |

|---|---|---|---|---|

| Conventional Rental | 680+ | 75%–80% LTV | DTI-based | Full-doc |

| DSCR Loan | 620 | 75%–80% LTV | 1.00–1.25 | No-doc (property cash flow) |

| Non-QM (Bank Statement) | 660 | 75%–80% LTV | N/A | 12–24 mo. bank statements / 1099s |

| Bridge / Fix-and-Flip | 600–660 | 70%–80% LTC for newer investors; higher leverage for experienced borrowers | N/A | Project / rehab experience |

Here’s where deals tend to break down most often, based on the bucket that fails:

| Bucket | Denial Trigger | Impact |

|---|---|---|

| Property | DSCR < 1.00 | Denial or 65% LTV cap |

| Property | Low appraisal or rent estimate | Requires more cash to close |

| Borrower | Insufficient reserves | Denial at final underwriting |

| Deal | Heavy rehab / no experience | Denial or lower leverage cap |

Conclusion: The Requirements That Matter Most

Match the property, income method, and reserve level to the loan type before you apply. Investors who avoid preventable denials are usually the ones who run the numbers first.

FAQs

Which loan type fits my situation best?

The right loan comes down to three things: your income paperwork, the kind of property you're buying, and what you're trying to do with the deal.

- Conventional loans work best for investors with strong W-2 income and solid credit who want the lowest rates. The tradeoff? You’ll need full income verification, you’ll face strict debt-to-income limits, and financing is capped at 10 properties.

- DSCR loans are a good fit for self-employed investors or buyers with multiple properties. That’s because approval is based on the property’s cash flow, not your personal income.

- Portfolio loans give lenders more room to work with, which can help if you’re buying an unusual property or your finances are a bit more complex.

- Hard money loans are built for short-term fix-and-flip deals where speed matters most.

Can I qualify if the property needs repairs?

It depends on the loan program.

Standard DSCR loans usually require the property to be in acceptable condition. In many cases, they also don’t allow fix-and-flip properties.

Lenders will also check your liquid reserves. They want to see that you have cash on hand to cover things like surprise repairs or a stretch of vacancy.

If the property is in rough shape, a standard long-term DSCR rental loan may not fit. In that case, you may need bridge financing or fix-and-flip financing instead.

What can I do before applying to improve approval odds?

Before you apply, get the basics in order.

Start with your credit profile. Keep revolving balances below 30%, fix any reporting errors, and avoid new credit applications for 60 to 90 days. Small moves here can make a big difference.

Next, build liquidity. In most cases, you’ll want 20% to 25% down, plus 3 to 6 months of PITIA reserves. That means cash set aside for principal, interest, taxes, insurance, and association dues if they apply. Lenders like to see that you can handle the property even if things don’t go perfectly right away.

Then check the deal itself. Confirm the rents, look closely at the property’s condition, and if you’re using a DSCR loan, aim for about 1.20 to 1.25. Put simply, the numbers need to work on paper before they work in real life.