Non-QM Loans Explained: The Investor's Complete Guide

If your tax returns make you look weaker than you are, a Non-QM loan may keep your next deal alive.

I’d sum it up like this: Non-QM loans give investors other ways to qualify when W-2 income, tax returns, or the 10-financed-property cap shut the door. They still require full underwriting and Ability-to-Repay review, but lenders may use bank statements, 1099s, rental income, or assets instead.

Here’s the short version:

- DSCR loans fit rental properties that can cover their own payment

- Bank statement loans fit self-employed borrowers with strong deposits but low taxable income

- Asset depletion loans fit borrowers with large liquid assets and limited monthly income

- Credit-event programs fit borrowers who are past a bankruptcy, foreclosure, or short sale and have rebuilt

A few numbers matter right away:

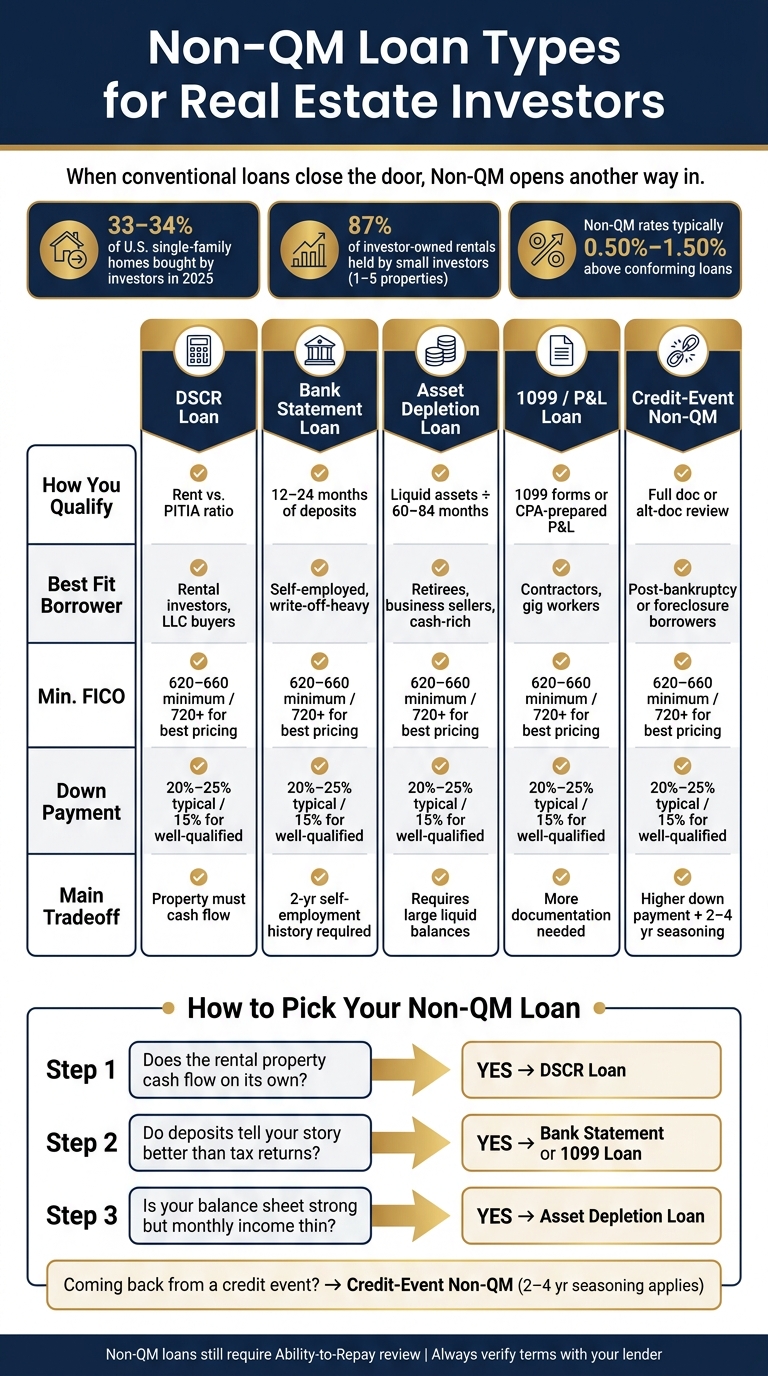

- Investors bought 33% to 34% of U.S. single-family homes in 2025

- 87% of investor-owned single-family rentals are held by small investors with 1 to 5 properties

- Many Non-QM programs look for 620 to 660+ FICO

- Investment property down payments often start around 20% to 25%

- Non-QM rates are often about 0.50% to 1.50% above comparable conforming loans

- DSCR pricing often gets better at 1.25+ DSCR, while some lenders may go down to 0.75

Non-QM Loan Types for Real Estate Investors: Side-by-Side Comparison

🏡💰 Understanding Non-QM Loans | DSCR Loans Explained

sbb-itb-e7c549b

Quick Comparison

| Loan type | How I qualify | Best fit | Main catch |

|---|---|---|---|

| Conforming | W-2s, tax returns, DTI | Simple income, smaller portfolio | Tight rules, 10-property limit |

| DSCR | Property rent vs. PITIA | Rental investors, LLC buyers | Higher rate, property must cash flow |

| Bank statement | 12–24 months of deposits | Self-employed, write-off heavy borrowers | More expensive than conforming |

| Asset depletion | Assets turned into income | Retirees, business sellers, cash-heavy borrowers | Need large liquid balances |

| Credit-event Non-QM | Alt-doc or full-doc review | Borrowers after a setback | More cash down, more reserves |

My takeaway is simple: pick the loan based on what is strongest in your file. If the property cash flows, DSCR may be enough. If your deposits tell the story better than your tax returns, bank statement or 1099 may fit. If your balance sheet is strong, asset depletion may work.

That’s the lens I’d use before comparing rates, reserves, prepay penalties, and loan terms.

What Non-QM loans are and who they are built for

Non-QM loans use a different underwriting approach for borrowers who don't fit the usual income rules. Unlike standard QM loans, they don't rely on W-2s or tax returns to prove repayment ability. For many investors, the main problem isn't getting credit at all. It's showing income in a way that fits the lender's checklist.

Non-QM loans still require an Ability-to-Repay review. The difference is how that review happens. Lenders may verify income with bank statements, rental cash flow, asset balances, or P&L statements.

Borrowers who commonly use Non-QM financing

Non-QM financing works for borrowers whose income is there, but doesn't show up cleanly under conventional underwriting. The investor profiles you see most often include:

- Self-employed borrowers with heavy write-offs

- 1099 contractors and freelancers with steady cash flow but no W-2

- LLC owners buying through an LLC for liability protection

- Portfolio investors who have hit the conventional 10-financed-property limit

- Borrowers with strong assets but uneven monthly income

- Borrowers with recent credit events who have recovered financially but are still inside conventional waiting periods

That list gets to the heart of why Non-QM exists. It's built for people with workable finances that don't fit neat boxes. The next piece is seeing how it differs from conventional loans and DSCR loans.

Why investors choose Non-QM over conventional loans

A lot of investors move to Non-QM because tax write-offs can make their reported income look weaker than it is. Depreciation and business deductions may push taxable income down even when the property or business is doing fine.

"QM loans were designed for households, not portfolios. They break the moment you start stacking properties." - Todd Orlando, CEO, Defy Mortgage

There's also the property-count problem. Conventional loans often cap investors at 10 financed properties. Non-QM programs, especially DSCR-based options, can get around that by qualifying the loan based on property-level cash flow instead of personal DTI.

Speed is another big reason. Non-QM can move faster than conventional underwriting, which can make a difference when you're trying to win a purchase in a tight market. That gap becomes clearer when you compare full-documentation loans, DSCR loans, and other Non-QM options.

How Non-QM differs from conventional and DSCR financing

Conventional loans are the most rigid. DSCR is one Non-QM path built around rental cash flow. Broader Non-QM programs look at income in other ways. For investors, the big issue is simple: should the lender qualify you, the property, or both?

Documentation, qualification, and use-case differences

The main split comes down to what the lender reviews to approve the loan.

Conventional loans lean on personal income history. That usually means W-2s, tax returns, and pay stubs. They also tend to cap debt-to-income ratios at 43%. And Fannie Mae limits investors to 10 financed properties, which can become a serious bottleneck as a portfolio gets larger.

DSCR loans take a different route. They do not use personal income or personal DTI. Instead, the lender looks at whether the property's rental income can cover the mortgage payment, including principal, interest, taxes, insurance, and HOA fees.

Broader Non-QM programs sit in the middle. Loans like bank statement and asset-based programs still underwrite the borrower, but they use alternate income proof instead of W-2s. So if your tax returns don't tell the whole story, these programs may give the lender a better view of your finances.

| Feature | Conventional (QM) | DSCR (Non-QM) | Broader Non-QM |

|---|---|---|---|

| Income Documentation | W-2s, tax returns, pay stubs | Leased rent or market rent estimate | Bank statements, 1099s, P&L, asset statements |

| Qualifying Method | Personal DTI | DSCR ratio (Rent ÷ principal, interest, taxes, insurance, and HOA) | Alternative income calculation |

| Property Types | Primary, second home, limited investment | Investment properties only | Primary, second home, investment |

| Property Count Limit | Max 10 financed properties | No limit | Varies by lender |

| Underwriting Flexibility | Low - rigid agency guidelines | High - property performance focused | High - flexible underwriting |

| Best-Fit Borrower | W-2 employees with simple portfolios | Scaling rental investors, LLC borrowers | Self-employed investors, 1099 earners, asset-rich retirees |

When DSCR is enough and when a broader Non-QM option fits better

DSCR works when the property can carry the deal on its own. If the rental brings in enough income to cover the mortgage payment - ideally with a DSCR ratio of 1.0 or higher - you may not need to rely on your personal financials at all. That's why it fits rentals that can qualify on cash flow alone.

Broader Non-QM programs make more sense when cash flow is tight or when the property is not an investment property. A self-employed borrower buying a primary residence or vacation home will often look at bank statement or 1099 programs, because DSCR does not apply to owner-occupied properties.

Asset depletion can also help borrowers with a lot of liquid assets but uneven monthly income. In that setup, the lender converts those assets into qualifying income by dividing the total balance over 60 to 84 months.

Next, compare the main Non-QM programs investors use: bank statement, DSCR, asset-based, and credit-event options.

Main Non-QM loan types investors use

Each program solves a different problem. Some help you show income in a way that matches how you actually earn. Others lean on property cash flow. And some are built for borrowers working their way back after a credit hit.

Bank statement loans and asset-based qualification

Bank statement loans are made for investors whose tax returns don't tell the whole story. Instead of relying on reported income, lenders review 12 or 24 months of bank deposits to estimate what you earn. In many cases, they apply a 50% expense factor to those deposits. If your business runs lean, a CPA letter may support a lower expense factor, which can increase the income used to qualify you.

Asset-based qualification takes a different route. The lender focuses on liquid assets like brokerage accounts, savings, and retirement funds. Those assets are then converted into qualifying income.

This can work well for borrowers who have money on the balance sheet but not much monthly income on paper, such as:

- Retirees

- Business sellers

- High-net-worth investors

That setup can be a strong fit when cash reserves are solid but standard income docs are thin.

If the rental can stand on its own, move to DSCR.

DSCR loans and interest-only options for rental property cash flow

DSCR loans qualify the property based on rental cash flow, not your personal income. Most programs look for a DSCR of 1.0 or higher, though some will go down to 0.75.

For investors right on the line, interest-only can help. Moving from a fully amortizing payment to an interest-only setup for the first 5 to 10 years can cut the monthly payment by about 8% to 10%. That drop may be enough to push a borderline deal into qualifying range.

Short-term rentals can work under some DSCR programs, but it depends on the exact property address and local permitting rules. That's the part you don't want to gloss over. Confirm that the property is allowed to operate as an STR before you go under contract.

Programs for borrowers with recent credit events

Some Non-QM programs are built for investors coming back after a rough patch. They can fit borrowers recovering from bankruptcy, foreclosure, or a short sale.

The tradeoff is pretty direct. You should expect:

- A higher down payment

- Larger reserve requirements

- A rate premium compared with borrowers who have clean credit

Most Non-QM programs in 2026 call for a seasoning period of 2 to 4 years after the credit event. Some lenders may look at a borrower once they hit 24 months, case by case, but 36 months is still a common approval point.

The table below puts the main Non-QM program types next to each other:

| Program Type | Documentation Method | Best Use Case | Typical Borrower | Main Tradeoff |

|---|---|---|---|---|

| DSCR | Lease or market rent vs. PITIA | Scaling rental portfolios | Real estate investors | Higher rates |

| Bank Statement | 12–24 months of deposits | Primary or investment purchase | Self-employed/freelancers | 2-year self-employment history |

| Asset Depletion | Liquid asset statements | High-net-worth / retirement | Retirees, business sellers | Requires strong liquidity |

| 1099 / P&L | 1099-NEC forms or CPA-prepared P&L | Complex business structures | Independent contractors, gig workers | More documentation |

| Credit Event | Full doc or alternative doc | Recovery after a financial disruption | Post-bankruptcy or foreclosure borrowers | Higher down payment |

Qualification standards, costs, and how to decide

Once you know which Non-QM program fits, the next step is simple: can you meet the lender's credit, cash, and reserve rules?

What lenders look at: credit, down payment, reserves, and rent coverage

Non-QM underwriting is still strict. Lenders still look hard at your credit, equity, and liquidity. The difference is in how they weigh those pieces compared with conventional programs.

Credit score sets the baseline. Most programs start with a 620–660 minimum FICO, but a 720+ score is often where better rates and higher loan-to-value options start to open up.

Down payment on investment properties usually lands in the 20% to 25% range. Some programs may allow 15% down for well-qualified borrowers, but that's more of an outlier than the norm.

Reserves after closing are another big checkpoint, and this is where many investors get surprised. It's common to need 3 to 12 months of PITIA reserves, with higher leverage and larger loan amounts often leading to tougher reserve demands.

With DSCR loans, lenders use the appraisal rent schedule to see whether the property can cover its debt. A DSCR of 1.25 or above usually gets the best pricing tiers. Ratios below 1.0 point to negative cash flow, which tends to bring tighter underwriting.

For bank statement and 1099 programs, lenders may still check personal DTI, often with a cap near 50%. DSCR loans, by contrast, focus mostly on the property's cash flow.

Pricing tradeoffs: what you pay for flexible qualification

Non-QM rates are higher than conventional loans. That's the plain tradeoff. In most cases, the premium falls between 0.50% and 1.50% above similar conventional rates.

The exact bump depends on the program. DSCR and asset depletion loans are often at the lower end, around +0.50% to 1.00%. Bank statement and 1099 loans usually come in a bit higher, around +0.75% to 1.25%.

Prepayment penalties also show up often on investor-focused Non-QM loans. These usually cover a 1–3 year period, so it's smart to check that part of the note before you sign.

You're paying more, yes. But in return, you may get looser income documentation, room for larger reserves, and a path to grow a rental portfolio when conventional rules start boxing you in.

How to choose the right Non-QM loan for your investment strategy

The best fit usually comes down to three things: where your income comes from, how the property performs, and how much cash you can keep on hand after closing.

DSCR works well for rentals with enough rent to support the debt. It's often a strong match if you're close to the conventional 10-property limit or if you'd rather leave personal income out of the approval process.

Bank statement and 1099 programs fit borrowers whose income is there, but doesn't show up well on tax returns. In that case, deposits or gross earnings do the heavy lifting instead.

Asset depletion can work for borrowers with strong liquidity and a solid balance sheet, but not much monthly income on paper. It turns those assets into qualifying income.

If you're coming back from a recent credit event, expanded-credit programs may also be on the table, though seasoning rules still apply.

FAQs

Is a Non-QM loan harder to get than a conventional loan?

It comes down to your financial profile.

If you earn standard W-2 income and your tax returns are clean, a conventional loan is often the easier and lower-cost option. Why? It fits the usual agency guidelines, so the approval path tends to be more straightforward.

If your income doesn’t look as neat on paper, things can get trickier. Self-employed income, uneven monthly deposits, large write-offs, or income from other sources can make a conventional loan harder to qualify for.

That’s where a Non-QM loan can help. It can be easier to get because the underwriting is more flexible and may look at:

- Bank statements

- Assets

- Property performance

So, if your finances fit the standard mold, conventional is often the simpler route. If they don’t, Non-QM may give you more room to work with.

Can I use a Non-QM loan to buy through an LLC?

Yes. You can use a Non-QM loan to buy an investment property through an LLC.

This setup often works well for investors who use LLCs for asset protection or business reasons. In many cases, DSCR loans are a common fit because they look at the property's rental income instead of the usual personal income paperwork.

During underwriting, expect to provide your entity documents.

When does a bank statement loan make more sense than a DSCR loan?

A bank statement loan is often a better fit for a self-employed borrower with strong business cash flow when their tax returns don't show what they actually earn because write-offs lower their reported income.

A DSCR loan leans on the property's rental income. A bank statement loan looks at 12 to 24 months of personal or business bank deposits to verify income. Go with a bank statement loan when you need to qualify based on deposits, not on how the rental property performs.