How to Refinance a Rental Property with a DSCR Loan

If your rental income can cover the new mortgage payment, you may be able to refinance without using your personal income. That’s the core idea behind a DSCR loan.

If I were sizing up this option, I’d focus on five things first:

- DSCR math: monthly rent ÷ monthly PITIA

- Property type: investment property only, not a primary home

- Credit score: many lenders look for 620–680+

- Equity: often up to 75%–80% LTV for rate-and-term, 70%–75% for cash-out

- Reserves: often 2–6 months of PITIA

In plain terms, this refinance works best when the property’s cash flow is strong, the value is there, and I want to avoid full personal-income review. It can also help if I’m leaving short-term debt, pulling cash from equity, or my tax returns don’t show much income after write-offs.

Here’s the short version of what matters most:

- A 1.25 DSCR or higher often gets the best pricing

- A DSCR near 1.00 may still work, but terms can get tighter

- Closing costs often run about 2% to 4% of the loan amount

- Many DSCR refinances close in about 21 to 28 days

- Cash-out deals often have lower LTV limits and more seasoning rules

A quick example: if rent is $2,400 and the new PITIA is $2,000, the DSCR is 1.20. If rent is $2,000 and PITIA is $1,950, the DSCR is 1.03. That small gap can change pricing, leverage, and approval odds.

| Loan type | Common LTV | Common DSCR target | Main goal |

|---|---|---|---|

| Rate-and-term | Up to 80% | Around 1.00–1.15 | Lower rate or change term |

| Cash-out | Up to 70%–75% | Around 1.10–1.25 | Pull equity from the property |

The bottom line: if I’m refinancing a rental property with a DSCR loan, I’d check rent, PITIA, credit, reserves, and prepayment penalties before I apply. That gives me a fast read on whether the deal is likely to work.

DSCR Loan Refinancing | Lower your rate or cash out with DSCR

sbb-itb-e7c549b

How a DSCR Refinance Works

A DSCR refinance swaps your current mortgage on a rental property for a new investment-property loan. At its core, the lender is looking at one thing: does the property's rent cover the new monthly payment? Instead of leaning on your W-2s or tax returns, the lender looks mostly at the property's cash flow.

What DSCR Means and How It Is Calculated

DSCR stands for Debt Service Coverage Ratio. The standard formula is:

DSCR = Monthly Gross Rent ÷ Monthly PITIA

PITIA includes principal, interest, taxes, insurance, and any HOA dues. This ratio matters because it affects both approval and loan terms. In plain English, a higher DSCR usually puts you in a better spot for pricing and leverage.

| DSCR Ratio | Approval Range | Typical Terms |

|---|---|---|

| 1.25 or higher | Strong | Best pricing, up to 80% LTV for rate-and-term |

| 1.00 – 1.24 | Standard | Most common range; standard pricing |

| 0.75 – 0.99 | Marginal | Requires 700+ credit or lower LTV (65%–70%) |

| Below 0.75 | Weak | Limited no-ratio options; significant equity required |

A common mistake? People ballpark PITIA and end up with a ratio that looks better than it should. If property taxes or insurance get left out, the deal may seem fine at first glance but fall apart once underwriting checks the numbers.

How Lenders Use Rental Income to Qualify the Loan

For occupied properties, lenders usually use the lower of the current lease amount or the appraiser's market rent estimate. That estimate often comes from a rent schedule, usually Form 1007 for single-family homes. So even if your tenant is paying above-market rent, the lender may still base the file on the lower market-rent number.

If the property is vacant when you refinance, some lenders use 90% of the appraiser's market rent estimate to account for vacancy, while others use 100% of projected market rent. Some also make a vacancy or income adjustment before they calculate DSCR. Either way, that rent figure drives underwriting, not the borrower's personal income.

When a DSCR Refinance Is the Right Fit

This setup can make a lot of sense for investors whose tax returns show losses due to depreciation, even when the property is bringing in rent. It's also a solid option for borrowers who want cash-out without going through personal-income underwriting.

It can also help investors move out of short-term bridge or hard money debt and into a lower-rate, long-term loan.

If the math checks out, the next step is to look at the property, credit, equity, and reserve rules that shape approval.

Check Your Eligibility Before You Apply

Before you apply, look at three basics: property type, credit score, and equity.

Property, Credit, and Equity Requirements

DSCR loans are built for non-owner-occupied rental properties. That means the property needs to be an investment property, not your primary home.

Eligible property types include:

- Single-family homes

- 2–4 unit properties

- Condos

- Townhomes

- PUDs

Primary residences do not qualify.

Credit score matters too. Most lenders want a minimum FICO score between 620 and 680. If your score is 720 or higher, you can often get better pricing and a higher LTV. A lower score doesn't always knock you out, but it can lead to tighter loan terms.

Equity is a big piece of the puzzle. For a rate-and-term DSCR refinance, many lenders allow up to 75%–80% LTV. For a cash-out refinance, the cap is often lower, usually 70%–75% LTV.

Lenders also want to see cash reserves. In most cases, that means 2 to 6 months of PITIA in liquid reserves. For larger loans over $1.5 million, the reserve requirement may jump to 6–12 months. And timing matters: if you try to do cash-out too soon, the lender may limit the loan amount to the purchase price plus documented rehab costs.

If your property and borrower profile line up with those basics, the next move is to check your DSCR and pull together your documents.

DSCR Benchmarks with Simple Examples

The math is pretty simple: monthly gross rent ÷ monthly PITIA.

Here are two quick examples:

Example A - Solid file: Monthly rent is $2,400. New PITIA is $2,000. DSCR = $2,400 ÷ $2,000 = 1.20.

Example B - Tight file: Monthly rent is $2,000. New PITIA is $1,950. DSCR = $2,000 ÷ $1,950 = 1.03.

In plain English, a higher ratio gives the lender more breathing room. A DSCR of 1.25 or higher is often the range where lenders offer their best pricing and more room on terms. If the ratio drops below 1.00, some lenders may still look at specialty low-ratio programs, but those deals usually come with lower LTV caps and stricter credit standards.

Documents to Gather Before Applying

Getting your paperwork ready up front can save time later. Most lenders will ask for:

- Current mortgage statement and written payoff letter - the payoff letter helps confirm any prepayment penalty on your existing loan

- Lease agreements and rent roll

- Recent property tax bill and insurance declarations page - both are used to calculate PITIA

- 2–6 months of bank statements - to verify liquid reserves

- Government-issued photo ID and signed credit authorization

- Entity documents if the property is held in an LLC: Articles of Organization, Operating Agreement, EIN documentation, and a Certificate of Good Standing

If the property is vacant, lenders usually use Form 1007 market rent instead of a lease.

With your numbers checked and your documents in hand, the refinance process usually moves faster. After that, you can look at whether a rate-and-term or cash-out setup makes more sense.

The DSCR Refinance Process, Step by Step

Once your file is ready, the refinance moves through a pretty standard path: application, appraisal, underwriting, and closing. In short, the lender looks at the loan setup, checks the property's value and income, reviews the file, and then moves it to funding.

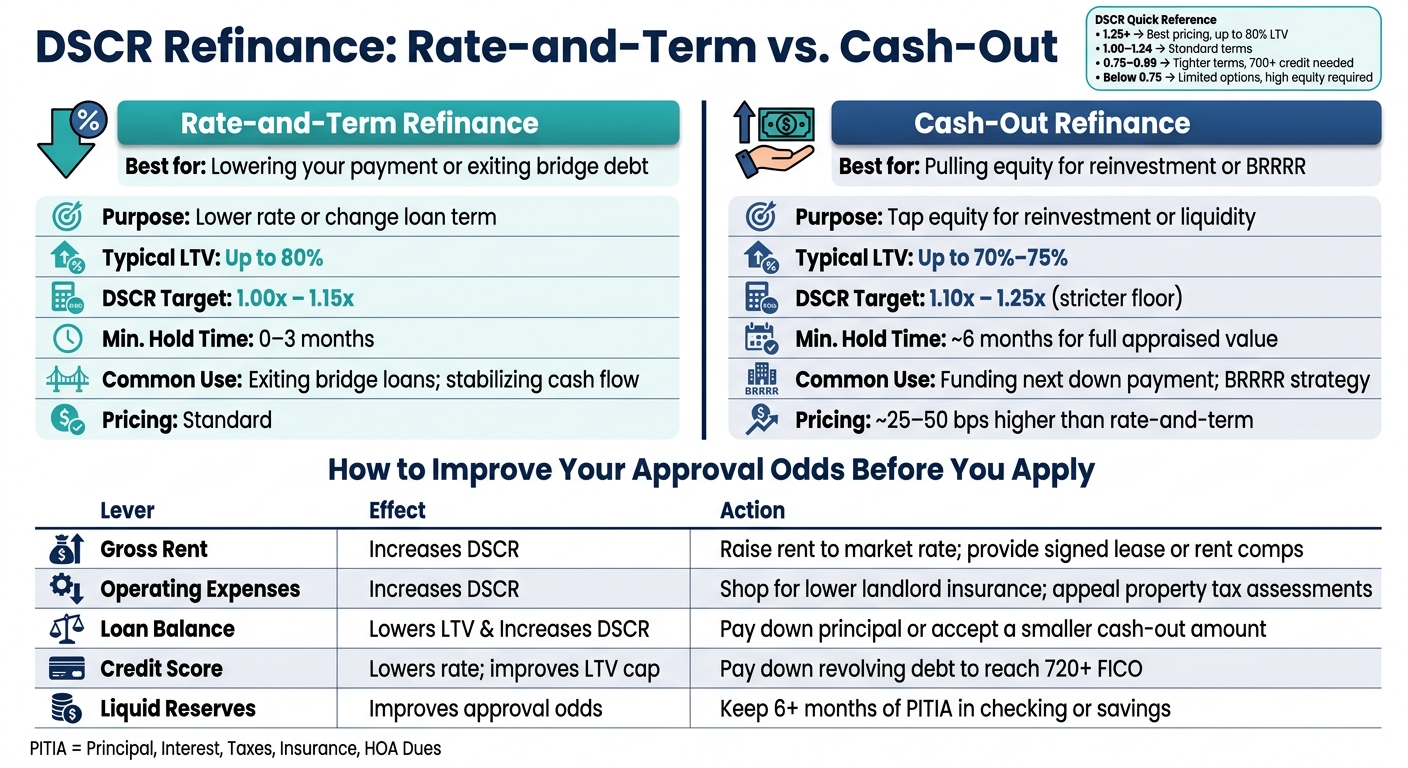

Rate-and-Term or Cash-Out: Choosing the Right Structure

Start by picking the structure that fits your goal. If you want a lower or steadier payment, a rate-and-term refinance is usually the right move. If you want to tap equity, a cash-out refinance lets you pull money from the property, with the difference paid to you in cash.

Cash-out loans tend to come with lower leverage limits, higher pricing, and longer seasoning rules than rate-and-term deals.

After that choice is locked in, the lender checks the property's income and value.

Application, Appraisal, and Underwriting

This is where the lender digs into the file and the property details. After you apply, the lender reviews the file, orders the appraisal, and checks the numbers. Initial screening usually takes three days.

The appraisal does more than set value. It also sets market rent, using Form 1007 for single-family properties or Form 1025 for 2–4 unit properties.

Underwriting centers on DSCR, LTV, credit score, and liquid reserves. The underwriter also checks title for existing liens or other issues that could slow things down. This phase usually runs from days 7 through 14. Common delays come from appraisal problems, title issues, or LLC paperwork that wasn't ready when the application was submitted. Those delays can add 7 to 14 days.

Approval, Closing Costs, and Funding Timeline

Once underwriting is done, the loan moves to closing. You'll usually get a conditional approval first, along with any last items the lender needs, such as an updated bank statement, insurance binder, or LLC Certificate of Good Standing. When those conditions are cleared, the lender issues a clear-to-close.

Closing costs on a DSCR refinance usually land around 2% to 4% of the loan amount. That often includes the appraisal, title, escrow, recording, origination, prepaids, and any discount points.

A few last details matter here:

- If the property is held in an LLC, you'll sign in the name of that entity.

- Funds are usually wired shortly after closing.

- The full process often wraps up within 21 to 28 days from application.

Before signing, check the prepayment penalty. Most DSCR loans use a step-down setup, such as 5-4-3-2-1, so it's smart to weigh the rate savings against the cost of getting out early.

Compare Your Options and Improve Your Approval Odds

DSCR Loan Refinance: Rate-and-Term vs. Cash-Out at a Glance

Once you understand how the refinance works, the next step is simple: compare the setup and tighten your numbers before you apply.

Rate-and-Term vs. Cash-Out: A Side-by-Side Look

Choose a rate-and-term refinance if your goal is a lower payment. Choose cash-out if you want to pull equity, though pricing is often 25 to 50 bps higher.

| Feature | Rate-and-Term Refinance | Cash-Out Refinance |

|---|---|---|

| Purpose | Lower rate or change loan term | Tap equity for reinvestment or liquidity |

| Typical LTV Range | Up to 80% | Up to 70%–75% |

| Typical DSCR Target | 1.00x–1.15x | 1.10x–1.25x (stricter floor) |

| Typical minimum hold time | 0–3 months | About 6 months for full appraised value |

| Common Use Cases | Exiting bridge loans; stabilizing cash flow | Funding next down payment; BRRRR strategy |

The best choice is usually the one that leaves the property with the strongest post-closing DSCR. Cash-out funds from a DSCR refinance can often be used for a new down payment, rehab, or other investment needs.

Once you pick the structure, focus on the three levers that tend to shape approval most: rent, leverage, and reserves.

How to Improve Your DSCR, LTV, and Reserves Before Applying

DSCR, LTV, and reserves have a big impact on approval and pricing. If you can improve even one before you apply, that can help.

| Lever | Effect | Action to Take |

|---|---|---|

| Gross Rent | Increases DSCR | Raise rent to market rate; provide a signed lease or rent comps |

| Operating Expenses | Increases DSCR | Shop for lower landlord insurance; appeal property tax assessments |

| Loan Balance | Lowers LTV; Increases DSCR | Pay down principal or accept a slightly smaller cash-out amount |

| Credit Score | Lowers rate; improves LTV cap | Pay down revolving debt to reach 720+ FICO |

| Liquid Reserves | Improves approval odds | Keep 6+ months of PITIA in a checking or savings account |

Not all assets are treated the same. Lenders usually do not count every asset at full value, so the type of reserve matters. Brokerage and retirement accounts are often discounted when counted as reserves, while cash in checking or savings tends to count more directly.

Lowering the loan amount is another useful move. Taking a slightly smaller loan - say, 70% LTV instead of 75% - can improve your DSCR enough to help you qualify for a better interest rate tier, which may improve net cash flow after closing.

Conclusion: Is a DSCR Refinance Right for You

If the numbers work, the refinance should support your next move without putting too much pressure on cash flow. A DSCR refinance works best as one piece of a broader portfolio plan. If the rent covers the payment and the equity is there, a DSCR refinance can replace higher-cost debt with a longer-term loan.

FAQs

Can I refinance with a DSCR loan if the property is vacant?

Yes. You can refinance a vacant rental property with a DSCR loan.

Instead of relying on a current lease, lenders look at the property’s income potential. In most cases, the appraiser provides a market rent survey - often on Fannie Mae Form 1007 - to estimate monthly rental income. That estimate is then used to calculate your DSCR and decide eligibility and loan terms.

Will a low DSCR automatically disqualify me?

No. A low DSCR can narrow your options, but it doesn’t automatically rule you out.

Many lenders look for 1.0+, but some programs go as low as 0.75. If your ratio falls below the usual cutoff, you may still qualify with a lower LTV, stronger credit, or a specialty no-ratio program.

How do prepayment penalties affect refinancing?

Prepayment penalties can have a big impact on refinancing because they add an upfront cost you need to compare against the upside of the new loan. A lot of DSCR loans use declining penalty structures like 5-4-3-2-1, while others charge a fixed percentage if you pay off the loan early.

Before you refinance, run the numbers and find your break-even point. The goal is simple: make sure your interest savings or cash-out proceeds are greater than the penalty.

Some borrowers go with a shorter penalty schedule or a buyout option to get more room to move. That extra flexibility often comes with a higher note rate.