Rental Property Loans: Which Financing Option Is Best for Your Strategy?

The best rental loan depends on what you’re trying to do. If you want the lowest cost, I’d look at conventional loans. If I want to qualify based on rent instead of my tax returns, DSCR loans often fit better. If I’m buying a fixer-upper and need to close in 5 to 21 days, I’d look at a bridge loan.

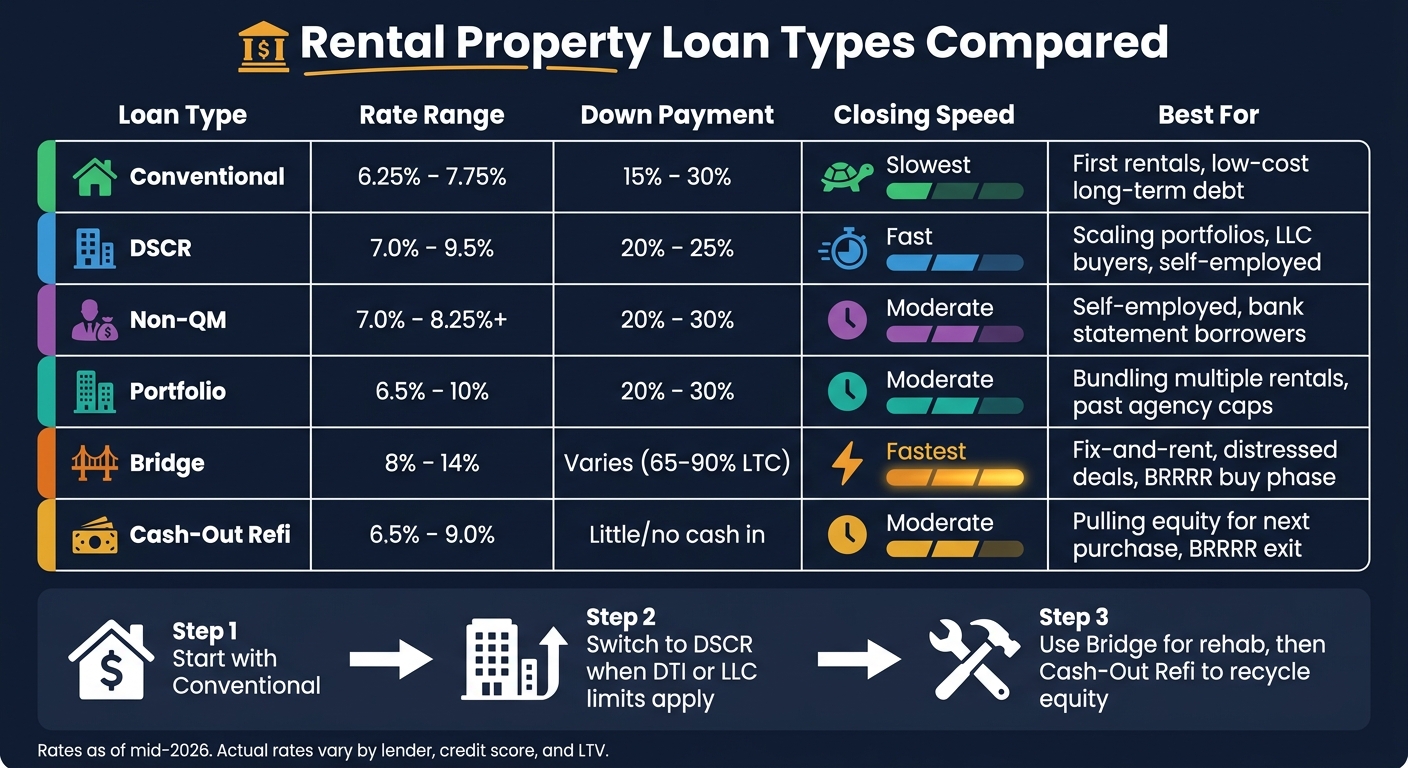

Here’s the short version:

- Conventional: lower rates, but tighter income rules and property-count limits

- DSCR: based on rental income, often 20% to 25% down, but rates are higher

- Non-QM: for self-employed borrowers using bank statements or assets

- Portfolio: for bundling multiple rentals under one loan

- Bridge: short-term money for purchase, rehab, or lease-up

- Cash-out refinance: pulls equity from a stabilized rental to fund the next deal

In most cases, I’d use this simple rule:

- Start with conventional if I can qualify and still have room to buy more

- Move to DSCR when DTI, write-offs, or LLC ownership make agency lending harder

- Use bridge for the buy-and-rehab phase

- Use cash-out refinance after the property is fixed, rented, and stable

A few numbers stand out:

- DSCR rates: about 7.0% to 9.5%

- Conventional rates: about 6.25% to 7.75%

- Bridge rates: about 8% to 14%

- DSCR and Non-QM down payments: often 20% to 30%

- Conventional financed-property cap: up to 10 properties

Rental Property Loan Types Compared: Rates, Down Payments & Best Use Cases

Best Loan Options for Investment Properties – Insider Tips for Smart Investors

sbb-itb-e7c549b

Quick Comparison

| Loan type | How I qualify | Typical cash needed | Rate range | Best use |

|---|---|---|---|---|

| Conventional | Personal income and DTI | 15% to 30% down | 6.25% to 7.75% | First rentals, lower-cost long-term debt |

| DSCR | Property rent vs. PITIA | 20% to 25% down | 7.0% to 9.5% | Scaling, LLC buying, self-employed borrowers |

| Non-QM | Bank statements, P&L, or assets | 20% to 30% down | 7.0% to 8.25%+ | Borrowers with tax-return issues |

| Portfolio | Lender looks at the group of properties | 20% to 30% down | 6.5% to 10% | Bundling loans, growing past agency caps |

| Bridge | Asset value, rehab plan, exit plan | Varies; often points plus reserves | 8% to 14% | Fix-and-rent, distressed deals, BRRRR buy phase |

| Cash-out refi | Equity, appraisal, and either DSCR or income | Usually little cash in | 6.5% to 9.0% | Pulling equity for the next purchase |

My take: the tradeoff is simple: easier approval usually means a higher rate. So before I pick a loan, I’d match it to my hold time, cash on hand, and exit plan.

That’s the lens I’d use for the rest of this article.

1. DSCR Loans

A Debt Service Coverage Ratio (DSCR) loan qualifies you based on the property’s income, not your personal income. In plain English: the lender looks at whether the rent can carry the payment.

Here’s the basic math. The lender divides gross monthly rent by PITIA, which stands for principal, interest, taxes, insurance, and association dues. If the result is 1.0x or higher, the property is covering its own debt. That’s why DSCR loans usually don’t require W-2s, tax returns, or employment verification.

For investors with heavy write-offs, that can be a big deal. A borrower may look weak on paper with a standard loan, even when the property itself cash flows just fine.

Qualification Standards

Many lenders will accept a 1.0x DSCR, but 1.20x to 1.25x usually gets you better pricing. So yes, you may qualify at the lower end, but the terms often look better when the property has more breathing room.

Credit score minimums often start around 640 to 660. If your score is 720 or higher, you’ll usually have a better shot at the best rates and higher LTV limits.

Short-term rental investors get a bit more flexibility too. Some lenders will use AirDNA projections, host statements, or a 12-month booking history to size income. That said, you need to check one detail before you get too far: whether the lender uses gross DSCR or net DSCR. Net DSCR is tougher because it also factors in operating costs.

Cash Needed Upfront

Most borrowers should expect a down payment of 20% to 25% for 1 to 4 unit properties. For 5+ unit or commercial deals, 25% to 30% is more common.

Maximum LTV usually lands at:

- 75% to 80% for purchases

- 70% to 75% for cash-out refinances

Lenders also tend to want reserves. In most cases, that means 6 to 12 months of PITIA, depending on the loan size and the number of properties you already own.

A larger down payment can help in two ways at once: it improves the DSCR and may push the loan into a better pricing tier.

Rates and Terms

DSCR loan rates usually fall in the 7.0% to 9.5% range. That’s about 50 to 200 basis points above conventional investment property rates.

Common loan structures include:

- 30-year fixed

- 40-year fixed

- 5/1 or 7/1 ARMs

Many programs also offer 10-year interest-only periods. That can improve monthly cash flow in the first years of a hold, which matters if you’re trying to keep payments lighter early on.

One thing to watch closely: prepayment penalties. They’re common on DSCR loans and usually come as a 3- to 5-year step-down. If you think you might refinance or sell within three years, it’s smart to push for a shorter penalty window at the start, even if that means taking a slightly higher rate. Origination fees usually run 1% to 2%.

Best-Fit Strategy

DSCR loans work best for investors who need the deal to stand on its own. They’re often a strong fit for self-employed borrowers, investors with heavy tax write-offs, and buyers who want to close in an LLC.

They also make sense for STR investors who want to qualify using projected rental income instead of a standard long-term lease. And they’re a common move for BRRRR investors who use a bridge loan for the rehab, then refinance into a 30-year fixed DSCR loan once the property is stabilized and rented.

That same setup is why DSCR is often used as the exit loan after a bridge rehab or short-term rental stabilization.

2. Conventional Investment Property Mortgages

If you can qualify based on your personal income, conventional loans are usually the cheapest way to finance an investment property. The upside is lower cost. The catch? Approval leans hard on your income, debt load, and credit profile.

Qualification Standards

Plan on handing over full personal-income docs. DTI usually tops out around 43% to 45%, although automated underwriting may push that as high as 50%. Lenders also usually count only 75% of projected rental income when they size the loan.

Credit score minimums often begin at 620, but if you want the best pricing, you’ll usually need 740 or higher.

There’s another limit that can sneak up on investors: property count. Fannie Mae and Freddie Mac cap borrowers at 10 financed properties, and many retail lenders set their own ceiling lower, often around 4 to 6 properties.

So yes, the rate is often lower. But underwriting is tighter, and you’ll need more cash on hand at closing.

Cash Needed Upfront

For single-family rentals, down payments can start at 15%. For 2- to 4-unit properties, lenders usually want 25% to 30% down.

Reserve rules also get stricter as your portfolio grows. Lenders may require:

- 2% of the aggregate loan balance for 1 to 4 financed properties

- 4% for 5 to 6

- 6% for 7 to 10

That means the entry point can feel pretty manageable at first, then get heavier as you add more doors.

Rates and Terms

Rates usually fall in the 6.25% to 7.75% range, with better pricing going to borrowers with stronger credit and lower LTVs.

Most conventional investment loans come as 30-year fixed-rate mortgages, and they usually don’t include a prepayment penalty. Origination fees also tend to be lower, often around 0 to 1 point for well-qualified borrowers.

That’s the big tradeoff in plain English: conventional financing is often a great fit for your first few deals, but it’s not built for fast portfolio growth.

Best-Fit Strategy

Conventional loans make the most sense for investors with steady W-2 income, strong credit, and fewer than 4 to 6 properties who want low-cost fixed-rate debt.

3. Non-QM Rental Property Loans

Non-QM loans are built for borrowers whose tax returns don't show the full picture. Instead of relying on W-2s and tax returns, these loans let lenders use other ways to verify income. So if the rental deal makes sense but your paperwork doesn't fit the usual box, Non-QM can be the answer.

Qualification Standards

The big draw here is flexibility with income docs. Borrowers may qualify with 12 to 24 months of bank statements, a profit and loss (P&L) statement, or an asset depletion formula that turns liquid assets into a monthly income number. This matters for investors whose tax returns look thin because of depreciation and write-offs. On paper, they can look weak under standard DTI rules even when the cash flow is there.

That makes Non-QM a good fit when the main problem is borrower income paperwork, not the number of properties owned.

These programs also tend to be more forgiving after recent credit events like bankruptcy or foreclosure. Minimum FICO scores often start around 620 to 640, while 720 to 740+ tends to open the door to the best rates and the most leverage. Investors may also close in the name of an LLC or corporation for liability protection.

Cash Needed Upfront

Most Non-QM rental loans call for 20% to 30% down or 70% to 80% LTV. Some niche programs can go as high as 85% LTV for borrowers with high FICO scores. Reserve rules usually land at 3 to 6 months of PITIA in liquid funds.

One small but useful detail: if you're using bank statements to qualify, personal account statements can sometimes show more usable income than business accounts. Why? Lenders often don't apply an expense ratio to personal deposits.

Rates and Terms

As of May 2026, bank statement loans are pricing around 7.25% to 8.25% for a 740 FICO borrower at 75% LTV, while asset depletion loans are usually around 7.00% to 8.00%. Lower credit scores can add about 200 basis points.

Many Non-QM programs also offer 40-year fixed terms and interest-only periods, which can help monthly cash flow. The tradeoff is simple: you build equity more slowly. Prepayment penalties are also common, often set up as step-down penalties. So if you plan to refinance or sell soon, read those terms closely before closing.

You pay more for this type of flexibility. The question is whether easier documentation and deal access matter more than getting the lowest rate.

Best-Fit Strategy

Non-QM works best as the backup plan when cash flow or assets matter more than tax-return income. It's often a strong match for self-employed and 1099 borrowers whose bank deposits support the loan better than their tax returns do. It also helps investors who have hit the conventional financing cap and need more room to keep buying.

It can also help at the refinance stage. If conventional DTI is killing the deal, Non-QM may let you refinance a stabilized property without that same hurdle. And if a property's DSCR is too thin to stand on its own, bank statement income may still get the borrower qualified.

4. Portfolio Loans

When conventional loans or DSCR loans start slowing you down, portfolio loans can help you keep buying. Instead of financing each rental one by one, one lender can roll several properties into a single loan. These are in-house mortgages that the lender keeps on its own books, which means it can make its own rules around income documents, property types, and how many properties you own.

A blanket loan can group 3 to 25 properties into one mortgage with one monthly payment.

Qualification Standards

With portfolio loans, lenders usually look at the cash flow of the full group of properties instead of judging each one on its own. In most cases, they want a blended DSCR of 1.15x to 1.25x.

Credit score minimums often start at 660, and stronger scores usually lead to better pricing and terms. Paperwork can be more flexible, but the process is often more hands-on than agency lending. Lenders also tend to like borrowers who already have at least 12 months of rental property management experience. These loans can be made in the name of an LLC, S-corp, or trust.

That setup works well for investors who have moved past single-property underwriting and need a lender that can look at the bigger picture.

Cash Needed Upfront

You should plan for a down payment of 20% to 30%. LTV caps usually fall between 70% and 80%.

Reserve rules are also tougher than with many other loan types. A lender may ask for around 6 months of PITIA for the portfolio loan, and on larger holdings, sometimes 3 to 6 months per property. Closing costs can also run higher than a one-property loan because the underwriting is more manual.

Rates and Terms

As of mid-2026, portfolio loan rates usually range from 6.5% to 10%. That's often 1% to 3% higher than conventional loan rates. Terms are often set up as 5-, 7-, 10-, or 15-year loans, and some come with balloon payments. Most also include a 3-to-5-year prepayment penalty.

One feature worth pushing for at the start is a partial release clause. This gives you a way to sell one property from a blanket loan, usually by making a partial paydown, without having to refinance the rest of the portfolio. Since the lender keeps the loan in-house, origination fees and interest-only options may also be more flexible.

Best-Fit Strategy

Portfolio loans make sense for investors who want to bundle properties, cut down on separate payments, or keep growing after they run into agency loan limits. They tend to fit best once you've reached the 10-property conventional financing cap or when you're buying several properties in one deal. They can also help if you want to fold multiple mortgages into one payment.

The big tradeoff is cross-collateralization. Each property backs the full loan, so if you miss one payment, the entire group of properties can be on the line.

5. Bridge Loans

Bridge loans are short-term, asset-based loans used to buy, renovate, or stabilize a property before you move into permanent financing. Terms usually last 6 to 36 months. In plain English, this is the go-to option when a property's condition, vacancy, or timeline makes long-term financing hard to get.

The big draw is speed. Bridge loans can close in as little as 5 to 21 days, which can help you go head-to-head with all-cash buyers.

Qualification Standards

Approval usually comes down to the deal itself: the property's current value, its after-repair value (ARV), the rehab plan, and your exit strategy.

Many lenders look for a 620 to 650 credit score, although some private lenders care more about the asset than the borrower profile. You also need a clear exit plan. That might mean refinancing into a DSCR loan or selling the property once the work is done. Most bridge lenders also want the property held in an LLC or corporation.

Cash Needed Upfront

Bridge loans usually top out at 65% to 80% LTV based on as-is value, or 85% to 90% loan-to-cost (LTC) for rehab deals. On renovation projects, lenders often release rehab funds in draws. That means you'll need cash ready to cover early work before the first draw hits.

Reserves matter too. Lenders often want liquid reserves equal to 6 to 12 months of debt service, plus extra room for rehab overruns. On top of that, origination fees usually run 1 to 3 points. Some lenders also charge an exit fee of 0% to 1%, plus extension fees of 0.5 to 1.0 points each time you extend the loan if the project drags on.

Rates and Terms

Bridge loans come with the highest rates in this comparison. In 2026, you can expect rates around 8% to 14%, with many investors landing in the 9% to 12% range.

Payments are almost always interest-only, which can keep monthly carrying costs lower while you're renovating or stabilizing the property. That's a big help when the property isn't ready to produce steady income yet.

Best-Fit Strategy

Bridge debt works best as a temporary tool between purchase and stabilization. It's the main financing option for the Buy and Rehab stages of the BRRRR strategy. It's also a strong choice when a property can't qualify for conventional or DSCR financing because it's vacant, in rough shape, or under active renovation.

The smart move is to plan the bridge loan around the exit loan from day one. In other words, don't just think about how fast you can buy the property. Think about how you'll get out of the bridge loan too. Size the loan around your exit timeline so a refinance or sale doesn't get stalled by seasoning rules or unfinished rehab work. Once the property is stable, move into permanent financing.

6. Cash-Out Refinance Loans

Once a property is stabilized, a cash-out refinance lets you turn built-up equity into the down payment for your next deal. This is the BRRRR exit. You replace the current loan with long-term debt and pull part of your equity out in cash.

Qualification Standards

Cash-out refis follow the same two underwriting paths as purchase loans:

- Conventional: based on your personal income

- DSCR: based on the property's rental income

For DSCR loans, lenders may use 75% of gross rent before they calculate DSCR.

Credit score minimums usually fall in these ranges:

- DSCR: 620 to 680

- Conventional: 660 to 700+

Seasoning also matters. Most lenders want you to own the property for 6 to 12 months before they let you tap equity based on the new appraised value. Some DSCR programs go as low as 3 months, and delayed financing exceptions may apply if you bought the property with cash.

Once you know which lane you fit into, the next step is simple: figure out how much equity you can pull without putting too much pressure on monthly cash flow.

Cash Needed Upfront

In most cases, you bring little or no cash to closing. But you still need to leave equity in the property.

Conventional programs usually cap cash-out at 70% to 75% LTV. DSCR programs can sometimes go a bit higher, up to 75% to 80% LTV on single-family rentals.

Closing costs usually land around 2% to 5% of the new loan amount. On top of that, lenders often want 6 to 12 months of PITIA in liquid reserves after closing.

One thing people sometimes miss: check your current loan for a prepayment penalty before you refinance. DSCR and hard money loans often come with step-down penalties, like 5-4-3-2-1 over five years, and that can eat into your net proceeds.

Rates and Terms

In mid-2026, DSCR cash-out rates were roughly 7.0% to 9.0%, based on LTV, credit score, and property type. Borrowers with strong credit, solid DSCR, and 12+ months of seasoning could get closer to 6.5% to 7.625%.

| Property Type | Max LTV | Min DSCR | Rate Range (Mid-2026) |

|---|---|---|---|

| Stabilized SFR | 75% | 1.15x | 7.0% – 7.75% |

| 2–4 Unit Multi-Family | 75% | 1.20x | 7.25% – 8.0% |

| Short-Term Rental | 70% | 1.20x | 7.75% – 8.75% |

| Lower-credit borrowers | 65–70% | 1.25x | 8.25% – 9.0% |

Source: PeerSense

Loan terms include 30-year fixed, 40-year fixed, and interest-only options. Before you apply, run the numbers on the post-refi DSCR using the new loan balance. If you push that ratio right down to the minimum, the deal can start to feel tight later.

The rate matters, of course. But the bigger issue is whether the new payment still fits your exit plan and leaves enough room for the next purchase.

Best-Fit Strategy

This loan is made for the refinance step of BRRRR. After the property is rehabbed, rented, and stabilized, you pull equity out and use it for the next deal.

A good example came from Tampa in May 2026. An investor owned a rental worth $510,000 with an existing balance of $280,000. They completed a DSCR cash-out at 75% LTV and netted $90,500 after closing costs. That money went straight into the down payment for the next buy.

DSCR cash-out tends to work best for investors who want to recycle equity without going through personal-income underwriting. Conventional cash-out is a better fit for borrowers who still meet agency rules. The right pick depends on your paperwork, how fast you want to scale, and whether the new payment still leaves the property cash-flowing.

Qualification, Cost, and Strategy Tradeoffs

The core tradeoff is pretty simple: the easier a loan is to qualify for, the more it usually costs. Every loan is built around a different kind of risk. Some lenders focus on borrower income. Others care more about property income, asset value, or how the full portfolio performs. That choice affects pricing, leverage, and how fast the deal can close.

In most cases, conventional loans cost the least. DSCR and Non-QM loans usually come with higher pricing, but they give you more room on income rules. And the more flexible the loan gets, the more cash you’ll often need up front.

There’s also a clear speed-versus-cost tradeoff. Conventional loans are usually the slowest to close, but they’re also the cheapest. DSCR loans tend to move faster and give you more flexibility. Bridge loans sit at the other end of the spectrum: fastest and most expensive.

Here’s the side-by-side view:

| Loan Type | Underwriting Basis | Typical Leverage | Closing Speed | Ideal Use Case |

|---|---|---|---|---|

| Conventional | Personal income / DTI | Higher | Slowest | First purchases; cost efficiency |

| DSCR | Property cash flow | Moderate–High | Faster | Scaling portfolios; LLC vesting |

| Non-QM | Bank statements / assets | Moderate | Moderate | Self-employed; complex income |

| Portfolio | Lender-specific | Moderate | Moderate | Multi-property consolidation |

| Bridge / Hard Money | Asset value / exit strategy | Highest | Fastest | Distressed acquisitions; BRRRR |

| Cash-Out Refi | Equity / appraisal | Moderate | Moderate | Equity recycling for next purchase |

A common investor playbook is "Conventional first, DSCR later." The idea is straightforward. Use agency debt for the first one to four properties so you can lock in the lowest rates. Then switch to DSCR when your tax returns, DTI, or property count start making conventional underwriting less efficient.

That’s often where the tradeoffs come into focus. Conventional debt works best when cost matters most. DSCR makes sense when you want to scale. Non-QM can fit borrowers with messy or hard-to-document income. Portfolio loans help when you want to bundle properties. And bridge loans are built for speed.

Pros and Cons

Every loan type has a lane where it shines. And every loan type has a point where it starts to fall apart.

That’s why the table below boils things down to the tradeoffs investors care about most: cost, speed, flexibility, and scale.

| Loan Type | Key Advantages | Key Limitations |

|---|---|---|

| Conventional | Lowest rates; no prepayment penalty; high leverage on simple deals | Strict DTI; 10-property cap; usually requires personal-income qualification |

| DSCR | No personal income docs; LLC-friendly; fast closings | Higher rates; prepayment penalties common; reserve needs can be higher |

| Non-QM | Fits self-employed borrowers; bank statements or assets can qualify | Higher rates; less standardized terms |

| Portfolio | Flexible for bundled or nonstandard deals | Lender-specific terms; less standardized; possible balloon payment |

| Bridge / Hard Money | Fastest to close; works for distressed or rehab deals | Highest rates and points; short terms; tight refinance window |

| Cash-Out Refi | Taps equity without selling; funds the next deal | Needs equity, appraisal support, and seasoning |

Use these tradeoffs to line up the loan with your income profile, hold time, and growth plan.

That leads to the next step: figuring out which loan fits your strategy best.

Conclusion

The right loan is the one that fits your strategy, income profile, and exit timeline.

Once you compare cost, speed, and underwriting, the choice is usually pretty clear. Start with conventional loans for your first properties. Then move to DSCR loans when your property count, DTI, or LLC setup starts making conventional financing a bottleneck.

Use bridge loans for acquisition or rehab before you move into permanent financing. And if you're self-employed and claim heavy write-offs, DSCR or a bank statement loan is often a better match.

Match the loan to the strategy first. Then run the numbers.

FAQs

How do I choose between DSCR and conventional?

Choose conventional if your main goal is the lowest rate, your W-2 income is easy to document, you own fewer than four or five properties, and you can wait 30 to 45 days to close.

Choose DSCR if you’re self-employed, maxed out on DTI, need to close in an LLC, or you’ve hit the 10-property agency limit. Rates are usually 0.5% to 1.5% higher, but approval is based on the property’s debt service instead of your personal income.

When should I use a bridge loan?

Use a bridge loan when you need speed, flexibility, or renovation funds that permanent financing can’t offer. It’s often a good fit for fix-and-flip deals, the buy-and-rehab phase of a BRRRR strategy, distressed properties, or auction purchases where a fast closing matters.

Bridge loans usually come with higher rates and fees, so they make the most sense as a short-term tool, often 6 to 24 months. That’s why you need a clear exit plan from day one, like refinancing into a long-term DSCR or conventional loan.

What loan works best for BRRRR?

BRRRR usually uses two loans, one after the other.

First comes a bridge or hard money loan. That loan covers the purchase and the renovation. It also gives investors the speed they need to close on distressed properties and pay for rehab work, usually with a 12- to 18-month term.

Once the property is renovated, rented out, and stable, investors usually refinance into a DSCR loan for long-term financing.