Short-Term Rental DSCR Loans: How to Finance Your Airbnb Investment

If your Airbnb can cover its own payment, a DSCR loan may let you buy it without using W-2s, pay stubs, or tax returns. For most short-term rental deals, I’d expect lenders to check whether the property hits about 1.00x to 1.25x DSCR, ask for roughly 15% to 25% down, and want 3 to 12 months of PITIA reserves.

Here’s the short version:

- DSCR = qualifying rental income ÷ PITIA

- For Airbnb properties, lenders often cut projected income by 10% to 25%

- Income usually comes from AirDNA, Airbnb/Vrbo history, or an STR appraisal

- Many lenders want at least 640 credit

- These loans are for non-owner-occupied investment properties only

- Zoning, permits, and HOA rules can stop a deal even if the math works

- A deal that only barely clears 1.00x DSCR may be too tight for slow months

A simple example: if a property is projected to bring in $96,000 per year, and the lender applies a 25% haircut, they may count $72,000. That’s $6,000 per month. If PITIA is $5,000, DSCR is 1.20x.

Will This $1.4M Airbnb Investment Deal Actually Get Financed?

sbb-itb-e7c549b

Quick comparison

| Item | Short-Term Rental DSCR | Long-Term Rental DSCR |

|---|---|---|

| Income used | AirDNA, booking history, STR appraisal | Lease or rent schedule |

| Income treatment | Usually reduced by 10% to 25% | Often lease income is used as-is |

| Common DSCR target | 1.00x to 1.25x | 1.00x+ |

| Reserves | Often 6 to 12 months PITIA | Often 3 to 6 months PITIA |

| Extra checks | HOA, zoning, permit rules | Fewer STR rule issues |

If I were sizing up this loan type, I’d focus on four things first: cash flow, down payment, reserves, and local STR rules. That tells me fast whether the deal has a shot or whether it falls apart under a lender’s review.

How DSCR Loans Work for Short-Term Rentals

Short-term rental DSCR loans use a property’s projected or actual Airbnb income to cover PITIA. But lenders don’t just glance at one strong month and call it good. They usually test income across a 12-month period to account for seasonality.

That’s the big shift with this loan type: personal income matters less than the property’s income pattern. Lenders look at Airbnb income data, booking history, and occupancy trends. So in most short-term rental DSCR files, the main issue is simple: How well can the rent be documented?

Most U.S. lenders want a minimum DSCR of 1.00 to 1.25 for short-term rentals. A 1.25 ratio gives the lender a 25% cushion. Some programs go as low as 0.75, but there’s a catch. Those deals usually need stronger reserves and bigger down payments, often 25% to 30% down and as much as 12 months of PITIA in reserves. When the DSCR drops, lenders usually want more strength somewhere else, such as reserves, equity, or credit.

After that, the next step is where things get a little more nuanced: lenders often adjust the income figure before they apply the ratio.

How Lenders Calculate DSCR on Nightly Rental Income

The formula itself is straightforward: monthly gross rental income divided by PITIA.

The tricky part is the income input. Lenders don’t usually use short-term rental gross income at face value. Instead, they normalize it first. In plain English, they trim the number to account for vacancy, seasonality, and the ups and downs that come with nightly rentals. Most lenders apply a 10% to 25% discount before calculating DSCR.

That adjusted income figure is the number that gets divided by PITIA.

Lenders usually accept income documentation in one of three ways:

- AirDNA market projections for the subject property address

- 12 to 24 months of actual booking statements from Airbnb or Vrbo

- A short-term rental appraisal based on local comps

Short-Term Rental DSCR vs. Long-Term Rental DSCR

Long-term rental DSCR is usually built on lease income. Short-term rental DSCR leans on projected or past income, then applies a lender discount. That one change has a big effect on how much income the lender is willing to count.

It also explains most of the underwriting gap between long-term and short-term rental DSCR loans.

| Feature | Long-Term Rental DSCR | Short-Term Rental DSCR |

|---|---|---|

| Income Basis | Signed lease or 1007 rent schedule | AirDNA projections or booking history |

| Lender Discount | Typically 0% (100% of lease used) | 10%–25% discount on projected revenue |

| Typical Min. DSCR | 1.00 (0.75 with exceptions) | 1.00–1.25 (0.75 with exceptions) |

| Reserve Requirement | 3–6 months PITIA | 6–12 months PITIA |

| Interest Rate | Standard DSCR pricing | +0.25% to +0.50% premium |

| Local Rules | Not typically required | Local permit and zoning checks |

How to Qualify Using Projected Airbnb Income

For properties with no lease and no booking history, lenders use projected Airbnb income based on documented market data. That’s how investors can finance a new short-term rental before it has a single prior booking.

Income Sources Lenders Accept for Airbnb Qualification

AirDNA is the most common source for income projections. For properties with 12 to 24 months of operating history, lenders may also accept earnings statements from Airbnb or Vrbo. Another option is a short-term rental appraisal that uses STR comps. That income then goes into the DSCR test.

Lenders usually cut the gross annual projection by 20% to 25%, then divide the result by 12 to get monthly qualifying income. So if a property is projected to make $96,000 per year in gross STR revenue, and the lender applies a 25% discount, qualifying income drops to $72,000 per year, or $6,000 per month.

DSCR Calculation Examples Based on Airbnb Revenue Scenarios

The table below shows the main income and debt items lenders look at:

Inputs Used to Calculate DSCR on a Short-Term Rental

| Category | Example Items | Typical Source |

|---|---|---|

| Gross Income | Annualized booking revenue | AirDNA report, Airbnb/Vrbo statements, STR appraisal |

| Income Adjustments | 20%–25% vacancy/seasonality underwriting discount | Lender underwriting guidelines |

| Debt Service (PITIA) | Principal, interest, taxes, insurance, HOA | Loan Estimate, insurance quote, tax records |

Here’s what that looks like with actual numbers. A property in a coastal market projects $96,000 in gross annual STR revenue. After a 25% underwriting discount, qualifying income falls to $72,000 per year, or $6,000 per month. If monthly PITIA is $5,000, the DSCR comes out to 1.20. That clears the 1.00 minimum and sits close to the 1.25 mark, which often helps with pricing.

Now the flip side. If the AirDNA projection is lower, at $78,000 gross, and the lender still applies a 25% discount, monthly qualifying income falls to $4,875. With the same $5,000 PITIA, DSCR drops to 0.975. That lands below the common qualifying range of 1.00 to 1.25.

The math is pretty simple: take the AirDNA projection, apply the lender’s discount, divide by 12, and compare that number with PITIA. If the ratio meets the lender’s minimum, the file can move on to credit, down payment, reserves, and property review in the next section.

Qualification Requirements and the Loan Process

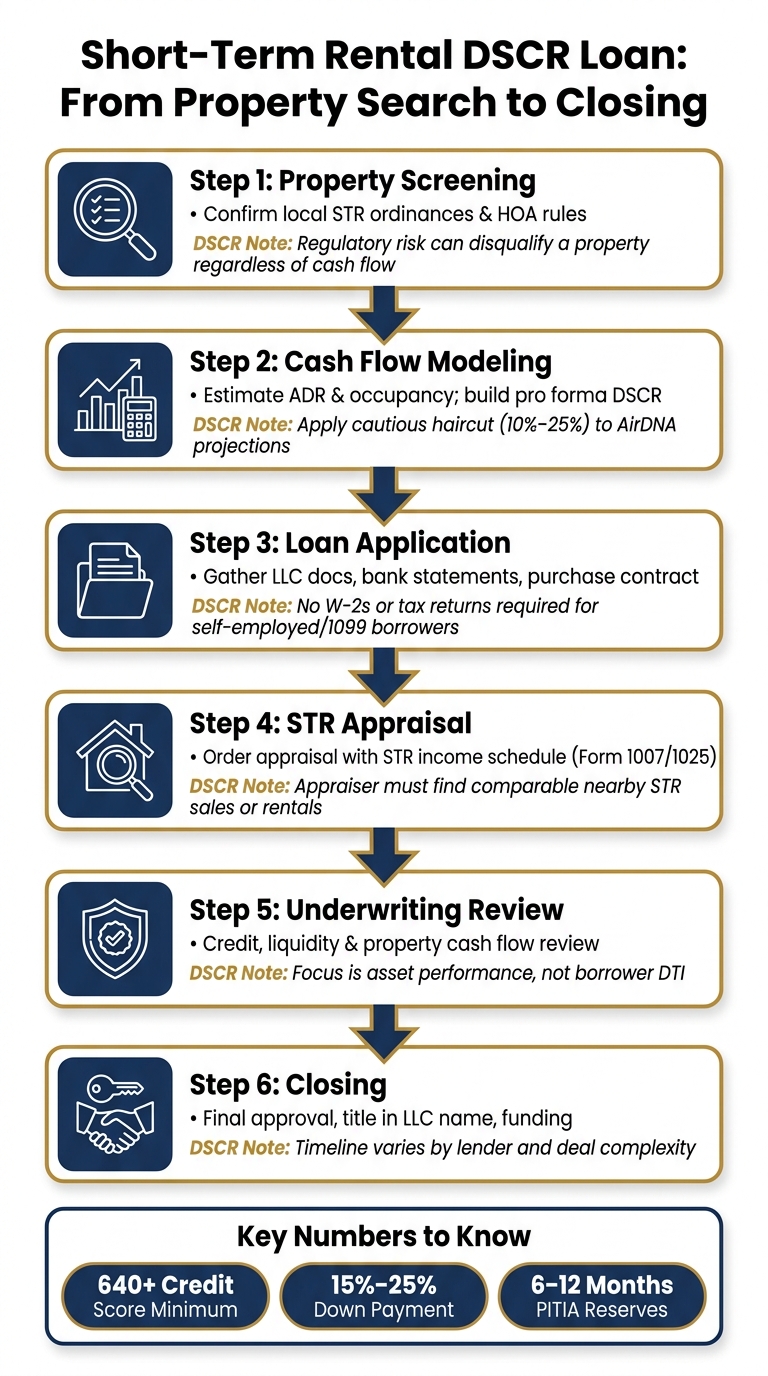

Short-Term Rental DSCR Loan Process: From Property Search to Closing

Once the DSCR gets past the minimum, lenders shift their attention to three things: your credit, your cash, and the property itself.

Credit Scores, Down Payments, Reserves, and Property Rules

For most short-term rental DSCR programs, the minimum credit score starts around 640. That opens the door for self-employed borrowers and 1099 earners. Approval is tied to the property's income, not your W-2s or tax returns, so big write-offs usually don't hurt your chances.

Most DSCR loans close in an LLC. So before you apply, make sure you have your Articles of Organization, Operating Agreement, and EIN ready. Missing entity paperwork can slow things down at the worst time.

Typical DSCR Requirements for Short-Term Rentals

| Requirement | Common Range | What Lenders Look For |

|---|---|---|

| Credit Score | 640 – 720+ | Scores of 720+ can qualify for the best rates and higher LTV limits |

| Down Payment | 15% – 25% | Most programs ask for 20%–25%, though some go as low as 15% |

| Cash Reserves | 3 – 12 months PITIA | Liquid funds to cover payments during slow seasons or vacancies |

| Borrower Type | LLC / Entity | Loans usually close in an LLC name instead of an individual's |

| Property Rules | Zoning & HOA | STRs must be allowed by the city, county, and HOA |

One issue trips up a lot of investors: HOA rules can override city or county permission. So even if the local government allows short-term rentals, a line in the CC&Rs that bans them can kill the deal. Check both before you put in an offer.

Step-by-Step: From Property Screening to Closing

The process is pretty straightforward, but it helps to know the order before you're in the middle of it.

It starts with market research. You'll pull ADR and occupancy estimates from AirDNA, then build a cautious monthly revenue model. That gives you a pro forma DSCR before you're locked into the deal. If it clears 1.00, it's worth a closer look.

Next comes the application. You'll gather the purchase contract and your entity documents, then submit everything to the lender. DSCR underwriting looks at property cash flow and your credit profile more than personal income paperwork. That means the document list is shorter than what you'd see with a conventional loan.

The appraisal is a big part of the file. It usually includes Form 1007 or 1025 plus a short-term rental revenue report. The appraiser has to find nearby comparable STR sales or rentals that support the income estimate. If those comps aren't there, the deal can get shaky fast.

From Property Search to DSCR Closing

| Stage | Primary Tasks | Key DSCR Considerations |

|---|---|---|

| Screening | Confirm local STR ordinances and HOA rules | Regulatory risk can disqualify a property no matter how good the cash flow looks |

| Modeling | Estimate ADR and occupancy; build pro forma DSCR | Use a cautious haircut on AirDNA projections |

| Application | Gather LLC docs, bank statements, purchase contract | No W-2s or tax returns are needed for self-employed or 1099 borrowers |

| Appraisal | Order appraisal with STR income schedule | Appraiser must find nearby comparable STR sales or rentals |

| Underwriting | Credit, liquidity, and property cash flow review | The focus is asset performance, not borrower DTI |

| Closing | Final approval, title in LLC name, funding | Timeline depends on the lender and the deal's complexity |

That review is what tells the lender whether the loan can move to final approval. After that, it comes down to whether the deal lines up with your investing goals.

When a Short-Term Rental DSCR Loan Makes Sense

A DSCR loan makes the most sense when the property's cash flow matters more than the borrower's tax returns. That's often the case for self-employed buyers or investors who take heavy write-offs and depreciation, which can make their income look lower on paper than it is in day-to-day life. The best setups are steady properties in STR-friendly areas, with cash flow that sits well above breakeven.

It also makes sense when the property's STR income meaningfully outpaces what it would earn as a long-term rental. If the short-term rental numbers are much stronger, DSCR financing lets you qualify based on the property's income instead of your personal earnings.

The biggest risks are regulation and seasonality. Markets with tighter STR rules can shift fast, and a property that qualifies using projected Airbnb income could later be pushed into long-term rental use and bring in less money. The same goes for single-season homes, like ski cabins. They can look great in peak months and still struggle when demand drops. Projected Airbnb income only helps if the market can support steady occupancy. A smart move is to stress-test the deal at 10 points below projected occupancy before you commit.

Good Fit Scenarios and Potential Red Flags

Here are the clearest signs that DSCR fits the deal - and where trouble can show up:

| Deal Characteristic | Favors DSCR Loan | Potential Concern |

|---|---|---|

| Borrower Income | Self-employed or high tax write-offs | - |

| Ownership Structure | Closing in an LLC for liability protection | Purchasing in a personal name |

| Property Performance | STR income is 2x–3x higher than long-term rent | Property barely breaks even as a short-term rental |

| Local Regulation | STR-friendly markets (e.g., Scottsdale, AZ; Destin, FL) | Restrictive or unstable markets (e.g., New York City, San Francisco, Maui) |

| Cash Reserves | 12+ months of PITIA available | Borrower is cash-poor after the down payment |

| Seasonality | Year-round or multi-season demand | Single-season demand with high vacancy risk |

| HOA Rules | No restrictions on short-term stays | HOA requires 30-day or longer minimum leases |

Grandfathered STR permits may not transfer to a new owner. In markets with permit caps, lenders want proof that the permit is active and transferable before closing. If the new owner has to apply again, the deal may stop making sense.

"A loan that clears 1.01 DSCR on projected income is not a cushion; it is a warning light." - David Park, Financial Planner

If the deal only works at peak occupancy, the margin is too thin. There isn't much room for slow months, repairs, or surprise costs. If the property only barely clears the numbers, walk away.

FAQs

Can I qualify with no Airbnb history?

Yes. You can still qualify for a DSCR loan even if the property has no Airbnb history.

When that happens, lenders usually look at projected income instead of past short-term rental performance. They may use a third-party market report or an appraiser’s market study based on similar local properties.

One catch: many lenders trim those income estimates by 10% to 25% to account for risk and seasonality. So before you move forward, confirm which method your lender accepts and how they adjust the numbers.

What counts against DSCR on an STR loan?

On a short-term rental DSCR loan, DSCR measures the property’s gross rental income against its total debt payments, or PITIA: principal, interest, taxes, insurance, and any association dues.

Put simply, the lender wants to see whether the rent coming in can cover the property’s monthly costs.

Most lenders also trim projected STR income by 10% to 25%. In some cases, they cut it by 30% to 50% to make room for vacancy, seasonality, and management costs. If debt service goes up, or income comes down, the ratio drops.

What can kill an STR deal besides cash flow?

Beyond cash flow, an STR deal can fall apart for a bunch of other reasons.

Local rules are a big one. City regulations, zoning limits, or HOA/condo rules can block short-term rentals outright. And if that happens, the deal can die fast.

Other common problems show up during financing and underwriting. Appraisal issues can throw off the numbers. Missing STR-specific insurance can stop the loan from moving forward. Thin cash reserves can make a borrower look too risky. And if the property's use is listed the wrong way - like calling an investment property a second home - that can derail the deal too.

This is why STR financing isn't just about whether the property makes money on paper. The details around legality, insurance, reserves, and occupancy type matter just as much.