Blanket Mortgage for Multiple Properties: Is It the Right Move for Portfolio Investors?

If I own 5+ rentals and plan to hold them, a blanket mortgage can cut paperwork and combine cash flow - but it also links every property to the same debt. That’s the tradeoff in one line.

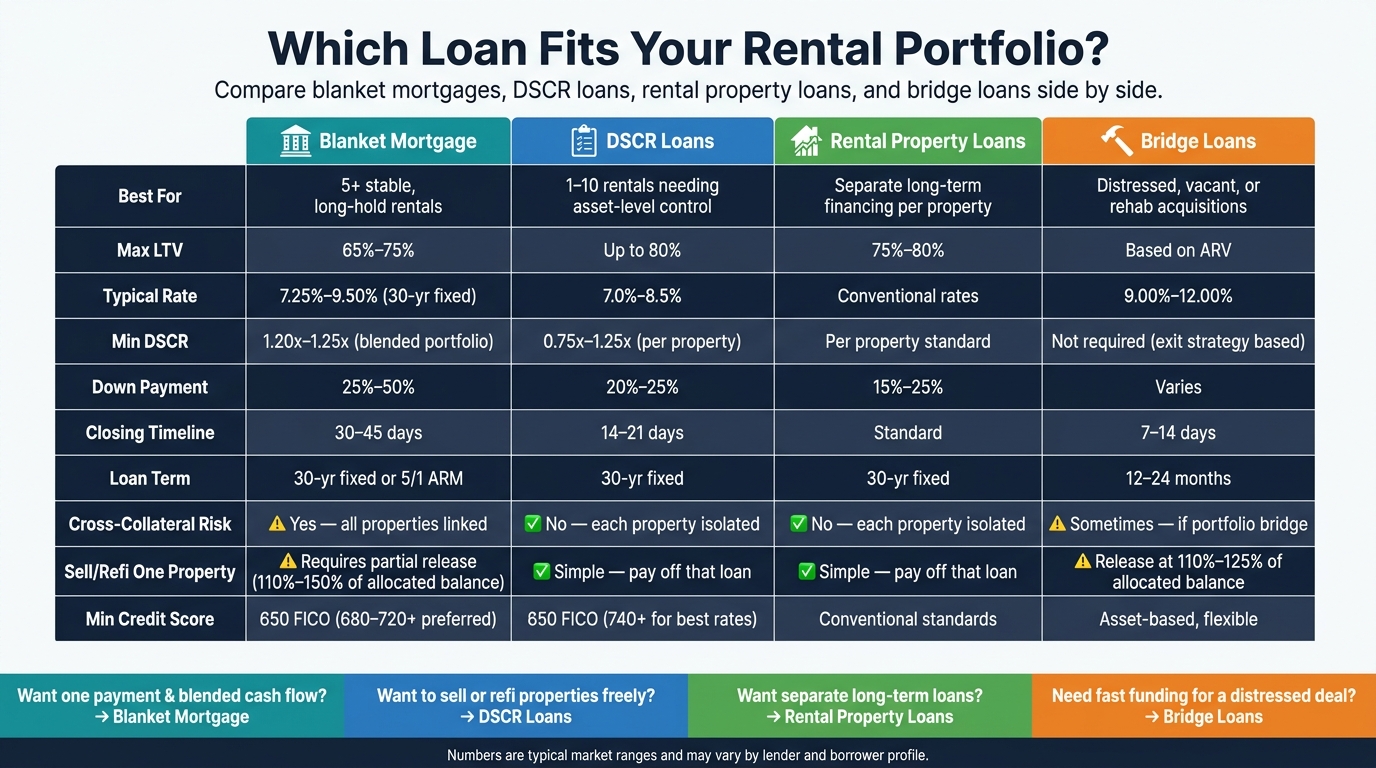

Here’s the short answer:

- Blanket mortgage: best when I want one loan for several properties and can live with cross-collateral risk

- DSCR loans: best when I want each property on its own loan and easier sales or refinances

- Rental property loans: best when I want long-term separate financing and don’t mind more loan files

- Bridge loans: best when I need short-term funding for a purchase, rehab, or cleanup before a refinance

A few numbers matter right away:

- Blanket loans often land around 65% to 75% LTV

- Blended DSCR often needs 1.20x to 1.25x

- DSCR loans can go up to 80% LTV

- Bridge loan rates often run about 9.00% to 12.00%

- Blanket loan release prices may land near 110% to 150% of the released property’s share

So, is a blanket mortgage the right move? Usually yes for stable portfolios and long holds. Usually no if I expect to sell properties one by one, do a 1031 exchange, or keep risk split by asset.

Blanket Mortgage vs. DSCR vs. Rental & Bridge Loans: Portfolio Investor Guide

Why Smart Investors Think Twice About Blanket Mortgages

sbb-itb-e7c549b

Quick Comparison

| Loan type | Best use | Main upside | Main risk |

|---|---|---|---|

| Blanket mortgage | 5+ stable rentals | One payment and blended cash flow review | One default can affect all properties |

| DSCR loan | 1–10 rentals with property-level control | Easy to sell or refinance one property | Each asset must qualify on its own |

| Rental property loan | Long-term financing per property | Each loan stands alone | More files, more lender work |

| Bridge loan | Distressed, vacant, or rehab deals | Fast short-term funding | High rates and short payoff window |

My view: a blanket mortgage is less about rate and more about control vs. consolidation. If I want fewer moving parts, it can work well. If I want freedom to sell, refinance, or isolate trouble at one address, separate loans are often the better pick.

Below, I’d break down where each option fits, what numbers to watch, and when one loan starts to help more than it hurts.

1. Blanket Mortgage

Collateral and Release Flexibility

A blanket mortgage places one lien across every property in the pool. That makes admin easier, but it also increases the stakes: if one asset goes into default, the whole portfolio can be at risk. Put simply, one problem property can put every property in the pool on the line.

The next issue is simple: can the portfolio's cash flow carry the debt?

A release clause gives you a way to sell one property without paying off the full loan. But there's a catch. The lender will set a release price. Try to push that number closer to 110% at closing. If the release price lands at 150%, it can tie up too much equity in the rest of the portfolio and shrink your room to move.

Qualification and Cash Flow Underwriting

Lenders look at the portfolio as one package. That means stronger properties can help offset weaker ones in the portfolio DSCR, and the blended performance of all assets decides whether the loan clears underwriting.

In most cases:

- Credit minimums usually start at 650 FICO

- Many lenders prefer 680 to 720+ for better pricing

- Down payments often fall between 25% and 50% of the combined property value

- Lenders often want at least six months of liquid reserves after closing

- Most loans need to close in an LLC or corporation

Leverage and Term Structure

Rates often land around 7.25% to 9.50% for a 30-year fixed and 6.75% to 8.75% for a 5/1 ARM. Origination fees usually run 0.5% to 2% of the total loan amount.

The scale can help on costs. If you pool five $200,000 properties into one $1,000,000 loan, you may save $15,000 to $25,000 in closing costs.

Many blanket loans also come with a step-down prepayment schedule, often 5-4-3-2-1%. That gives investors a clearer picture of exit costs over a five-year hold.

Best-Fit Investor Scenarios

This setup tends to work best for investors with five or more properties, borrowers getting close to the 10-financed-property limit, or buyers picking up a small portfolio in a single deal.

It usually makes less sense for near-term sales or 1031 exchange properties, where release clauses can make things more rigid.

If you want financing based on cash flow without linking several properties to a single lien, DSCR loans are the next option to compare.

2. DSCR Loans

Collateral and Release Flexibility

A DSCR loan works very differently from a blanket mortgage. It uses a "one property, one loan, one lien" setup. That means each property is financed on its own. If one asset hits a rough patch, the rest of the portfolio isn't pulled into the problem.

Selling is simpler too. You just pay off the loan tied to that property. There’s no need to work through a partial release or get sign-off tied to the rest of the portfolio. The same setup can make 1031 exchanges much easier on a property-by-property basis, since you don’t have to disturb your other financing.

That split also affects how lenders look at income, leverage, and exit plans.

Qualification and Cash Flow Underwriting

DSCR loans don’t use personal income verification. Instead, the main question is simple: does the property bring in enough rent to cover the debt?

Lenders figure DSCR by dividing monthly gross rental income by PITIA, which includes principal, interest, taxes, insurance, and HOA fees. Most programs look for a minimum ratio between 0.75x and 1.25x. And each property has to stand on its own.

Credit still matters. A minimum FICO score of 650 is common, while borrowers at 740+ usually get the best rates and can reach the top-end 80% LTV.

Leverage and Term Structure

Individual DSCR loans usually go up to 80% LTV on purchases and 75% on cash-out refinances. Rates often land between 7.0% and 8.5%.

Costs and timing are part of the appeal here. Closing costs tend to run about $4,000 to $7,000 per property. And these loans often close in 14 to 21 days, compared with 30 to 45 days for many blanket mortgages.

Best-Fit Investor Scenarios

Individual DSCR loans are often a better fit for investors with fewer than five properties, where the admin upside of a blanket loan may not be worth much. They also make sense for short holds, like renovations, planned sales, or 1031 exchanges, where being able to exit one property cleanly matters more than bundling everything together.

In plain English, these loans fit smaller portfolios and properties that need a clean payoff at the asset level. If the goal is long-term financing tied to each property, without cross-collateralizing the full portfolio, rental property loans are the next comparison.

3. Rental Property Loans

Collateral and Release Flexibility

Rental property loans finance each property separately, which gives investors a lot more room to move. If you sell or refinance one property, it doesn't affect the rest of the portfolio.

That matters in practice. You pay off the loan tied to that one property and move on. There’s no partial release process and no lender approval tied to your other assets. If you want every property to stand on its own loan, this setup keeps things simple and flexible.

Qualification and Cash Flow Underwriting

Lenders underwrite each property based on that property’s own performance, while still using conventional borrower-level qualification standards. The rent also needs to cover the debt at the property level.

Leverage and Term Structure

Individual rental loans often allow up to 75%–80% LTV, with down payments in the 15%–25% range. That’s lower than blanket mortgages, which may call for 25%–50% down.

Best-Fit Investor Scenarios

Rental property loans are a strong fit for investors who want separate long-term loans for each property and may sell properties one at a time. If the deal is more short-term - like a purchase with a rehab plan - bridge loans are the next option to compare.

4. Bridge Loans

Collateral and Release Flexibility

Bridge loans can also cover more than one property under a single short-term note. When that happens, the same cross-collateralization risk shows up here too. With portfolio bridge loans, cross-collateralization still applies, and partial releases usually call for 110% to 125% of the released property's allocated balance.

The big difference is how the lender looks at the deal. With bridge debt, the first question usually isn't long-term rental income. It's whether the property can be stabilized and exited cleanly.

Qualification and Cash Flow Underwriting

Bridge loans are underwritten based on asset value, rehab feasibility, and exit strategy, not current rent. Lenders pay close attention to ARV, the rehab plan, and how you plan to get out of the loan.

That makes bridge financing a short-term fix for a timing issue, not a long-range portfolio play. It's often used for distressed or vacant properties that don't yet qualify for permanent financing. Lenders still want a clear and realistic exit, whether that's a sale or a refinance after the property is stabilized.

Leverage and Term Structure

Bridge loans are built for speed and short holding periods. Terms usually run 12 to 24 months, and some lenders can close in as little as 7 to 14 days. That's a big edge when you're bidding on a distressed portfolio or trying to win an auction deal.

The downside is price. Interest rates on bridge portfolio loans currently range from 9.00% to 12.00%, with origination fees of 0.5% to 2%. Many of these loans are set up as interest-only during the term, which can ease cash flow while the properties are under renovation or being stabilized.

Best-Fit Investor Scenarios

Bridge loans make sense when the properties aren't ready for long-term financing. If you're buying a distressed portfolio, rehabbing several properties at the same time, or acquiring multiple parcels in one shot, bridge financing gives you room to move fast.

A common path looks like this:

- Use bridge financing to buy and stabilize the properties

- Refinance into a long-term blanket loan, DSCR loan, or separate rental loans once the assets qualify

After the properties are stabilized, the focus shifts from speed to picking the loan structure that fits the next stage best.

Pros and Cons for Portfolio Investors

Each financing option fixes a different issue. The best fit comes down to where you are in your portfolio, how much room you want to maneuver, and how much extra admin work you're ready to deal with. The comparison below helps you weigh flexibility, cash flow, and exit risk.

| Factor | Blanket Mortgage | Individual DSCR Loans | Rental Property Loans | Bridge Loans |

|---|---|---|---|---|

| Key Pros | One payment, one lender; blended DSCR lets stronger properties carry weaker ones | Asset-level flexibility; sell or refinance any property independently | Separate long-term loans; each property stands alone | Short-term financing for buying or rehabbing distressed properties before refinancing |

| Key Cons | Cross-collateralization puts the full portfolio at risk if one property defaults | Multiple payments and lenders; each property must qualify independently | Conventional lenders generally cap investors at 10 financed properties | High rates and short terms require a clear exit |

| Best For | Seasoned investors consolidating 5+ properties | Investors scaling 1–10 properties who want asset-level control | Investors who need each property on its own long-term loan | Investors acquiring or rehabbing distressed properties before permanent financing |

The main gap here isn't just price. It's how much control you keep over each property.

The biggest day-to-day edge of a blanket mortgage is the blended DSCR. Instead of forcing every single property to stand on its own, the lender can look at the portfolio as a whole. That can make a big difference if a few properties are strong and a few are lagging.

As Georgey Tishin of Sinai Capital says:

"Weaker properties get carried by stronger ones (blended DSCR). This is one of the biggest advantages of portfolio lending."

That's the heart of the tradeoff. You may cut down on closing work and simplify payments now, but you give up some freedom later. If you want to sell, refinance, or separate one property, that structure can get in your way.

Those tradeoffs are what shape when a blanket mortgage makes sense.

When a Blanket Mortgage Is the Right Move

A blanket mortgage tends to work best when your rental portfolio is already stable and you plan to keep it for the long haul. In that setup, one loan, one payment, and blended underwriting can make life a lot easier. Stronger properties can help offset weaker ones across the same pool, which is where consolidation starts to pay off.

It can also be a smart move for investors who want to keep growing once conventional financing starts to feel clunky. Instead of sizing up each property on its own, the lender looks at the full rental pool. That can make it easier to scale without stacking one separate loan on top of another.

In most cases, blanket loans make the most sense for experienced investors with strong DSCR and larger down payments.

For newer portfolios, planned sales, or 1031 exchanges, separate DSCR loans are often the better fit. For distressed or transitional assets, bridge loans usually make more sense. And if your portfolio has a bit of everything, a hybrid setup can be the better call. The main idea is simple: match the loan to the stage of the portfolio, not just the rate.

| Investor Goal | Most Suitable Loan Type | Primary Caution |

|---|---|---|

| Consolidate 5+ stable rentals | Blanket Mortgage | All properties share the same risk |

| Maximize flexibility to sell or exchange | Individual DSCR Loans | More loans, more paperwork |

| Acquire or rehab distressed assets | Bridge Loan | High rates and short repayment windows |

| Scale past conventional financing limits | Blanket Mortgage | Down payments up to 50% and stricter qualification |

| Isolate risk per property | Individual DSCR Loans | Harder to qualify if individual properties have low cash flow |

FAQs

How does a blanket mortgage affect my ability to sell one property later?

Usually, you can sell one property only if the loan has a partial release clause.

That clause lets you remove one property from the mortgage by paying a set portion of the loan balance, often with money from the sale.

Once that payment is made, the lender releases its lien on that property. The other properties stay tied to the same loan.

Without this clause, selling a single property usually means paying off the entire loan.

What is a good release clause for a blanket loan?

A good release clause uses clear, mechanical terms instead of lender discretion.

That means the clause should spell out a release price - often 100% to 110% of the property’s allocated loan amount - and clearly define the post-sale coverage test, such as the minimum portfolio LTV.

It also needs to be in writing before closing. And it should include a firm processing timeline, ideally 30 to 60 days, so a sale or refinance doesn’t get held up.

When should I choose separate DSCR loans instead of a blanket mortgage?

Choose separate DSCR loans when you want better risk isolation, more flexibility for each property, and simpler exit strategies.

With individual loans, each property stands on its own. That makes it easier to sell, refinance, or complete a 1031 exchange on one asset without needing a partial release. And if one property runs into trouble, it’s less likely to drag down the rest of your portfolio.