How to Build a Rental Property Portfolio Using DSCR Loans

If I want to grow past a few rentals, DSCR loans can make that easier because the lender looks at the property's rent, not mainly my job income.

Here’s the short version:

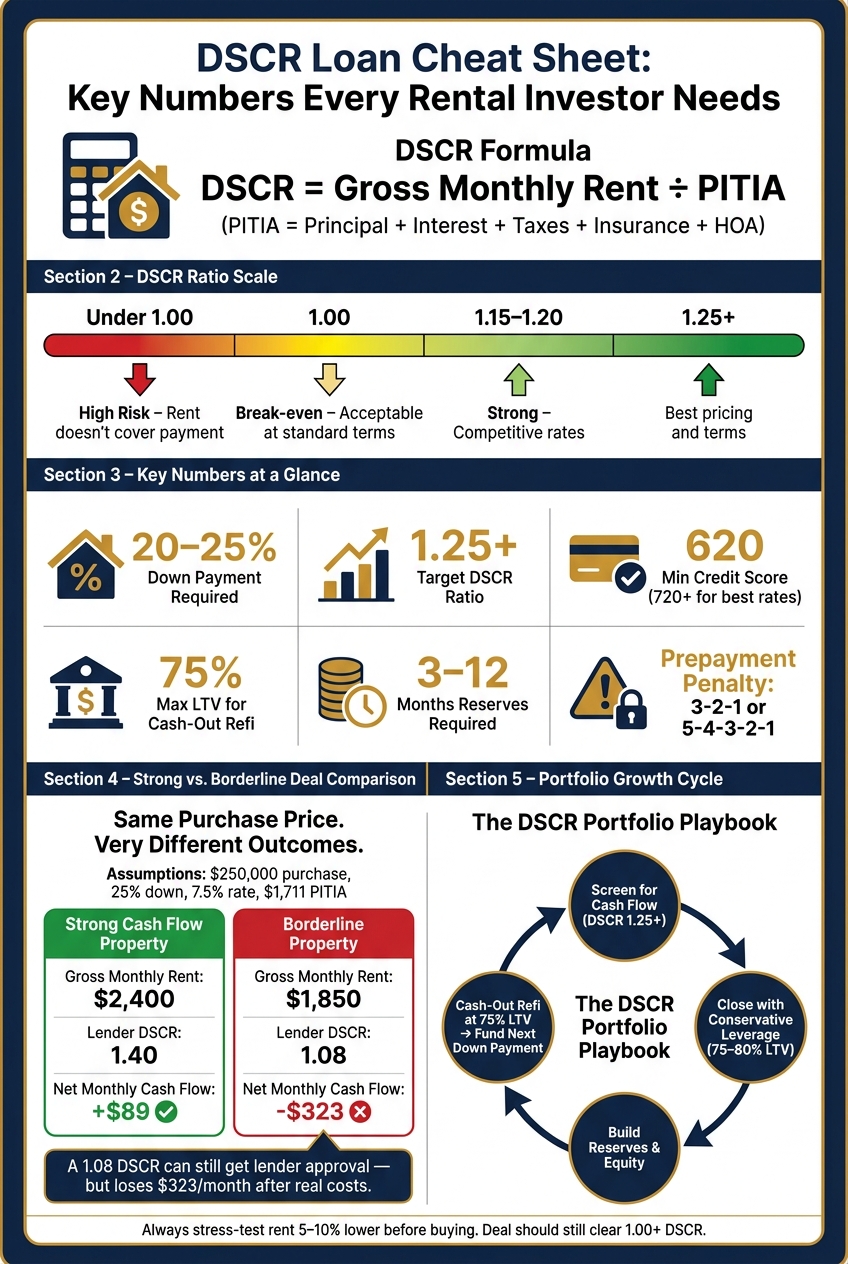

- I use DSCR = monthly rent ÷ PITIA

- Many investors target at least 1.20 to 1.25

- Most deals need 20% to 25% down

- Cash-out refis often top out around 75% LTV

- Lenders may want 3 to 12 months of reserves

- Many loans include a prepayment penalty

- The deal only works long term if the property still cash flows after vacancy, repairs, and management

In other words: a DSCR loan can help me buy rentals in a way that is tied to the property’s income. That can make it easier to keep buying, refinance later, and use equity for the next down payment.

But there’s a catch: getting approved is not the same as buying a good rental. A property can pass at 1.00 DSCR and still lose money each month once I add normal costs. That’s why I’d screen hard, keep cash on hand, and avoid thin deals.

DSCR Loan Cheat Sheet: Key Numbers Every Rental Investor Needs

70-Unit Rental Portfolio in 3 Years Using DSCR Loans (Here's How)

sbb-itb-e7c549b

Quick Comparison

| Area | What I’d watch |

|---|---|

| Qualification | Rent vs. monthly housing payment |

| Target ratio | 1.25+ is a common goal |

| Down payment | Usually 20% to 25% |

| Refinance limit | Often 75% LTV for cash-out |

| Rent proof | Lease or market rent appraisal |

| Risk points | Low cash flow, weak reserves, refi timing, penalties |

| Growth plan | Buy, lease, build equity, refi when numbers still work |

The main idea is simple: I’m not just buying one rental. I’m building a system where cash flow, leverage, and timing all need to work together.

What Are DSCR Loans and How Do They Work for Rental Properties

A DSCR loan is an investment-property mortgage that qualifies the deal based on rental income, not your personal income. That means lenders usually don't look at W-2s, pay stubs, or tax returns to approve the loan. Instead, they look at one thing first: does the property bring in enough rent to cover the monthly debt payment?

What a DSCR Loan Actually Measures

DSCR = Gross Monthly Rent ÷ PITIA (principal, interest, taxes, insurance, and HOA fees).

That's the core math behind the loan.

Say a property brings in $2,900 per month in rent and has a total PITIA payment of $2,175. The DSCR would be 1.33 ($2,900 ÷ $2,175).

Here's how lenders usually view that number:

| DSCR Ratio | What It Means | Typical Lender View |

|---|---|---|

| Under 1.00 | Rent doesn't cover the payment | High risk - requires a higher-risk structure |

| 1.00 | Break-even | Acceptable at standard terms |

| 1.15–1.20 | 15–20% cushion above debt service | Strong - competitive rates |

| 1.25+ | Solid positive cash flow | Best pricing and terms |

In plain English, the higher the ratio, the more room the property has to cover its payment. And lenders like that cushion.

One detail matters here: lenders usually calculate the ratio using the lower of the actual lease amount or the appraiser's market rent schedule. So even if a tenant is paying more, the lower figure may be the one that counts for underwriting.

Why DSCR Loans Support Portfolio Growth

The biggest structural difference between DSCR financing and conventional financing is simple: each property qualifies on its own.

Your personal debt-to-income ratio doesn't keep getting squeezed every time you buy another rental. Instead, each new property is underwritten based on its own cash flow. For investors who want to keep buying, that's a big shift.

Conventional loans backed by Fannie Mae and Freddie Mac cap most investors at 10 financed properties. DSCR programs usually don't have that cap. That's why many investors use them to grow past 10 properties and into portfolios of 20, 50, or more.

This setup also works well for LLC ownership, which conventional lenders often limit. Holding rentals in an LLC can help keep investment debt off your personal credit profile and maintain liability separation.

"The biggest barrier to scaling a rental portfolio is often financing, not finding properties. DSCR loans are designed specifically for investment property lending." - 360 Mortgage Inc.

With that structure in mind, the next move is to test whether a property's rent can support the payment.

How LoanGuys.com Works with DSCR Borrowers Nationwide

LoanGuys.com operates as a nationwide mortgage broker and direct lender focused on DSCR and non-qualified mortgage (non-QM) financing for real estate investors. Borrowers qualify based on the property's rental income and their credit profile, without tax returns or pay stubs.

The platform works for both first-time investors buying a first rental and landlords adding to a growing portfolio. Closings can happen in as little as 15 to 21 days. That speed can matter a lot when you're weighing several deals and need approval tied to the property, not your job paperwork.

Next, use DSCR to screen deals before you make an offer.

How to Calculate DSCR and Pick Profitable Rentals

Run the numbers before you make an offer. The goal isn't just getting approved. You want rentals that can help pay for the next rental too. If a property barely hangs on, it can slow your whole plan down.

Estimate NOI and Debt Service Before Making an Offer

Lenders usually calculate DSCR as gross monthly rent ÷ PITIA. For your own deal review, go a step further. Back out vacancy, maintenance, and management so you get closer to true NOI.

A simple way to do that is to budget:

- 5% to 10% for vacancy

- 5% to 10% for maintenance

- 8% to 10% for management

Also, don't rely on the seller's tax and insurance numbers. Property taxes often reset after a sale. And landlord insurance is usually a DP-3 policy, which is priced differently from a standard homeowner's policy. It pays to underwrite the deal like you'll hire a property manager from day one. That way, the property still makes sense as your portfolio gets bigger.

Many investors aim for a 1.25 DSCR. That's a common target because it gives you some breathing room when rents dip or costs climb.

A Simple DSCR Screening Method for Deal Analysis

Here's a quick screen to use before you send in an offer.

Assume a $250,000 purchase price with 25% down ($62,500). At a 7.5% interest rate, the principal and interest payment on a $187,500 loan is about $1,311 per month. Add $350 for taxes and insurance plus $50 in HOA dues, and total PITIA comes to $1,711.

Now compare two properties with that same price and loan setup. One has strong rent. The other looks close enough at first glance, but that's where people get into trouble.

| Metric | Strong Cash Flow Property | Borderline Property |

|---|---|---|

| Gross Monthly Rent | $2,400 | $1,850 |

| Total PITIA | $1,711 | $1,711 |

| Lender DSCR | 1.40 | 1.08 |

| Vacancy & Maint. (15%) | $360 | $277 |

| Management Fee (10%) | $240 | $185 |

| Net Monthly Cash Flow | $89 | ($323) - Negative |

The first property works because it leaves cash you can put back into the business. The second doesn't. It ties up your money and doesn't help you build speed.

That's the big trap with borderline deals. A property with a 1.08 DSCR may still get past the lender because it's over 1.00. But once you include normal operating costs, it loses $323 per month.

Before you buy, stress-test the rent down by 5% to 10%. The deal should still stay above 1.00 DSCR. Better yet, focus on properties that can still stay above 1.25 after that stress test. That's where extra monthly cash flow can start helping fund your next down payment.

Once a property passes this screen, the next move is checking how it fits a lender's underwriting rules.

DSCR Loan Requirements and Key Underwriting Factors

Once a property passes the cash-flow test, underwriting takes over. That’s where the deal either moves forward or stalls out. DSCR is a big part of the picture, but it’s not the whole picture. Credit, reserves, property type, rent proof, and loan setup all play a part too. The point isn’t just to get a yes. It’s to keep enough cash flow and cash on hand to buy the next property.

Core Approval Standards to Expect

A 620 credit score is a common minimum, but 720 or higher often gets better pricing. That gap can change your monthly payment, which then changes your DSCR on every deal you do. Stronger credit and deeper reserves can also help you keep more cash free for your next purchase.

Down payments usually land at 20% to 25% of the purchase price, which puts LTV at 75% to 80%. Some programs go as low as 15% down for borrowers with strong credit and a solid DSCR, but that’s less common. For refinances, expect a maximum 75% LTV for cash-out.

Reserves often make or break approval. Lenders usually want 3 to 12 months of PITIA in liquid reserves per property. As your portfolio gets larger, some lenders switch to a global reserve rule. Retirement accounts may count, but lenders often use only 60% to 70% of the stated account value.

Property Type, Rent Documentation, and Loan Structure

Eligible property types usually include:

- Single-family rentals

- 2–4 unit residential properties

- Condos

- Townhomes

- Short-term rentals (STRs)

For rent proof, lenders usually rely on either a signed lease for occupied properties or a Fannie Mae Form 1007 market rent appraisal for vacant ones. If your lease is well above market comps, the lender may cut the income figure back to the appraiser’s estimate. That can be frustrating, but it happens.

Loan structure matters too. A 30-year fixed-rate loan gives you steady payments. An ARM, such as a 5/6 or 7/6 structure, usually starts 0.25% to 0.75% lower, which can help a tight deal clear the minimum DSCR. In some cases, underwriters use interest-only debt service instead of principal-and-interest, which can help a thinner deal qualify.

Underwriting Factors That Affect Scaling

These details matter because they shape how fast you can refinance, recycle equity, and pick up the next property.

Borrower experience is not always required, but a recorded track record as a landlord can lower reserve needs and help with LTVs on later deals. Entity ownership is also common. Most DSCR lenders require or strongly prefer closing in an LLC to support business-purpose lending and keep the loan separate from personal assets.

Most DSCR loans come with a prepayment penalty. The two structures you’ll see most often are:

- 3-2-1

- 5-4-3-2-1 step-down

These penalties can lower your rate, but they also affect your timing. If you want to refinance or pull equity out early, that penalty can get in the way. If early cash-out is part of your plan, a shorter penalty term may make more sense, even if the rate is a bit higher.

As portfolios grow, approvals tend to depend less on how many properties you own and more on your reserves, leverage, and the cash flow of each new deal.

Once you know the rules lenders use, the next move is setting up your first purchase so you can repeat the process with refinances and new buys.

Step by Step: Growing From One Rental to a Portfolio Using DSCR Loans

How to Prepare and Close Your First DSCR-Financed Rental

Once a property meets your DSCR target, the job is simple in theory: turn that first approval into a process you can use again and again.

Start with the basics in place - an LLC, solid credit, and documented reserves. Then go after deals that can do more than just close. They should also help support the next purchase. That usually means focusing on markets where rent-to-price ratios can support a DSCR of 1.20 or higher.

Run the numbers before you make an offer, not after. Check projected rent, expected expenses, and the DSCR. Then pick from various investor loan programs that keeps cash flow alive, order the appraisal, and move through underwriting.

One of the big draws here is speed. DSCR loans can close in as little as 15 to 21 days, which helps a lot when you're working on multiple deals and need approval tied to the property instead of your income paperwork.

After that first closing, the game changes. It stops being only about getting approved and starts being about putting your capital back to work.

How to Use Repeat Purchases and Cash-Out Refinances to Add Properties

The basic idea is pretty straightforward: cash flow keeps the property running, and equity helps fund the next deal.

A cash-out refinance can turn built-up equity into money for another down payment. At 75% LTV cash-out, every $100,000 in property appreciation can free up $75,000 in cash for the next purchase. That said, this only works if the new loan payment doesn't crush the deal. A good rule is to use cash-out refinances only when the property still lands at a DSCR of 1.0 or higher after the new payment.

A rate-and-term refinance can help too. Instead of pulling cash out, it can lower the monthly payment and improve DSCR without adding to the loan balance. That can leave more monthly income available for the next purchase.

The rhythm stays the same:

- Lease the property

- Build cash flow

- Refinance only if the DSCR still works

- Repeat

It sounds mechanical, and in a way it is. But that's the point. You want a buying system, not a one-off win.

How to Manage Risk as You Add More Properties

Growth falls apart fast when reserves are thin. If a vacancy hits or a repair bill lands at the worst time, you don't want to be pushed into a rushed sale or refinance. Keep enough liquidity on hand so one bad month doesn't turn into a chain reaction.

Diversification matters too. If too much of your portfolio sits in one market or depends on one tenant type, you're taking on a kind of risk that's tough to fix in a hurry. Spreading across different markets and mixing property types - like single-family homes, duplexes, and short-term rentals - helps keep DSCR-based growth on track, not just a little less risky.

As you move past a handful of units, day-to-day operations can start to drag on performance. At that stage, professional property management often becomes much more important.

"Managing two rental properties personally is manageable. Managing ten or twenty requires systems, software, and often professional property management." - FAAS Funding

Another point in favor of DSCR financing: each loan stands on its own. Unlike blanket loans, trouble with one property does not usually trigger default across the rest of the portfolio. That separation gives you room to deal with one problem property without putting everything else on the line.

With that setup, the next move is less about buying fast and more about managing for steady, long-term cash flow.

Conclusion: Build a Rental Portfolio Around Cash Flow, Leverage, and Timing

Once a deal passes DSCR screening and underwriting, the playbook gets a lot easier to repeat. When you know how the numbers work, DSCR can become a steady way to grow. Lenders look at the property's rent instead of your personal income, which means each loan can stand on its own.

Steady investors usually aim for 1.25+ DSCR, keep leverage around 75%–80% LTV, and use cash-out refinances at 75% LTV to help pay for the next purchase.

But refinancing isn't just about pulling out equity when you feel like it. Timing matters. The refinance has to line up with the loan's prepayment schedule, and you should only pull equity if the new loan still clears 1.0 DSCR.

The move from one rental to a full portfolio comes down to repeating the same disciplined process:

- Screen for cash flow

- Close with conservative leverage

- Build reserves

- Recycle equity on schedule

That's how property cash flow, not personal income, drives portfolio growth.

FAQs

Can I get a DSCR loan with no landlord experience?

Yes. You can qualify for a DSCR loan without prior landlord experience.

That’s because DSCR loans focus on the property’s income potential, not your job history or track record as a real estate investor. In most cases, lenders look at the property’s lease or market rent, your credit score, and your liquid reserves.

What expenses should I include before trusting a DSCR deal?

Start with the property’s full monthly PITIA: principal, interest, property taxes, insurance, and HOA or association fees. That’s the main number lenders use for DSCR.

For your own review, set aside 8% to 10% of gross monthly rent for maintenance and capital expenditures. Also check your liquidity and make sure you can cover any required reserves, which are often 3 to 6 months of PITIA per property.

When does a cash-out refinance make sense?

A cash-out refinance makes sense when you want to tap the equity in a rental property that has gone up in value or improved through renovations, then use that cash for down payments on new deals.

It tends to work best when the property has enough added value to support a cash-out refi - often up to 75% LTV - and any prepayment penalty window has already ended. That gives you a way to grow your portfolio without leaning on personal income or dipping into your own savings.