What Is a Debt Service Coverage Ratio and Why Does It Matter for Investors?

If a rental property can’t cover its loan payment, the deal can fall apart fast. That’s what DSCR measures: whether the property’s income is enough to pay its debt.

Here’s the short version:

- DSCR = property income ÷ debt payment

- Above 1.00 means the property brings in enough income

- Below 1.00 means the property falls short

- Many lenders want about 1.20 to 1.25

- A stronger DSCR can mean more borrowing power, lower rates, and a smaller down payment

- A weak DSCR can mean less leverage, higher rates, more reserves, or a loan denial

In plain terms, DSCR matters because lenders use it to decide:

- if I qualify

- how much I can borrow

- how much cash I need to bring in

- how much monthly room the property has

A simple example: if a property has $2,375 in monthly qualifying rent and $1,980 in monthly PITIA, the DSCR is 1.20x. That means the property brings in about 20% more than the debt payment.

There’s one thing many investors miss: the lender’s math is often tighter than mine. The underwriter may use the lower of lease rent or market rent, subtract 5% to 10% for vacancy, and count full PITIA instead of just principal and interest. That can turn a good-looking deal into a thin one.

What moves the number? Two things only:

- more net income

- less debt service

That’s why common fixes include:

- bringing rents to market before applying

- adding parking, pet rent, storage, or laundry income

- cutting owner-paid costs

- putting more money down

- using interest-only terms

- stretching amortization to 30 years

DSCR Loans for Beginners - Real Estate Investing Explained!

sbb-itb-e7c549b

Quick Comparison

| DSCR Level | What It Means | Common Loan Result |

|---|---|---|

| 1.25x+ | Strong cash flow cushion | Better pricing, more leverage |

| 1.00x–1.24x | Thin to fair cushion | Standard approval range |

| Below 1.00x | Property does not cover debt | Higher rates, lower LTV, or denial |

If I’m buying or refinancing a rental, DSCR loans are one of the first things I check because it tells me whether the property can stand on its own.

What DSCR Means in Real Estate Investing

DSCR measures whether a rental property's income covers its debt service. In plain English, it shows if the deal can pay for itself.

That matters because DSCR loans put the spotlight on the property, not the borrower's personal income. Lenders want to know one thing first: Does this rental bring in enough money to cover the loan?

Here’s the formula they use.

The DSCR Formula Every Investor Should Know

The formula is simple:

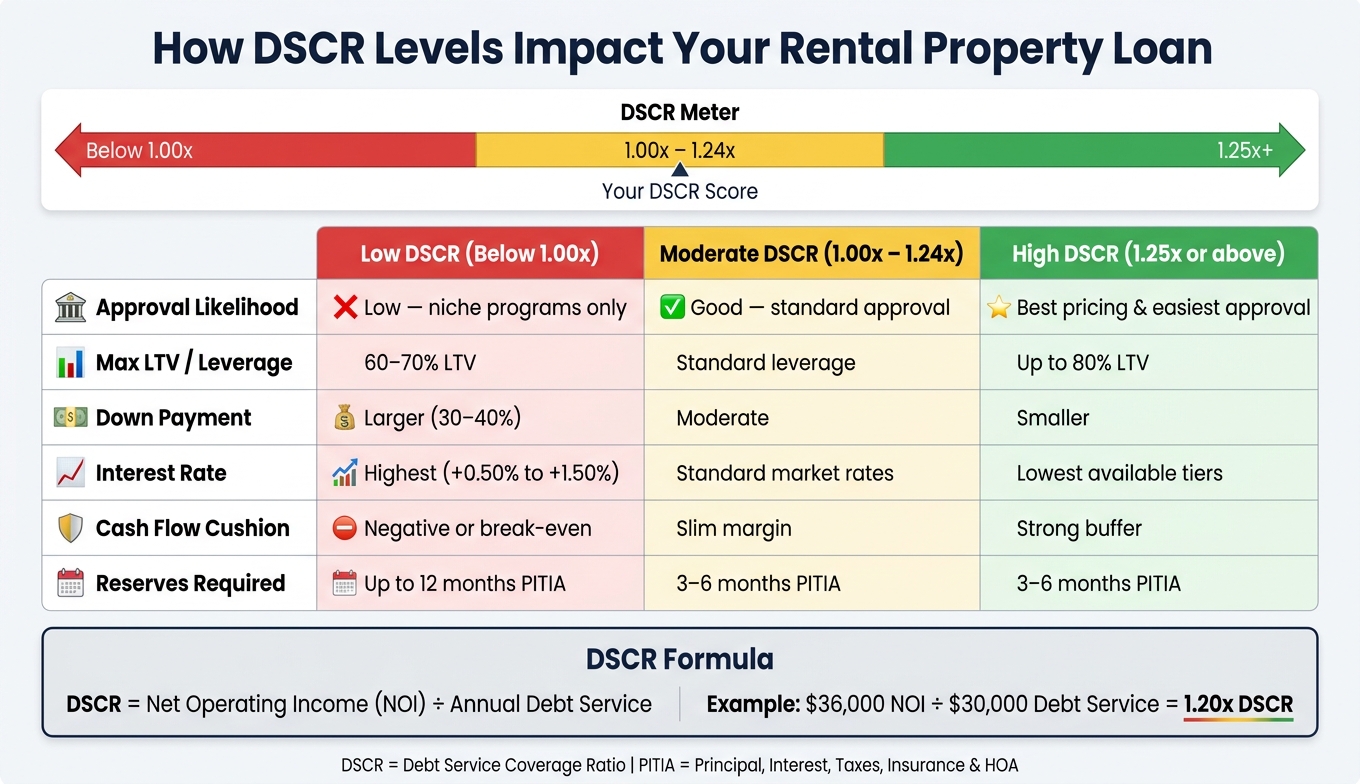

DSCR = Net Operating Income (NOI) ÷ Annual Debt Service

Say a rental property brings in $36,000 in NOI per year and its annual debt service totals $30,000, including any taxes, insurance, and HOA costs the lender includes. The DSCR would be 1.20x.

That means the property brings in 20% more than it needs to cover the debt. It's not a huge buffer, but it's above break-even.

What Counts as NOI and What Does Not

NOI is the income left after paying the property's operating costs. You start with gross rental income, then subtract expenses like:

- Property taxes

- Insurance premiums

- Repairs and maintenance

- Property management fees

- HOA dues

- Owner-paid utilities

NOI does not include debt service, depreciation, or personal taxes.

How to Read Strong, Marginal, and Weak DSCR Numbers

A 1.00x DSCR means the property breaks even. Above 1.00x means there's surplus income. Below 1.00x means the investor has to cover the gap out of pocket.

| DSCR Range | What It Means | Loan Impact |

|---|---|---|

| 1.25x or higher | 25%+ surplus | Lowest rates; up to 80% LTV |

| 1.00x – 1.24x | Slim to moderate surplus | Standard rates; qualifies for most programs |

| 0.75x – 0.99x | Monthly shortfall | Higher rates; reduced leverage (60–70% LTV) |

| Below 0.75x | Significant shortfall | Specialty lenders only; 35–40% down payment |

A higher ratio gives lenders more room for vacancy, repairs, and tax increases. Next, see how lenders calculate DSCR on an actual rental property.

How Lenders Calculate DSCR for Rental Property Loans

Lenders usually use tighter math than investors do. So even if your back-of-the-napkin estimate looks fine, the underwritten DSCR often comes in lower. The gap usually starts with rent, vacancy, and debt service.

A Step-by-Step DSCR Calculation Using a U.S. Rental Property

Here’s what lender underwriting might look like for a single-family rental:

- Gross monthly rent: $2,500 (the lower of the lease or the appraiser's Form 1007 market rent)

- Vacancy deduction (5%): −$125

- Qualifying monthly income: $2,375

- Monthly PITIA (principal, interest, taxes, insurance, and HOA dues): $1,980

- DSCR: $2,375 ÷ $1,980 = 1.20x

That’s the figure the lender uses to decide if the property can carry the debt. A 1.20x DSCR may be enough to qualify, but better pricing often shows up at higher ratios. And this number may still move once the lender finishes its tax, insurance, and rent checks.

Why the Lender's DSCR May Come Out Lower Than Yours

Lender underwriting tends to come in lower because the assumptions are stricter. Rent may be cut back, vacancy is usually added, and taxes, insurance, and debt service are often higher than an investor’s early estimate.

| Input | Investor Estimate | Typical Lender Underwriting |

|---|---|---|

| Monthly Rent | Current lease or high-end market estimate | Lower of lease or Form 1007 market rent |

| Vacancy | Often 0% (assumes full occupancy) | 5% to 10% market-standard deduction |

| Property Taxes | Seller's current tax bill | Reassessed value based on purchase price |

| Insurance | General estimate or placeholder | Actual bound quote, including flood/wind |

| PITIA | Principal and interest (P&I) only | Full PITIA - includes principal, interest, taxes, insurance, and HOA |

Two issues trip people up all the time: property tax reassessment and insurance. In states like Texas, taxes can jump hard after a sale. And in coastal or flood-prone markets, the actual insurance premium may land far above a rough estimate. Lenders want a bound quote, not a guess, before they lock in underwriting.

How DSCR Applies to Purchases, Rate-and-Term Refinances, and Cash-Out Refinances

DSCR affects more than just approval. It also helps determine how much you can borrow and which loan setup makes sense for the property's cash flow.

| Loan Purpose | Typical Max LTV | Relative Rate | Primary Underwriting Focus |

|---|---|---|---|

| Purchase | 80%–85% | Lowest | Highest leverage when rent supports the new payment |

| Rate-and-Term Refi | 75%–80% | Moderate | Best when the property is already stabilized |

| Cash-Out Refi | 70%–75% | Highest | Tightest DSCR tolerance because leverage is already being increased |

If the property's DSCR is tight, the lender may cut the LTV to 65% or 70% to get the deal within range. Once the lender has the ratio, it uses that number to shape approval, leverage, and pricing.

Why DSCR Affects Approval, Borrowing Power, and Cash Flow

DSCR Levels Explained: How Your Ratio Affects Loan Approval & Terms

DSCR shapes approval, loan size, and pricing. Once a lender has that ratio, it uses it to judge how much risk the loan can handle. For investors, that means one number can change approval odds, borrowing power, and monthly cash flow all at once.

How DSCR Affects Loan Approval and Maximum Loan Amount

If DSCR is too low, lenders usually cut leverage, ask for a bigger down payment, or do both. On the flip side, a stronger DSCR can support a larger loan and less cash due at closing.

In many cases, lenders look for a DSCR of around 1.20x to 1.25x for standard approval.

DSCR also has a direct effect on your interest rate. Ratios at 1.25x or higher often open the door to the best pricing tiers. If the DSCR falls below 1.00x, pricing can increase by 0.50% to 1.50%.

How DSCR Loans Work for Self-Employed and 1099 Borrowers

DSCR loans are non-QM mortgages. That means lenders focus on the property's cash flow instead of W-2s, pay stubs, tax returns, or personal DTI.

Put simply, the loan is based on how the property performs. That's a big deal for self-employed and 1099 borrowers whose tax returns may not show what they can actually afford.

DSCR loans can also be easier to grow with than conventional loans because many programs don't follow the same property-count caps.

Strong vs. Weak DSCR: What Each Scenario Means for Investors

The table below shows how the same property, with different income levels, can lead to very different financing results.

| Low DSCR (below 1.00x) | Moderate DSCR (1.00x–1.24x) | High DSCR (1.25x or above) | |

|---|---|---|---|

| Approval Likelihood | Low; often limited to niche programs | Good; standard approval | Best pricing and easiest approval |

| Typical Leverage | Lower leverage | Standard leverage | Highest leverage |

| Down Payment | Larger down payment | Moderate down payment | Smaller down payment |

| Interest Rate | Highest; premium pricing | Standard market rates | Lowest available tiers |

| Cash Flow Cushion | Negative or break-even | Slim margin | Strong buffer |

A weak DSCR makes the loan harder to place and the property tougher to carry. A strong DSCR gives the deal more room to handle vacancies, repairs, and payment changes.

Think of it like driving with almost no gas in the tank. A low DSCR leaves very little room for vacancy or repair costs. A high DSCR gives the loan more breathing room.

Lenders often want 3 to 6 months of PITIA in liquid reserves on standard deals. If DSCR is below 1.00x, they may ask for up to 12 months.

That gap is exactly why many investors try to improve income, lower costs, or change the deal structure before they apply.

How to Improve DSCR Before You Apply or Refinance

A weak DSCR isn't always a dead end. In many cases, you can fix it before closing.

If the lender's DSCR comes in low, there are only two ways to improve it: increase NOI or cut debt service. That's the whole game.

Ways to Increase Property Income Before Applying

Start with rent.

If the lease allows it, raise rent to market before underwriting. For long-term rentals, lenders usually use the lower of:

- your signed lease amount

- the appraiser's market rent estimate on Form 1007

That means actual rent bumps carry more weight than pro forma projections.

You can also add income outside of base rent. Things like pet rent, reserved parking, on-site storage, and laundry fees can all count toward gross income. On short-term rentals, many lenders use AirDNA-based projections but apply a 20% expense factor to those numbers.

One more detail that gets missed: underwrite taxes at the purchase price, not the seller's current tax bill.

Start with income first. Then look at expenses and loan terms.

How to Lower Operating Costs and Structure the Loan More Efficiently

On the expense side, small changes can help.

If you shift utility costs to tenants, or use a ratio utility billing system (RUBS) on small multifamily properties, you reduce owner-paid operating costs and improve NOI. Insurance is another area worth checking. Shop it every year, especially in high-cost states, and get a bound quote before you submit the file.

Loan structure is often the fastest lever.

A bigger down payment cuts the loan balance, which lowers monthly debt service. For example, moving from 80% to 75% LTV can push a borderline DSCR from 1.10x to 1.25x. An interest-only period removes principal from the qualifying payment during the IO window, which can improve the ratio in a big way. Extending amortization from 25 years to 30 years also lowers the monthly payment.

Choosing a Loan Structure That Fits the Property's Cash Flow

If you can't do much on the income side, shape the loan around the property's cash flow so the qualifying payment comes down.

The table below shows the most common moves and how they affect the ratio:

| Strategy | Effect on NOI | Effect on Debt Service | Typical Impact on DSCR |

|---|---|---|---|

| Raise Rents to Market | Increases | None | High improvement |

| Add Ancillary Income | Increases | None | Moderate improvement |

| Increase Down Payment | None | Decreases | High improvement |

| Interest-Only Period | None | Decreases | Very high improvement |

| Extend Amortization (30 yr) | None | Decreases | Moderate improvement |

| Lower Insurance | None | Lowers the qualifying payment | Low to moderate |

| 5/1 or 7/1 Adjustable-Rate Mortgage | None | Decreases (initial period) | Moderate improvement |

Sometimes one move won't get you there. In that case, combine two. A common example is raising rents to market and putting more money down. Two modest adjustments can be enough to move a borderline file into the approval range.

FAQs

What is a good DSCR for a rental property?

A good DSCR for a rental property is usually 1.25 or higher. In plain English, that means the property brings in 25% more income than it needs to cover its debt payments. For many lenders, that level often lines up with better loan terms.

A DSCR of 1.0 means the property is just breaking even. There's no room to breathe. If rent drops for a month or an expense pops up out of nowhere, things can get tight fast.

That's why many investors aim for 1.20 to 1.50. A higher ratio gives you a bit of cushion for vacancies, repairs, or other surprise costs.

Does vacancy count against DSCR?

It depends on the property type and how the lender underwrites the deal.

For commercial properties, lenders usually look at net operating income (NOI). That figure already includes a vacancy allowance, so the lender is building some empty-unit risk into the numbers from the start.

For residential properties, many lenders use a simpler formula: gross rent divided by PITIA. That said, not every lender handles it the same way. Some may still apply a vacancy adjustment or use a rental income factor before they run the numbers.

Can I qualify for a DSCR loan with a ratio below 1.00?

Yes, but your options may be more limited.

Many lenders want a DSCR of at least 1.00. That said, some specialty programs may go as low as 0.75.

A DSCR below 1.00 usually means you'll need stronger compensating factors, such as:

- A larger down payment

- Higher credit scores

- More cash reserves

These loans may also come with higher rates or premiums.