DSCR Loan Down Payment Requirements: How Much Do You Really Need?

Most DSCR buyers should plan for more than the headline minimum. In many cases, that means 25% to 35% down, not just 20%. And once I add closing costs plus cash reserves, total cash needed often lands around 27% to 33% of the purchase price.

If I were sizing up a deal fast, here’s what I’d watch first:

- 20% down is often the floor for a strong file

- 25% down is a common middle ground

- 30% to 35% down can show up with lower credit, thin cash flow, or tougher property types

- Short-term rentals, mixed-use, and 5+ unit deals often need more cash up front

- Reserves matter: many lenders want 6 months of PITIA, and some STR deals need 12 months

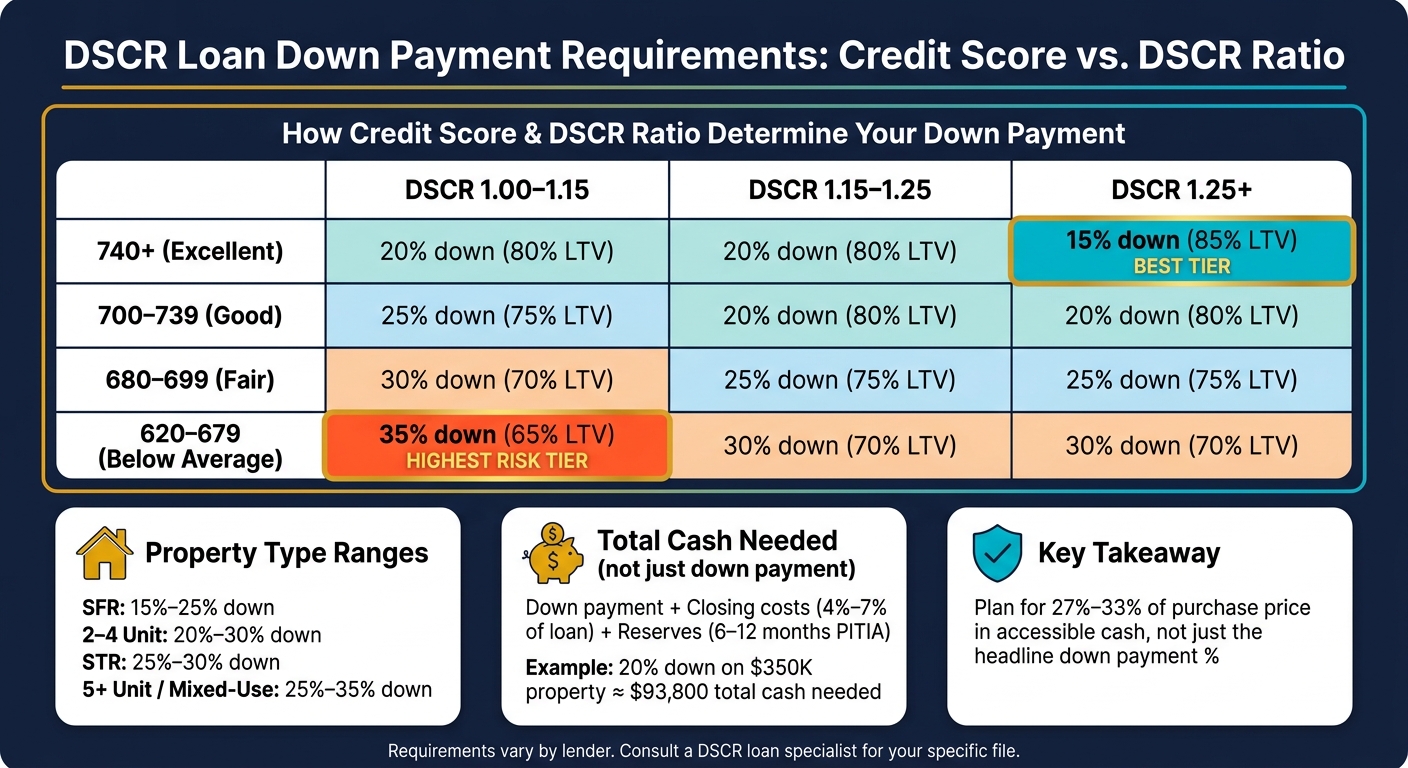

On a $350,000 rental, total cash needed can reach about $93,800 once I factor in the down payment, closing costs, and reserves. So the question is not just “What is the down payment?” It’s “What is my full cash-to-close number?”

Here’s the short version:

| Item | What to expect |

|---|---|

| Minimum down payment | Often 20% |

| Common range | 25%–35% |

| Strong SFR file | Sometimes 15%–20% |

| STR / mixed-use / 5+ units | Often 25%–35% |

| Total cash needed | Often above the down payment by a lot |

I’d treat the down payment as only one part of the deal. The full number is down payment + closing costs + reserves.

DSCR Loan: How Much Do I Need for a Down Payment?

sbb-itb-e7c549b

How DSCR loans work and why down payment matters

DSCR stands for Debt Service Coverage Ratio. Put simply, it measures whether the property's rent covers the monthly debt payment. The formula is gross rent divided by monthly PITIA. PITIA includes principal, interest, taxes, insurance, and any HOA dues.

With a DSCR loan, the property does the heavy lifting. Approval is based on rental income, not your W-2s or tax returns. That's a big reason these loans appeal to self-employed investors and buyers who take large tax write-offs.

What DSCR means for rental property qualification

A DSCR of 1.00 means the rent exactly matches the debt payment. A 1.25 means the property brings in 25% more income than the monthly payment. To run that math, lenders use the lower of the signed lease or the appraiser's market rent estimate.

If rent only barely covers the payment, the deal looks thinner on paper. In that case, a lower DSCR often leads to a bigger down payment requirement, often 25% to 30%.

Why a larger down payment can improve approval odds

A larger down payment reduces the loan amount. That lowers the monthly PITIA payment and improves the DSCR ratio right away. So a deal that looks shaky at 80% LTV can move into a better approval tier at 70% LTV.

There's also a pricing angle. Moving from 75% LTV to 70% LTV can reduce the rate by 25 to 50 basis points.

That's why lenders often shift from 20% down to 25% or even 30% depending on the numbers in the deal.

DSCR loan down payment ranges investors should expect

Most investor loan programs land at 80%, 75%, or 70% LTV. Put plainly, that usually means a down payment of 20%, 25%, or 30%. In practice, lenders tend to group deals into these standard leverage tiers.

20%, 25%, and 30% down: what each scenario looks like

Here’s how those down payment ranges look on a $300,000 property:

| Down Payment | LTV | Down Payment on $300K |

|---|---|---|

| 20% | 80% | $60,000 |

| 25% | 75% | $75,000 |

| 30% | 70% | $90,000 |

The 25% down (75% LTV) tier is often the sweet spot. That’s where investors can usually get more competitive interest rates and more flexible terms.

Putting more money down also reduces monthly debt service. That can improve the property’s DSCR ratio and give the deal a bit more room if vacancies show up. In some cases, moving from 75% LTV to 70% LTV can waive interest reserve escrow, which may cut cash needed at closing.

A 30% down requirement often shows up when the file has weaker credit, lower DSCR, or a more complicated property.

How property type affects the minimum down payment

Property type can shift a deal out of the standard range fast.

A standard single-family rental (SFR) can sometimes qualify with as little as 15% down, though 20% down is the more common starting point for a strong file. Most 2–4 unit multifamily properties start around 20% to 30% down. Short-term rentals (STRs) usually come in closer to 25% to 30% down because lenders may count only 75% to 90% of projected gross revenue in DSCR calculations. And 5+ unit, commercial, and mixed-use properties often need 25% to 35% down.

| Property Type | Typical Down Payment |

|---|---|

| Single-Family Rental (SFR) | 15%–25% |

| 2–4 Unit Multifamily | 20%–30% |

| Short-Term Rental (STR) | 25%–30% |

| 5+ Unit / Commercial | 25%–35% |

| Mixed-Use | 25%–35% |

Simple properties with strong income usually land near the low end of the range. More complicated deals tend to need more equity upfront.

What can push your required down payment higher

DSCR Loan Down Payment by Credit Score & DSCR Ratio

If 20% to 30% is the starting point, plenty of things can push the number up. In most cases, the minimum you see in a loan program isn't the number you should expect in real life. Lenders look at the whole file, not just one data point. When a deal stacks up multiple risk factors, the down payment usually goes up with it.

Your required down payment usually comes down to four things: credit score, DSCR, transaction type, and property type.

Credit score, DSCR, and investor experience

In practice, the lowest down payment options usually go to borrowers with a 720+ FICO score and a DSCR of 1.25 or higher. Once either one slips, the cash requirement tends to climb.

| Credit Score | DSCR 1.00–1.15 | DSCR 1.15–1.25 | DSCR 1.25+ |

|---|---|---|---|

| 740+ | 20% down (80% LTV) | 20% down (80% LTV) | 15% down (85% LTV) |

| 700–739 | 25% down (75% LTV) | 20% down (80% LTV) | 20% down (80% LTV) |

| 680–699 | 30% down (70% LTV) | 25% down (75% LTV) | 25% down (75% LTV) |

| 620–679 | 35% down (65% LTV) | 30% down (70% LTV) | 30% down (70% LTV) |

A simple way to read that table: stronger credit and stronger cash flow buy you more leverage. Weaker credit or a thinner DSCR mean the lender wants more money in the deal upfront.

Investor experience matters too. First-time investors often face higher minimum down payments than repeat landlords. That's not unusual. From a lender's point of view, someone who's already managed rental property is less of an unknown.

Purchase scenario, reserves, and occupancy strategy

The loan setup itself can also push your cash-to-close higher. One big factor is loan purpose. A purchase transaction may allow up to 80% to 85% LTV for a qualified borrower. But a cash-out refinance is usually capped at 70% to 75% LTV, even if the property has strong cash flow. That's just how the program is built.

Occupancy strategy can change the math too. Short-term rentals often come with tighter reserve rules. It's common to see 12 months of PITIA reserves required, along with a 10% to 25% haircut to projected income. So even if the headline down payment looks workable, the total cash needed can jump fast.

Here's where borrowers get tripped up: a deal can look fine on the surface, then land in a higher down payment bucket once all the parts are priced together. For example, even when 20% down is technically on the table, a borrower in the 700–739 credit range with a borderline DSCR and a short-term rental plan is more likely to end up at 25% to 30% down. That’s why two deals that seem similar can lead to very different cash requirements at closing.

How to estimate the total cash you need before applying

Most investors come up short here. They budget for the down payment, then get hit by closing costs and reserve rules. Once you have a rough LTV range, turn that into a cash-to-close estimate that includes the down payment, closing costs, prepaid items, and verified liquid reserves.

Step 1: Estimate price, rent, and likely LTV band

Start with three numbers: purchase price, estimated monthly rent, and your FICO score. Those inputs give you a solid first pass at your likely leverage tier before you talk to a lender.

In plain English: better DSCR and stronger credit usually lead to more leverage. Weaker files often land in the 25% to 35% down range. Even a small bump in your FICO score can help push you into a better leverage tier.

Step 2: Add closing costs, reserves, and monthly payment differences

Once you know your likely LTV band, add the costs that often get overlooked.

Closing costs usually land around 4% to 7% of the loan amount all-in. A rough breakdown often looks like this:

- Origination fees: about 1.0% to 1.5% of the loan amount

- Broker fees: about 0.75% to 1.0%

- Underwriting and processing: about $1,350 to $1,600

- Appraisal: about $400 to $600 for a single-family home

- Title insurance and impounds

You should also plan for reserves. For long-term rentals, expect 6 months of reserves. For short-term rentals, expect 12 months. The money usually stays in your account, but the lender still needs to verify that it’s there.

Here’s how leverage changes the cash you need up front on a $400,000 purchase:

| Down Payment | Loan Amount | Monthly Payment | DSCR Effect | Est. Total Cash Needed |

|---|---|---|---|---|

| 20% ($80,000) | $320,000 | Highest | Lowest ratio | ~$115,000–$125,000 |

| 25% ($100,000) | $300,000 | Moderate | Improved ratio | ~$130,000–$140,000 |

| 30% ($120,000) | $280,000 | Lowest | Highest ratio | ~$145,000–$155,000 |

Total cash includes down payment, estimated closing costs, and 6 months of PITIA reserves.

A 20% down deal often means you need about 27% to 33% of the purchase price in accessible cash. That’s the number to plan around, not just the headline down payment percentage.

Conclusion: Plan for more than the minimum

After looking at leverage tiers and approval factors, the takeaway is pretty simple: the advertised minimum usually isn't the amount of cash you’ll need at closing. Minimum down payments can look low on paper, but the cash needed to get a deal across the finish line is often higher. Your down payment can move up or down based on your credit profile, DSCR, and property type.

And that’s only one piece of the puzzle. Closing costs and reserve requirements can add a meaningful amount on top of the down payment, which can change the math fast.

Before you submit an offer, run the full cash-to-close number:

- Down payment

- Closing costs

- Reserve requirements

That’s the number that matters. If the total pushes your budget too far, lower the offer price or hold off until you find a deal that fits your numbers better.

FAQs

How do I estimate my full cash to close?

To estimate your full cash to close for a DSCR loan, look beyond the down payment. That piece is often 20% to 25% of the purchase price, but it’s not the whole picture.

You’ll want to add:

- the down payment based on your loan-to-value ratio

- closing costs, such as origination points, appraisal, title, escrow, and prepaid items

- cash reserves, which are often 3 to 6 months of PITIA

Miss those extra costs, and you could come up short during underwriting.

What raises my DSCR loan down payment?

Your DSCR loan down payment can go up based on your credit score, DSCR, property type, and the loan setup.

In many cases, lenders ask for more down if your credit score is below 720. That pressure tends to get stronger below 680. The same goes for your DSCR. If it falls below 1.0, expect a higher down payment in many loan files.

Property type matters too. A lender may ask for more down on:

- Multi-unit properties

- Short-term rentals

- Non-warrantable condos

- Commercial properties

- Cash-out refinances

Some lenders also set a hard floor of 25% down, no matter how strong the rest of your file looks.

Can I get a DSCR loan with less than 20% down?

Yes. Some lenders offer DSCR loans with as little as 15% down, but that isn't the norm. In most cases, borrowers need a strong profile to qualify.

That often means meeting tighter standards, such as a 720+ credit score and a 1.25+ DSCR. And there’s usually a trade-off: these lower-down-payment loans often come with higher interest rates than loans that require 20% or 25% down.