DSCR Loan Rates in 2026: What Real Estate Investors Should Expect

If I had to sum it up in one line: most DSCR borrowers in 2026 are seeing rates from about 6.50% to 8.75%, and small changes in credit, LTV, DSCR, or prepay terms can move a quote by 0.50% to 1.50% or more.

If you’re buying or refinancing a rental this year, here’s the short version:

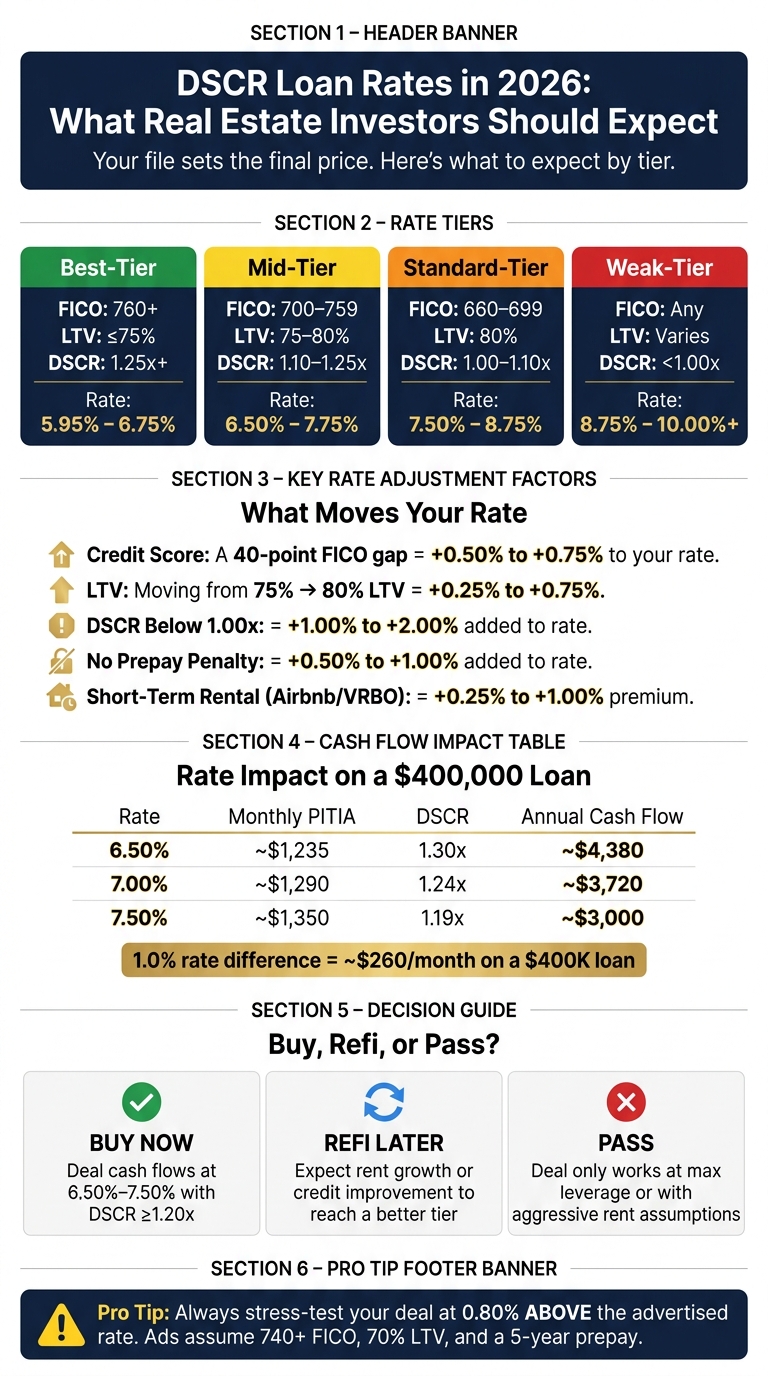

- Best-tier files are landing around 5.95% to 6.75%

- Mid-tier files are often around 6.50% to 7.75%

- Standard files are often around 7.50% to 8.75%

- Weaker files can run 8.75% to 9.50%+

- A move from 75% to 80% LTV can add 0.25% to 0.75%

- A DSCR below 1.00x can add 1.00% to 2.00%

- Choosing no prepayment penalty can cost 0.50% to 1.00% more in rate

- On a $400,000 loan, a 1.00% rate gap can change payment by about $260 per month

What does that mean for you? The market sets the starting point, but your file sets the final price. In 2026, Treasury yields, non-QM demand, credit score, leverage, property type, reserves, and prepay terms all play a part.

I’d look at this article as a simple decision guide:

- Buy now if the deal still cash flows at today’s rate

- Refinance later if rent growth or a stronger file could get you into a lower pricing tier

- Pass if the deal only works with thin margins, max leverage, or rent assumptions that feel too aggressive

The main point is simple: don’t focus only on the headline rate. I’d run the deal with a rate that’s about 0.80% above the ad, then check cash flow, DSCR, and exit timing before moving ahead.

DSCR Loan Rates by Borrower Tier in 2026

What Is Pushing DSCR Rates Up or Down in 2026

Market Forces Behind Daily and Weekly Rate Changes

The market sets the baseline. But it does not set the final quote.

In 2026, DSCR quotes move with Treasury yields, not the Fed alone. Most DSCR lenders price off the 5-year or 10-year U.S. Treasury yield. So when those yields climb, DSCR quotes usually climb too, often within 30 to 60 days. That benchmark is the starting line, not the finish line.

Inflation data is one of the fastest triggers. The April 2026 CPI print showed a +3.8% year-over-year headline increase. That pushed the 10-year Treasury to a one-year high of about 4.60% in mid-May 2026. When that happens, investor quotes can change fast, even if the property stayed the same and the borrower’s credit profile didn’t move an inch.

There’s another piece here: DSCR loans are funded through private capital and securitization. So investor demand has a direct effect on pricing. Strong demand tends to narrow spreads. Weak demand tends to widen them. Non-QM issuance is projected to reach $75.25 billion in 2026, up 12% from 2025, with DSCR loans making up nearly 50% of all non-QM securitizations. That’s why quotes can reprice before lock.

Once the market sets the base rate, the final quote comes down to the borrower and the property. In 2026, that borrower-level pricing matters more. Next up are the factors that push your rate above the baseline: credit score, leverage, DSCR ratio, and property type.

sbb-itb-e7c549b

Borrower and Property Factors That Change Your DSCR Rate

Lenders don’t stop at the market base rate. After Treasury yields and investor demand set the starting point, they add pricing adjustments based on you and the property. Those adjustments stack on top of each other. So if a few inputs work against you, your quote can end up well above the baseline.

Credit Score, LTV, and DSCR Ratio

Credit score, LTV, and DSCR do most of the heavy lifting on pricing.

Credit score is the biggest driver. A 40-point gap can move your rate by 0.50% to 0.75%. DSCR lenders often price in 20-point FICO bands, which means a borrower at 760+ is in a very different pricing bucket than someone in the high 600s.

LTV is another big swing factor. Moving from 75% to 80% LTV often leads to a rate bump of 0.25% to 0.75%. That jump can make or break deal cash flow. For many investors, staying at or under 75% LTV is one of the cleanest ways to keep the rate in check.

DSCR ratio works in two ways: it helps determine whether you qualify, and it tells the lender how much pricing cushion to build in. A 1.25x or higher DSCR will usually get you the best pricing available. Drop below 1.00x, and rates can climb 1% to 2%. On the same property, the gap between a 1.0x and 1.25x DSCR can be as much as 0.50% to 0.75% off your rate.

| Borrower Tier | FICO | LTV | DSCR | Typical Rate Range |

|---|---|---|---|---|

| Top-Tier | 760+ | ≤75% | 1.25+ | 5.95% – 6.75% |

| Mid-Tier | 700–759 | 75–80% | 1.10–1.25 | 6.50% – 7.75% |

| Lower-Tier | 660–699 | 80% | 1.00–1.10 | 7.50% – 8.75% |

| Sub-1.0 DSCR | Any | Varies | <1.00 | 8.50% – 10.00%+ |

Property Type, Reserves, and Prepayment Penalties

The property can change pricing too.

Single-family rentals usually get the best rates. If you move into 2–4 unit properties or condos, lenders often add 0.125% to 0.50% to the rate. Short-term rentals like Airbnb and VRBO tend to cost more, with a premium of 0.25% to 1.00%, because lenders discount projected income and use tighter vacancy assumptions. As of mid-2026, about 25% of funded DSCR loans are tied to short-term rental properties.

Reserves also matter for pricing and approval. Most institutional DSCR programs in 2026 want at least 6 months of PITIA - Principal, Interest, Taxes, Insurance, and Association dues - in liquid reserves. Having more reserves usually won’t lower your rate, but weak reserves can trigger lender overlays or slow down approval.

Prepayment penalties are where a lot of borrowers either save money up front or get hit later. A standard 5-year step-down (5-4-3-2-1) will usually get you the lowest headline rate. Choose no prepayment penalty, and the rate often goes up by 0.50% to 1.00%. That extra cost matters. But it can still make sense if you expect to refinance or sell in the next few years.

The smart move is to line up the penalty with your hold period. Buy-and-hold investors planning to keep the property for 5+ years will often want the 5-year penalty to get the lower rate. Investors using a BRRRR plan, or anyone expecting to sell within two to three years, should run the numbers before taking the lower quote at face value. A 5% penalty on a $375,000 loan is $18,750 in year one.

Those pricing gaps hit your monthly debt service first. After that, they flow straight into your purchase math and refinance math.

How 2026 DSCR Rates Affect Purchases, Refinances, and Cash Flow

Once credit, LTV, and property type shape your quote, the next step is simple: run the payment math before you commit. Even a modest rate change shows up fast in monthly debt service and cash flow. On a $500,000 purchase with 25% down and a $375,000 loan, the jump from 6.50% to 7.875% can take a deal from workable to thin.

Purchase Scenarios: When a Higher Rate Still Works

The key question is whether the property still covers its debt service and leaves enough room to make the deal worth your cash.

Take a $500,000 single-family rental with 25% down, which means a $375,000 loan, and $3,650 in monthly rent. At 6.50%, monthly principal and interest is about $2,370, and total PITIA comes in around $3,075. That leaves a 1.19x DSCR and about $575 in monthly cash flow. At 7.875%, P&I climbs to $2,718, PITIA reaches $3,423, and DSCR slips to 1.07x. Cash flow drops to just $227 per month. At 6.50%, the deal works. At 7.875%, there's not much room for error.

That doesn't always mean you should walk away. You may be able to get the numbers back in line by bringing in more cash to lower LTV, negotiating a lower purchase price, or using tighter rent assumptions. A higher rate can still pencil out, but the property has to carry the weight.

The same spread matters on a refinance too, but cash-out deals usually give you less room to work with.

Refinance Scenarios: Rate-and-Term vs. Cash-Out

In 2026, rate-and-term refinances tend to price close to purchases. Cash-out refinances usually cost 0.25% to 0.50% more, and lenders also keep leverage tighter. In most cases, that means 70%–75% max LTV on cash-out versus 80% on purchases.

| Refinance Type | Rate Range (June 2026) | Typical LTV Cap |

|---|---|---|

| Rate-and-Term (Best Tier) | 5.95% – 6.75% | 75% – 80% |

| Cash-Out (760+ FICO) | 6.45% – 7.25% | 70% – 75% |

| Cash-Out (Mid-Tier) | 7.25% – 8.50% | 70% |

| Cash-Out (Lower Tier) | 8.75% – 9.75% | 65% – 70% |

A cash-out refi makes sense only if the money you pull out can earn more than the added interest cost. Yes, it cuts monthly cash flow on the current property. But it also gives you capital to grow. A rate-and-term refi makes sense when you can lower your rate by at least 0.75% or move from a thinner DSCR tier into a stronger one, which may also help you get a better rate. And before you move ahead with either option, check for a prepayment penalty. The lowest-rate setups often come with one.

What a 0.50% to 1.00% Rate Difference Does to Deal Viability

A small shift in rate can change the whole picture. On a $400,000 loan, a 1.0% rate difference - for example, 6.50% versus 7.50% - changes the monthly payment by about $260. That's $3,120 per year.

On a $200,000 property bringing in $1,600 per month in rent, a 0.50% rate drop from 7.50% to 7.00% adds about $720 in annual cash flow and improves DSCR from 1.19x to 1.24x. That half-point move may not sound huge at first. But to a lender, it can be the line between a marginal file and a healthy one.

| Interest Rate | Monthly PITIA | DSCR (at $1,600 Rent) | Annual Cash Flow |

|---|---|---|---|

| 7.50% | $1,350 | 1.19x | $3,000 |

| 7.00% | $1,290 | 1.24x | $3,720 |

| 6.50% | $1,235 | 1.30x | $4,380 |

Run each deal at least 80 basis points above the advertised rate. That's the safer way to look at it. Advertised rates often assume 740+ FICO, 70% LTV, and a 5-year prepay setup. Miss any one of those inputs, and you should expect a higher rate and less cash flow than the early numbers suggest.

How to Improve Your DSCR Pricing and Make a Better Decision

Steps to Strengthen Your File Before You Apply

Once you see how rate changes hit your cash flow, the next move is simple: work on the parts you can still change.

The best pricing gains usually happen before you submit the loan file. In most cases, five things matter most: credit score, leverage, reserves, property type, and prepayment structure.

Credit score is often the fastest place to make progress. DSCR lenders usually price loans in 20- to 40-point FICO bands, with common pricing breaks at 680, 700, 720, and 740. If you pay revolving balances down below 30% utilization, your score may move up within 30–60 days. And that can matter a lot: the gap between a 680 and a 740 FICO can mean a rate difference of 0.50% to 1.50% on the same deal.

Leverage comes next. Moving from 80% to 75% LTV is usually a big pricing break. Getting to 70% LTV or less will often open the door to the lowest base rates on the menu. If a deal feels tight at 80% LTV, putting more money down will usually do more for pricing than shopping the same file all over town.

After that, reserves and property type still play a big role. Showing 6–12 months of PITIA in liquid reserves can help you avoid pricing add-ons. As for the asset itself, single-family rentals usually get the best pricing. Short-term rentals and smaller multifamily properties usually cost more.

The fifth lever is prepayment structure. If you accept a 5-year step-down penalty instead of a shorter step-down or a no-prepay option, your note rate may drop by 0.50% to 1.00%. That sounds good on paper, but it only works if your timeline fits the penalty. If your plan is to renovate, push rents, and refinance in two to three years, a no-prepay option or a shorter step-down is often the smarter move, even with a higher rate.

How to Decide Whether to Buy Now, Refinance Later, or Pass

Use the rate math to pick the right path, not just the cheapest quote.

Buy now if the property still cash flows at today’s rates - usually 6.50%–7.50% for standard files - and the DSCR lands at 1.20x–1.25x or better at 75%–80% LTV. Waiting for rates to fall can feel safe, but a good deal doesn’t always wait.

Refinance later can make sense for value-add deals. Maybe you expect rents to go up. Maybe you think you can move into a better credit tier. Maybe both. In that case, it can be worth choosing a no-prepay option or a 1- to 3-year step-down now, even if the rate is 0.50%–1.00% higher.

Here’s the plain-English version:

- Buy now if the deal cash flows at today’s rate.

- Refinance later if rent growth or better credit can move you into a stronger tier.

- Pass if the deal only works at max leverage or with optimistic rent.

That last point matters more than people like to admit. If the numbers only work when everything goes right, the deal is probably too thin to force.

FAQs

How do I know if a DSCR deal still works at today’s rates?

Model your actual deal, not the flashy starting rate in an ad. A more honest range is 6.50% to 9.25%, based on your profile, so underwrite with a conservative lens.

Stress-test the cash flow using the factors lenders will look at: your credit score, LTV, property type, DSCR, and any prepayment penalty. If the numbers only work at the very lowest rate, the deal is probably too thin.

A 1.25+ DSCR can help you get better pricing. On the flip side, choosing a no-penalty option may push the rate up by 0.5% to 1.0%.

What can I improve before applying to get a lower DSCR rate?

Before you apply, work on the risk factors lenders care about most.

Start with your DSCR ratio. Try to get it to 1.25 or higher. You can do that by lowering the purchase price, increasing rents, or putting more money down so your debt service drops.

It also helps to improve your credit score and keep LTV under 75% if you can. You may also get better pricing if you accept a 5-year prepayment penalty.

If you plan to hold the property for 4 to 6 years, buying down the rate with discount points can make sense.

Should I choose a lower rate or no prepayment penalty?

It depends on your investment horizon and exit strategy.

A standard 5-year step-down (5-4-3-2-1) usually comes with a lower rate, which can help long-term hold investors get more out of their monthly cash flow. If you choose no prepayment penalty or a shorter term, the rate often goes up by about 1.00%. That trade-off can make sense for flippers or BRRRR investors who want more room to sell or refinance without getting hit with big exit fees.