DSCR Loan Requirements: Everything Investors Need to Qualify in 2026

Most DSCR loans in 2026 come down to investor loan programs: the property’s rent, your credit score, your down payment, your cash reserves, and whether the property is a non-owner-occupied rental.

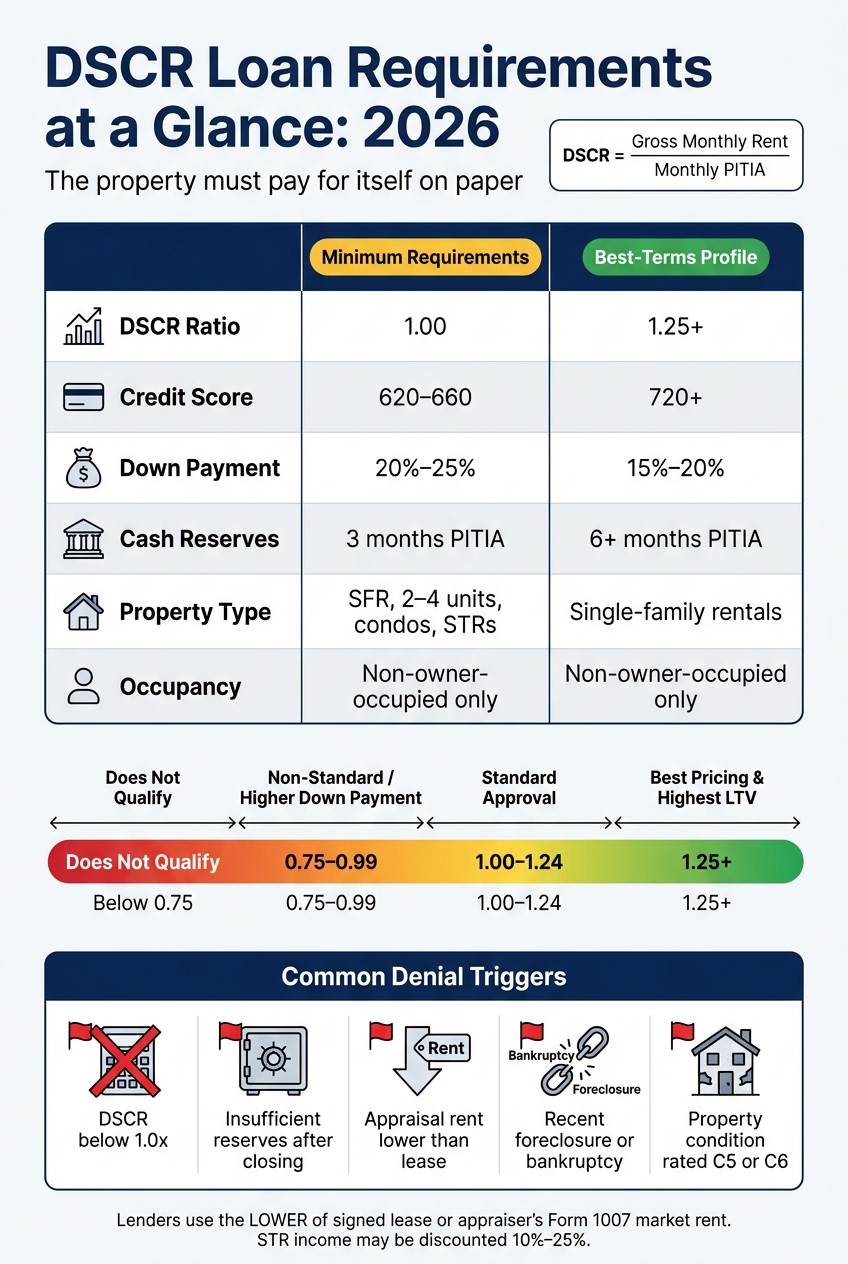

If I had to boil the article down to one point, it’s this: the property has to pay for itself on paper. In most cases, lenders want a DSCR of 1.00 or higher, a 620–660+ credit score, 20%–25% down, and at least 3 months of PITIA reserves after closing. Better files often land closer to 1.25 DSCR, 720+ credit, and 6+ months of reserves.

Here’s the short version:

- DSCR formula: monthly rent ÷ monthly PITIA

- Common minimum DSCR: 1.00

- Low-DSCR programs: sometimes 0.75, often with more money down

- Credit floor: often 620 to 660

- Down payment: often 20% to 25%

- Reserves: often 3 to 6 months of PITIA

- Property use: rental only, not a primary home

- Rent proof: lease, rent roll, or appraiser rent estimate

- Common denial triggers: low DSCR, weak appraisal rent, low reserves, poor property condition, or recent major credit issues

A few details matter more than many investors expect. Lenders often use the lower of the lease amount or the appraiser’s market rent. Insurance, taxes, and HOA dues can push a file from pass to fail because they increase PITIA. And if the property is a short-term rental, income may be discounted by 10% to 25%.

| Item | What lenders often want in 2026 |

|---|---|

| DSCR | 1.00+ |

| Stronger file | 1.25+ |

| Credit score | 620–660 minimum |

| Better pricing range | 720+ |

| Down payment | 20%–25% |

| Reserves | 3–6 months PITIA |

| Occupancy | Non-owner-occupied |

| Ineligible use | Primary residence |

Bottom line: if you want a cleaner approval path, go in with a rent-ready property, a clear paper trail, enough cash left after closing, and a deal that still works even if the appraisal rent or insurance number comes in lower than expected.

DSCR Loan Requirements at a Glance: Minimum vs. Best Terms (2026)

No W2? How the DSCR Loan Difference Saves You

sbb-itb-e7c549b

How Lenders Calculate DSCR and Use It to Approve a Deal

Lenders start with one core test: does the property's rent cover the monthly debt payment?

If the answer is no, the deal usually gets tough fast. If the answer is yes, the file has a much better shot of moving ahead.

The DSCR Formula: Gross Monthly Rent Divided by PITIA

The standard DSCR formula is gross monthly rent ÷ monthly PITIA. PITIA stands for Principal, Interest, Taxes, Insurance, and HOA dues when HOA applies. If the loan is interest-only, underwriters usually switch to ITIA - Interest, Taxes, Insurance, and HOA dues - instead of PITIA.

Here’s the simple version: if a property brings in $2,500 per month in gross rent and the monthly PITIA is $2,000, the DSCR is 1.25.

That number matters a lot. It can shape the rate, the max loan amount, and whether the deal keeps moving.

Lenders also tend to underwrite using the lower of the signed lease or the appraiser’s Form 1007 market rent. So if the lease says one number but the appraiser comes in lower, the lower figure is what counts.

Minimum DSCR Ratios Lenders Look For in 2026

A 1.00 DSCR means the property is basically breaking even. A 1.25 DSCR often opens the door to better pricing and stronger leverage. Some non-standard programs go as low as 0.75, but there’s usually a tradeoff: bigger down payments and higher rates.

| DSCR Ratio | Lender Classification | Typical Outcome in 2026 |

|---|---|---|

| 1.25+ | Stronger Pricing | Best pricing and highest LTV (up to 80%–85%) |

| 1.00–1.24 | Standard/Break-even | Standard terms |

| 0.75–0.99 | Negative Cash Flow | Non-standard programs; usually requires 30%–35% down |

| Below 0.75 | High Risk | Generally does not qualify at most lenders |

What Can Lower DSCR Before Closing

A deal can look fine at first and then slip before closing. That happens more often than people expect.

Higher-than-expected insurance binders can increase PITIA and pull the ratio down. That’s why shopping for insurance early matters. It helps keep the premium used in underwriting closer to the final number.

Property taxes can move the needle too. In high-tax states like Texas, taxes can make up a big share of PITIA, and even a small bump can drag a borderline deal below 1.00. HOA dues can do the same thing.

Short-term rentals are another spot where lenders get careful. They often use a discounted income figure - usually 10% to 25% below projected gross revenue - because they account for seasonality and vacancy.

Once the ratio gets past the minimum, lenders usually move on to the other parts of the file: credit, reserves, down payment, and property eligibility.

Core DSCR Loan Requirements Investors Must Meet in 2026

Once a property clears the DSCR test, lenders move on to the rest of the file: credit score, down payment, cash reserves, property type, and borrower history. Put simply, the ratio gets you in the door. After that, underwriting looks at the borrower, the property, and the cash behind the deal.

Here’s where most lenders tend to land in 2026:

| Requirement | Typical Minimum | Best Terms |

|---|---|---|

| Credit Score | 620–660 | 720–740+ |

| Down Payment | 20%–25% | 15%–20% |

| Cash Reserves | 3 months PITIA | 6+ months PITIA |

| Property Types | SFR, 2–4 units, condos, townhomes, STRs | Single-family rentals (SFR) |

| Occupancy | Non-owner-occupied only | - |

| Borrower History | Clean recent mortgage payment history preferred | Fewer credit events, stronger profile |

These ranges reflect standard 2026 DSCR programs, with stronger credit and DSCR profiles leading to better leverage and lower rates.

Credit Score, Down Payment, and Cash Reserve Requirements

After DSCR, credit and liquidity are usually the next two gates.

Most lenders set the credit floor at 620 to 660. But once a file drops below 660, pricing often gets worse and max LTV tends to shrink. Borrowers with 720+ scores usually get the best pricing and may qualify for a lower down payment.

Cash reserves matter too. Lenders often want 3 to 6 months of PITIA left in liquid or cash-equivalent accounts after closing. For bigger loans, multi-unit properties, or files with a sub-1.00x DSCR, that reserve requirement often jumps to 9 to 12 months.

There’s also a paper-trail piece here. Those funds usually need to be in the account for at least 60 days before closing, and large recent deposits may need to be sourced. So if money just showed up last week, expect questions.

Eligible Property Types and Occupancy Rules

DSCR loans are built for income-producing, non-owner-occupied properties. The most common property types are:

- Single-family rentals

- 2–4 unit properties

- Condos

- Townhomes

- Short-term rentals (STRs)

Some niche lenders also lend on 5–8 unit multifamily or mixed-use properties.

On the flip side, some properties are usually off the table: primary residences, second homes, fix-and-flip projects that are not rent-ready, raw land, and co-ops. Properties with severe deferred maintenance or an appraisal condition rating of C5 or C6 are also often ineligible.

Not all property types get treated the same. SFRs usually get the best LTV treatment. Non-warrantable condos are often capped at 65% LTV, which means a bigger down payment no matter how strong the credit score is.

Borrower Background Standards Beyond Income Verification

After credit and reserves, lenders still look at the borrower’s payment history and how the deal is being vested.

They review credit history and recent payment behavior. More than three recent 30-day mortgage lates can trigger a denial. Bankruptcies and foreclosures usually come with a 24- to 36-month seasoning period before most lenders will look at the file.

Many investors close in an LLC, but lenders still usually want a personal guarantee from the guarantor. If you’re vesting in an entity, it helps to have your Articles of Organization, Operating Agreement, and EIN letter ready before the loan process starts.

Property, Rent, and Appraisal Documents You Need to Qualify

Once the borrower file clears, underwriting shifts to the property file. At that point, the lender wants to confirm two things: the property supports the loan amount, and the rent is enough to help cover the debt. The proof you need depends on how the property is used.

Lease, Rent Roll, and Market Rent Documentation

Lenders check rental income differently based on whether the property is occupied, vacant, or run as a short-term rental.

For an occupied rental, lenders usually ask for a signed lease agreement. They may also want 12 months of canceled checks or bank statements that show rent deposits so they can verify the payment history. Then they compare the lease amount to the Form 1007 market rent estimate and use the lower number.

For 2–4 unit properties, you’ll also need a rent roll that lists each unit, the current rent, and whether the unit is occupied.

For a vacant property, the appraiser’s market rent estimate becomes the income used for qualifying. Since there’s no lease to review, the lender leans on comparable rentals in the area.

Short-term rentals are a different animal. Lenders often want both income proof and platform history. In many cases, that means 12 to 24 months of platform records or third-party data to support the income figure used for qualifying.

Appraisal Standards and Property Condition Requirements

The appraisal sets both the property value and the market rent. Lenders often order:

Each of those is usually paired with a Form 1007 rent schedule. To set market rent, appraisers review recent nearby rental comps.

Condition matters just as much as value. If the property has deferred maintenance or isn’t rent-ready, the appraiser may give it a C5 or C6 condition rating. That can knock the property out of the deal or lead to an appraisal with repair conditions, which can slow funding.

The property also needs landlord insurance, not a standard owner-occupied homeowner’s policy.

If the appraisal, rent documents, and property condition match up, the file moves to final underwriting.

How to Improve Approval Odds and Avoid Common Denial Reasons

The Most Common Reasons DSCR Loans Get Denied

Once the main DSCR, credit, reserve, and property rules are in place, most denials come down to a handful of file problems that can often be avoided.

The biggest one is a DSCR below 1.0x. That means the property's rent doesn't fully cover PITIA. When that happens, the file will usually get denied or approved only on much tougher terms.

Other deal-breakers show up again and again:

- Recent major credit events: A recent foreclosure, bankruptcy, or serious delinquency can push approval back until seasoning rules are met.

- Appraisal shortfalls: If market rent comes in lower than the lease amount, the lender uses the lower figure. That can push the file under the minimum DSCR.

- Insufficient reserves: Not having enough liquid PITIA reserves after closing can sink the deal.

- Property issues: Weak rental comps, high insurance costs in flood-prone areas, or C5/C6 condition ratings can stop an approval.

- Owner-occupancy misrepresentation: If the lender sees any sign that the borrower plans to live in the property, the loan can be declined because DSCR loans are business-purpose loans.

- STR restrictions: If local zoning or the HOA doesn't allow short-term rentals, lenders usually won't count that income. And that can break the deal.

How to Strengthen a DSCR File Before You Apply

Before underwriting begins, clean up the parts of the file you can control.

Credit score is one of the fastest levers to pull. Pay revolving balances down below 30% utilization, and if you can, get closer to 10%, at least 30 to 60 days before applying. Also, avoid opening new credit lines in the 60 to 90 days before you submit the file.

Down payment is another big lever. Moving from 20% down to 25% down cuts the loan amount and can help a borderline property get over the minimum DSCR line.

Reserves should be liquid and seasoned. Most lenders want 3 to 6 months of PITIA after closing, and larger loans may call for more.

Insurance costs matter more than some borrowers expect. Since insurance is part of PITIA, a lower premium quote can directly improve the DSCR before the file goes in.

Conclusion: The Shortest Path to Qualifying in 2026

The shortest path to approval is simple: send in a complete file with strong DSCR, clean credit, enough reserves, and rent-ready property documents.

Aim for at least a 1.25x DSCR, a 720+ credit score, 3 to 6 months of liquid PITIA reserves after closing, and a rent-ready property with confirmed rental comps, valid lease documents, and entity paperwork ready before the lender even asks.

FAQs

Can I qualify if the property is vacant?

Yes. You can still qualify for a DSCR loan if the property is vacant.

When there isn’t an active lease in place, the lender usually relies on an appraisal plus a Form 1007 Rent Schedule. That form estimates market rent based on similar local rental properties.

The lender then uses that estimated market rent to calculate the property’s DSCR.

Do DSCR lenders use the lease rent or the appraiser’s rent?

For DSCR loans, lenders usually use the lower of these two numbers:

- The rent in the signed lease

- The appraiser’s market rent estimate on Form 1007

If the property is occupied, the lender will look at the executed lease. But the appraiser’s market rent can still act as a cap on the income used to qualify.

That matters most in two cases:

- The property is vacant

- The lease amount is below market rent

So even if there’s a tenant in place, the income used for qualification may be limited by what the appraiser says the property should rent for on the open market.

What counts as reserves for a DSCR loan?

For a DSCR loan, reserves are liquid assets you still have after closing costs and the down payment. Lenders usually measure them by how many months of the property’s PITIA they cover: principal, interest, taxes, insurance, and HOA.

Common reserve sources often include:

- Seasoned checking and savings accounts

- Investment accounts, such as stocks, bonds, or mutual funds

- Vested retirement accounts

- Cash-value life insurance

On the flip side, property equity, business accounts, and unseasoned deposits usually don’t count.