DSCR Loan for Short-Term Rentals: Qualifying With Airbnb and VRBO Income

If your Airbnb or VRBO brings in enough rent to cover the monthly housing payment, you may qualify for a DSCR loan without relying much on personal income.

I’d boil it down like this:

- Lenders focus on the property’s cash flow, not just your W-2 or tax returns

- A DSCR of 1.00x is often the floor

- A DSCR of 1.25x+ usually puts you in a stronger spot

- Existing rentals usually need 12 to 24 months of income records

- New purchases or conversions often use AirDNA and an STR-friendly appraisal

- Projected income is often trimmed to 70% to 80%

- Most borrowers need 20% to 30% down

- Many lenders want 6 to 12 months of PITIA in reserves

- The property must allow short-term rentals under local rules, zoning, and HOA terms

Here’s the part many borrowers miss: top-line Airbnb income is not the same as qualifying income. Lenders often cut projected rent, check low-season performance, and test whether the property still covers principal, interest, taxes, insurance, and HOA dues.

A simple example:

- Monthly Airbnb income: $5,000

- Monthly PITIA: $4,000

- DSCR: 1.25x

That ratio often works much better than a deal sitting near 1.00x, where even a small drop in occupancy can hurt the file.

If I were sizing up an STR deal fast, I’d check four things first:

- Is the property legal as a short-term rental?

- Will the lender use actual income or projected income?

- Does the deal still work after income cuts and slow-season checks?

- Do I have enough down payment, credit, and reserves?

Can You Use a DSCR Loan for an Airbnb?

sbb-itb-e7c549b

Quick comparison

| Scenario | Income Source | What Lenders Usually Want | Common Catch |

|---|---|---|---|

| Existing Airbnb/VRBO | 12–24 months of host statements and bank deposits | Documented payout history | Seasonal swings can lower usable income |

| New STR purchase | AirDNA report + STR appraisal | Market rent support | Projected income is often reduced |

| Long-term to STR conversion | Market data + appraisal rider | Local STR approval | If STR use is not allowed, deal may fall back to long-term rent |

In short, DSCR loans can work well for short-term rentals, but only when the numbers still hold up after lender cuts, reserve checks, and legal review.

Step 1: Gather the Short-Term Rental Income Documents Lenders Review

Underwriters use your paperwork to confirm that the rental income is real, steady, and allowed under local rules. The documents you need depend on the income method the lender plans to use.

Documents for an Existing Airbnb or VRBO Property

If the rental is already live, underwriters usually ask for platform payout statements and booking history reports from Airbnb or VRBO. They don't want to see only the busy months. Peak-season numbers can paint the wrong picture, so lenders need enough history to spot the slow periods too.

Bank statements come next. Underwriters compare platform payouts with matching deposits in your bank account to make sure the funds actually showed up. This is where a separate bank account used only for STR deposits can save a lot of back-and-forth. If you use a property management system, those reports can also help support the file, especially when income comes from more than one platform.

You should also include proof of the STR permit or transient occupancy tax registration. If the home can't legally run as a short-term rental, it won't qualify for STR-based income underwriting.

Documents for a Purchase or New Short-Term Rental Conversion

If the property doesn't have an operating history yet, the lender leans on market data instead. In that case, use an AirDNA Rentalizer or MarketMinder report to estimate gross revenue based on similar STRs in the area, including bedroom count, location, and amenities.

You'll also want an appraisal that includes an STR income schedule, not just a long-term rent estimate. That's a big deal. A standard appraisal will usually limit income to long-term market rent, and that number is often lower than what a short-term rental may bring in.

Local compliance paperwork matters here too. Show proof from the city or county that the property is in a zone where STR use is allowed. And if the loan will close in an LLC, have the entity documents ready to go.

Comparison Table: Historical Income vs. Projected Income

| Factor | Historical Income (Existing STR) | Projected Income (Purchase/Conversion) |

|---|---|---|

| Use Case | Refinancing an operating STR | New purchase or long-term rental conversion |

| Primary Document | Platform payout statements | AirDNA Rentalizer report + STR appraisal rider |

| Verification Method | Matching bank deposits and PMS reports | Appraiser's STR market rent schedule |

| Income Credit | 90–100% of documented revenue | 70–80% of projected revenue (haircut applied) |

| History Needed | 12+ months | 0–11 months |

Once you've pulled these documents together, the lender can start turning that file into underwritten rental income.

Step 2: Understand How Lenders Calculate Projected STR Income

Once your paperwork is set, the lender turns Airbnb and VRBO data into one qualifying income number. That figure then drives the rest of the file: DSCR, cash reserves, and how much you may be able to borrow.

Appraisal-Based Rent Tools and STR Income Reports

Many lenders use AirDNA's Rentalizer to estimate short-term rental income for underwriting. It pulls from similar active listings in the area and estimates average daily rate (ADR) and occupancy. Some lenders won't use that projection unless the AirDNA market score is 60 or higher.

For a purchase or a new STR conversion, the underwriter may also use a special appraisal that includes a short-term rental schedule or rider. In most cases, lenders order Form 1007 for single-family homes and Form 1025 for 2-4 unit properties. Appraisal costs usually run from $500 to $900.

After the lender accepts the income source, it doesn't just take the top-line number at face value. It usually applies haircut, expense, and seasonality adjustments before the loan moves forward.

| Income Method | Data Reviewed | Typical Lender Treatment |

|---|---|---|

| Actual 12-month booking history | Airbnb/VRBO host statements or PMS data | Often 90% to 100% of documented income |

| AirDNA projections | Rentalizer market analytics report | Often 70% to 90% of projected income |

| AirDNA + partial history | AirDNA plus partial history | Often 80% to 90% of the blended figure |

Occupancy, Nightly Rate, and Seasonality Assumptions

Lenders usually lean on the median AirDNA data point to stay conservative, although some may allow the 75th percentile for higher-end properties. A common approach is to apply a 25% expense ratio and treat the remaining 75% as Effective Rental Income (ERI).

They also pressure-test seasonality. For example, an underwriter may look at the three lowest consecutive months of projected revenue and annualize that amount to see if the property can still cover debt service during the slow season. If that number comes in thin, the deal can fall below the lender's DSCR floor. When that happens, the lender may ask for more reserves.

So even if the raw Airbnb or VRBO revenue looks strong, the income used for qualification is often lower after these adjustments. That's why DSCR, reserves, and down payment still carry so much weight. Once income is normalized, the lender moves to the next check: whether the property still meets its DSCR, LTV, and reserve rules.

Step 3: Check Your DSCR, Down Payment, and Reserve Numbers Before You Apply

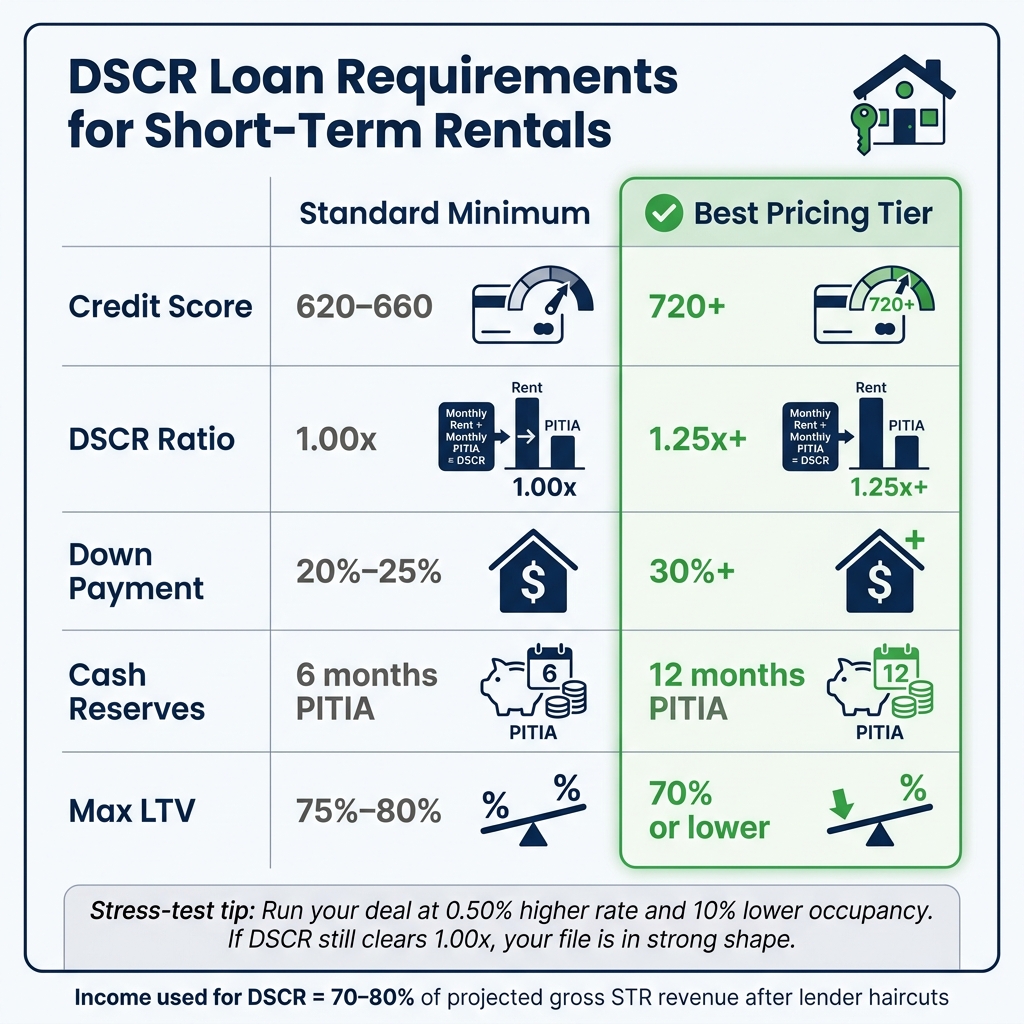

DSCR Loan Requirements for Short-Term Rentals: Key Thresholds at a Glance

Once projected income is normalized, three numbers drive approval: DSCR, down payment, and reserves.

Minimum DSCR Thresholds and How They Affect Approval

After income is normalized, the lender divides qualifying monthly rent by monthly PITIA to calculate DSCR. That ratio plays a big role in whether the deal qualifies and how good the terms may be.

Most STR programs set a hard floor at 1.00x. But in day-to-day lending, 1.25x or higher is usually where the best pricing and terms begin.

A DSCR that sits just above 1.00x doesn't leave much cushion for seasonal swings. One soft month can put pressure on the file fast.

Some niche programs go as low as 0.75x to 0.95x. The catch? Those deals usually need stronger backup factors, like a bigger down payment or more reserves. And if STR income comes in below the lender's floor, some lenders will switch to long-term rent from Form 1007 instead, which is often lower.

A smart move is to stress-test the deal before you apply. Run it at an interest rate 0.50% higher and occupancy 10 points lower than projected. If DSCR still clears 1.00x under those conditions, the file is in much better shape.

When the ratio looks thin, lenders usually try to offset that risk with more equity, more reserves, or both.

Loan-to-Value, Cash Reserves, and Credit Profile

Down payment size affects both the monthly payment and the DSCR. Most STR programs ask for 25% to 30% down, which means a maximum LTV of 70% to 75%. Borrowers with strong DSCR and credit scores above 720 may be able to get 20% down options.

Credit score also affects rate and LTV. Most STR-focused programs want at least 660 to 700, while 720+ is usually where the best pricing starts. On top of that, lenders often want 6 to 12 months of PITIA in liquid reserves to help cover seasonal income dips. In plain English: keep enough cash on hand to get through slow months.

| Requirement | Standard Minimum | Best Pricing Tier |

|---|---|---|

| Credit Score | 620–660 | 720+ |

| DSCR Ratio | 1.00x | 1.25x+ |

| Down Payment | 20%–25% | 30%+ |

| Cash Reserves | 6 months PITIA | 12 months PITIA |

| Max LTV | 75%–80% | 70% or lower |

Even with strong numbers, the deal can still fall apart if the property can't legally operate as a short-term rental.

Property Eligibility and Local STR Rules

Strong revenue projections won't save a property that isn't eligible.

Start with property type. Standard 1- to 4-unit residential properties usually qualify without much trouble. Condos and condo-hotels are tougher. They often come with stricter LTV caps, usually around 65% to 75%, and some lenders won't finance condo-hotels at all.

Then look at the HOA and condo documents. Some associations allow rentals only when stays are at least 30 days, which can wipe out STR income eligibility. Others give the board the power to block short-term use later, which adds rule-change risk even if the current language seems open.

Check legality before you submit an LOI. If the property can't legally run as an STR, it won't qualify.

The last gate is local zoning and permitting. Cities such as Nashville, New York City, and San Francisco require owner occupancy for some STR permits, which can shut out non-owner-occupied DSCR deals. Places like Gatlinburg, TN, Myrtle Beach, SC, and Scottsdale, AZ are usually seen as lower-risk because local rules are more permissive. Also make sure STR permits are available right now, not just allowed on paper, before you submit an application.

If the property clears these checks, the financing case is much easier to support.

Conclusion: How to Position an Airbnb or VRBO Property for Financing

Once income, DSCR, and reserve checks are in place, approval usually comes down to one thing: can the property cover its debt under conservative underwriting? Start there. Make sure the property can legally run as a non-owner-occupied STR under local zoning and HOA rules. Legal STR use is the first screen.

Then keep the file clean. If it's an existing Airbnb or VRBO, lenders want documented platform earnings that show steady revenue they can use for underwriting. If it's a purchase, use an appraiser's STR rent schedule or a third-party revenue projection report such as AirDNA. But don't underwrite the top-line figure. A safer approach is 70% to 80% of projected gross revenue. After the lender accepts the income source, that number gets adjusted before DSCR is tested.

Next, run qualifying income against PITIA. A 1.25x+ DSCR puts the deal in a much stronger spot. If the deal feels tight, putting more money down can cut the monthly PITIA and help the file work.

Most STR programs also want:

- 20% to 30% down

- 6 to 12 months of PITIA in liquid reserves

- A credit score in the 700+ range for better pricing

That mix is what usually makes a short-term rental financeable.

Short-term rentals tend to qualify best when the income is documented, the property is legal, and the deal still works under conservative DSCR assumptions.

FAQs

Can I qualify with projected Airbnb income?

Yes. For properties without 12 months of operating history, some lenders may still approve a DSCR loan by using projected Airbnb and VRBO income from third-party market data, most often AirDNA reports.

In most cases, they count only 75% to 80% of projected gross income to account for seasonality and market swings. Some lenders also compare that figure with a long-term rent estimate from Form 1007 and use the lower amount.

What if my STR is seasonal?

Seasonal properties are still financeable, but lenders plan for uneven income. To do that, they may use reports like AirDNA to estimate annual revenue across both busy and slow seasons.

Some lenders also stress-test the lowest 3 consecutive months of projected revenue. Since income can swing a lot from season to season, you should expect tighter reserve rules - often 6 to 12 months of PITIA - to help cover payments during the off-season.

Can I use an LLC for the loan?

Yes. You can often use an LLC for a DSCR loan, and many short-term rental investors do exactly that.

In most cases, the lender will ask for the LLC’s paperwork, such as the operating agreement and EIN, so the loan can close in the entity’s name instead of your personal name.