Investment Property Line of Credit: Can Investors Access Equity Without Selling?

Yes - you can tap rental property equity without selling, but most investors end up choosing between a rental HELOC, a cash-out refinance, a DSCR cash-out loan, or a portfolio line. The main limits are usually credit score, cash reserves, property type, and loan-to-value caps of about 70% to 80%.

If I were sizing up this choice fast, I’d focus on four things:

- Need cash in stages? A HELOC may fit.

- Need one lump sum? A cash-out refinance or DSCR cash-out may fit.

- Own multiple rentals? A portfolio or cross-collateral line may fit.

- Have a low first mortgage rate? Keeping that loan in place with a second lien can help avoid refinancing the full balance at a higher rate.

The big tradeoff is simple: borrowing against equity can free up cash, but it also adds debt, rate risk, and payment pressure. For many investors, the best use cases are down payments, rehab costs, bridge funding, and reserve support - not patching up a weak rental that already struggles to cash flow.

How to Get a HELOC on Investment Property | 2026 Expert Strategy

sbb-itb-e7c549b

Quick Comparison

| Option | Best for | How you get funds | Main downside |

|---|---|---|---|

| Investment HELOC | Repairs, staged projects, backup reserves | Revolving line | Variable rate and payment jump later |

| Cash-out refinance | One-time large cash need | Lump sum | Replaces your current mortgage |

| DSCR cash-out | Investors using rent to qualify | Lump sum | Fees can be higher and terms vary by lender |

| Portfolio / cross-collateral line | Investors with several properties | Larger line across properties | More than one property can be tied to the debt |

In short: you do not need to sell to use your equity, but the right option depends on how much cash you need, when you need it, and whether the property can still carry the debt if rates move up.

How investment property lines of credit work

An investment property line of credit is a revolving loan backed by equity in a rental property. You borrow only what you need, pay it back, and then borrow again from the same line - kind of like a credit card, except the property secures the debt. For investors, that’s the main draw: you turn locked-up equity into cash you can use without selling the property.

That setup affects three big things at once:

- how much money you can access

- how fast borrowing costs can change

- whether the loan lines up with your plan

If the rental already has a first mortgage, the line of credit usually sits behind it in second position as a second lien. That matters because the first mortgage gets paid first if things go sideways. Since that puts the second lien lender in a riskier spot, lenders usually tighten the rules and offer lower credit limits on investment properties than they do on owner-occupied homes.

Draw periods, repayment periods, and variable-rate risk

Most investment property lines of credit use a two-phase setup.

During the draw period, which usually lasts 5 to 10 years, you can borrow as needed. Payments are often interest-only, based only on the amount you’ve used.

After that comes the repayment period, which is commonly 10 to 20 years. At that point, the remaining balance is re-amortized into full principal-and-interest payments.

That switch can hit hard. A $100,000 balance at 9% costs about $750 per month during the draw period, then the payment climbs once repayment starts. And there’s another catch: most investment HELOCs use a variable rate, often set at prime plus 2% to 4%. So even before the draw period ends, your monthly payment can go up if rates move higher.

Those terms matter. But approval usually comes down to a more basic set of lender filters: equity, credit, cash reserves, and the kind of property you own.

LTV limits, credit requirements, reserves, and property type restrictions

Lenders take a tougher stance on rental properties, and you can see it in the numbers below:

| Underwriting Factor | Typical Expectation |

|---|---|

| Credit score | 700–720 minimum |

| Maximum combined loan-to-value (CLTV) | 70%–80% |

| Cash reserves | 6 months of PITIA expenses |

| Ownership seasoning (time since purchase) | 6–12 months |

| Rate type | Variable, prime plus margin |

These limits decide what the line can actually do for you - cover a down payment, pay for repairs, or smooth out short-term cash flow.

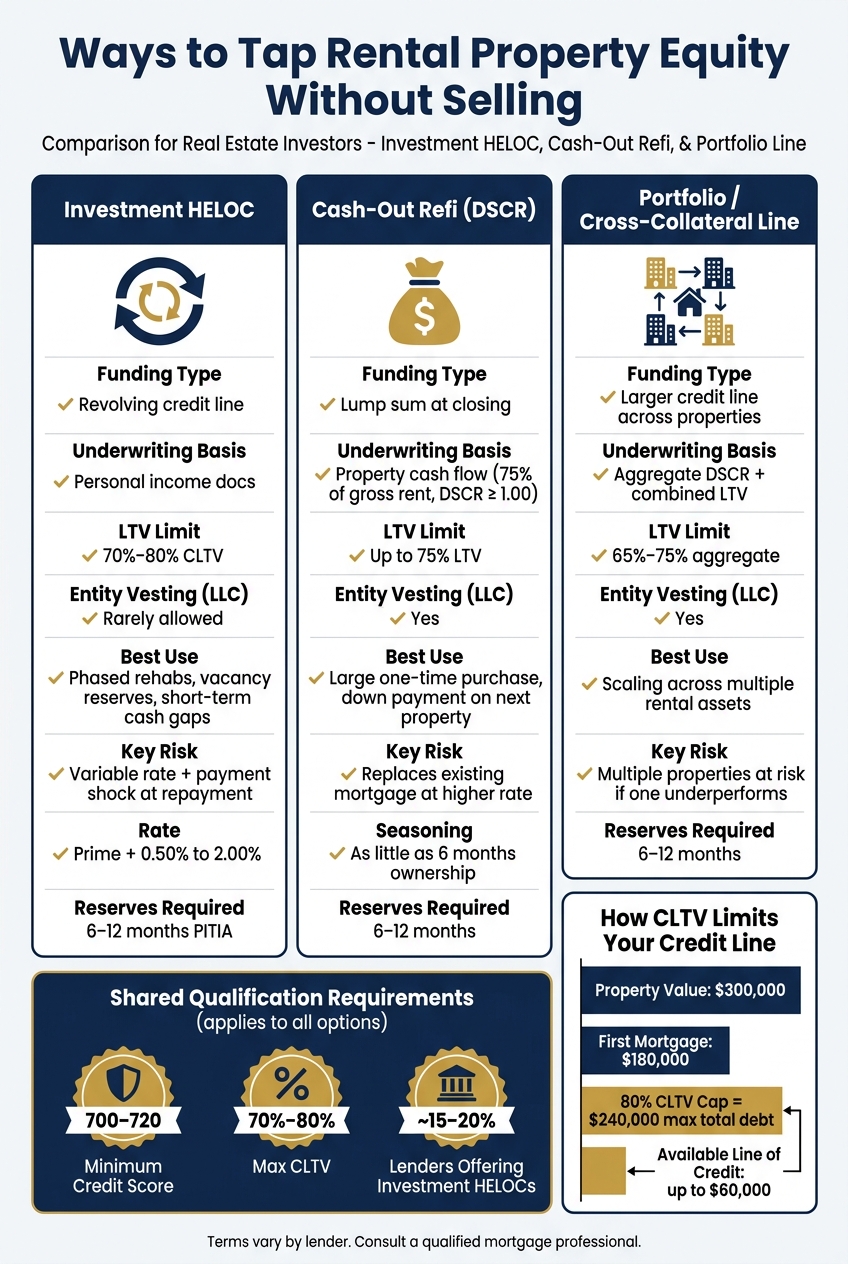

The CLTV cap is one of the biggest constraints. Say you own a $300,000 rental with a $180,000 first mortgage. If the lender caps CLTV at 80%, the total debt allowed is $240,000. Subtract the first mortgage, and you’re left with a line of credit of up to $60,000.

Property type also changes the math. Single-family rentals are the easiest fit and often qualify at about 70% to 75% CLTV. Two-to-four-unit properties usually face lower caps, often 65% to 70%, along with tighter DTI and reserve rules.

Once you get to five or more units, HELOC-style products usually drop off the table and commercial financing becomes the normal route. And that’s before you factor in lender availability: only about 15% to 20% of HELOC lenders offer these products on investment properties at all. So compared with borrowers using a primary home, investors have a much smaller lender pool to work with.

Those limits often decide which route makes more sense: a second lien, a cash-out refinance, a DSCR loan, or a portfolio line of credit.

Main ways to tap equity without selling

Investment Property Equity Options: HELOC vs Cash-Out Refi vs Portfolio Line

The best option comes down to one thing: do you need money over time, or all at once? Each loan setup works a bit differently, and those differences shape how investors use them and where the risk shows up.

HELOC-style second liens on rental properties

A rental HELOC is a second lien that sits behind your first mortgage and gives you a revolving credit line. You draw what you need, pay it back, and borrow again.

That setup works well for phased rehabs, vacancy reserves, or short-term cash gaps. You only pay interest on the amount you use, which gives you more control when project costs come in waves instead of all at once.

The catch? That flexibility usually means tighter underwriting and higher costs.

Cash-out refinance and DSCR-based equity options

A cash-out refinance replaces your current mortgage with a larger one and gives you the difference as a lump sum at closing. If you need one big chunk of cash instead of open-ended access, this is often the cleaner path.

For investors who want the loan based on property income, a DSCR cash-out refinance leans on rental income instead of personal tax returns. That's a big plus for self-employed borrowers or rentals held in an LLC, especially when the goal is a down payment or a new purchase.

Many programs allow up to 75% LTV and may ask for only a six-month ownership seasoning period.

Portfolio and cross-collateral credit lines

If one rental doesn't have enough equity on its own, a portfolio or cross-collateral credit line can pool equity across several properties. Lenders look at the deal using aggregate DSCR and combined LTV, which can open the door to a larger facility than a single-property line.

But there's a tradeoff. With cross-collateral lines, every pledged property is on the hook. Trouble with one rental can spill into the others. That's why this kind of setup needs a clear-eyed look at credit, reserves, and cash flow before a lender signs off.

| Feature | Investment HELOC | Cash-Out Refi (DSCR) | Portfolio / Cross-Collateral LOC |

|---|---|---|---|

| Funding type | Revolving line | Lump sum | Larger credit line |

| Underwriting basis | Personal income docs | Property cash flow | Aggregate DSCR |

| LTV limit | 70%–80% CLTV | Up to 75% LTV | 65%–75% aggregate |

| Entity vesting | Rarely allowed | Yes | Yes |

| Best use | Phased rehabs, reserves | Large one-time purchase | Scaling across multiple assets |

| Key risk | Variable rate, payment shock | Rate increase on the full balance | Multiple properties at risk |

Qualification, costs, and cash-flow tradeoffs

What lenders review before approving equity access

Once investors understand the main equity options, the next step is simple: can you qualify, and does the loan still make sense on paper?

For DSCR loans, lenders usually count 75% of gross rent and look for a DSCR of 1.00 or higher. Approval leans heavily on the property's income, not the borrower's personal income. That's why these loans can work well for self-employed borrowers or for rentals owned in an LLC. Lenders also often want 6 to 12 months of reserves set aside for vacancies, repairs, or other bumps in the road. Many programs ask for 12 months of ownership for HELOCs and as little as 6 months for DSCR cash-out refinances.

Interest rates, fees, and tax considerations

Borrowing against a rental property usually costs more than borrowing against a primary home. Investment HELOCs often come in above prime, commonly at Prime + 0.50% to 2.00%. On top of that, there may be appraisal, origination, and closing costs. DSCR refinances can also include a prepayment penalty.

But cost isn't just about the rate. Taxes matter too.

Under the interest tracing rules, if the borrowed money is used for buying, building, or substantially improving a rental property, the interest is generally deductible on Schedule E. One practical move: send all draws through a dedicated bank account so you have a clean paper trail for the IRS. That small step can save a lot of trouble later. Since tax treatment can get messy fast, it's smart to check your own case with a qualified tax professional before you count on a deduction.

Borrowing versus keeping equity locked: a side-by-side comparison

The main issue isn't just whether you can tap equity. It's whether the added payment helps the next deal without hurting monthly cash flow.

If a rental already runs on thin margins, adding debt service can push it from profitable to break-even. So before moving ahead, stress-test the numbers. Ask yourself: does this property still cover its costs if interest rates jump by 2 to 3 percentage points?

There's one case where leaving equity alone often makes a lot of sense: when your current first mortgage has a rate far below today's market rates. A cash-out refinance means refinancing the entire loan at that higher rate. The lump sum may look good upfront, but it might not make up for the bigger monthly payment over time.

The table below lays out how each option affects cash flow and risk.

| Strategy | Cash-Flow Impact | Risk Level | Best For |

|---|---|---|---|

| Keep equity locked | No added debt; maximizes monthly net cash flow | Lowest | Conservative investors with low-rate existing debt |

| Investment HELOC | Interest-only during draw; variable rates can increase costs | Moderate | Staged renovations, short-term cash needs, vacancy reserves |

| Cash-out refinance | Higher monthly payment if rates have risen; fixed-rate options add stability | Moderate | Large one-time acquisitions or long-term debt restructuring |

| Portfolio / cross-collateral line | Variable; depends on total draw across the portfolio | Higher; multiple properties at risk | Seasoned investors scaling a large portfolio |

The best fit comes down to your equity cushion, current rate, cash reserves, and what the money is for. A line of credit used lightly as a backup reserve is one thing. Drawing it down to fund a deal on a property with weak rent coverage is a whole different ballgame.

Conclusion: When tapping equity makes sense for U.S. investors

Yes - investors can tap rental equity without selling. But the best setup comes down to a few plain factors: how much equity is available, how fast the cash is needed, and whether the goal is a one-time lump sum or an open line you can use over time.

A HELOC-style second lien makes the most sense when you want to keep a low first-mortgage rate and still have access to cash as needed. A DSCR cash-out refinance is often a better fit when the goal is a larger lump sum and the loan needs to be approved based on rental income instead of personal tax returns. Portfolio and cross-collateral lines can work well for investors who want to borrow against more than one property at the same time. There isn't one best choice for everyone. The right move depends on your equity, your cash reserves, and your plan for paying the money back.

Qualification standards change by lender and loan type. For self-employed borrowers, 1099 earners, and properties held in an LLC, DSCR and Non-QM loans often provide a more practical route to equity access than conventional financing.

The strongest cases for borrowed equity are pretty clear: using it for a down payment on another property, funding a value-add rehab, or covering a refinance bridge. In each case, the money has a defined job and a clear path to pay off. Borrowing just to keep a weak property alive is often a warning sign that the deal needs a harder look.

Key decision points before moving forward

Before you move ahead with any equity product, run these five checks:

- Confirm usable equity against the lender's CLTV cap. Most investment-property programs cap combined loan-to-value at 70%–80%.

- Model the worst case. Stress-test the payment at 1–2 points above today's rate to make sure the property can still carry the debt if rates move up.

- Compare revolving access versus a lump sum. A HELOC lets you pull only what you need, when you need it. A DSCR cash-out refinance gives you a fixed amount at closing, which can be simpler to plan around for a one-time use.

- Understand lien position and seasoning. A second lien leaves your first mortgage in place. A cash-out refinance replaces it. Most lenders want to see several months of ownership before approving either option.

- Use the debt only for a clear return. The numbers tend to work better when borrowed funds go toward an acquisition, rehab, or portfolio growth - not when the plan is fuzzy.

FAQs

How much equity can I borrow from a rental property?

It depends on your property’s appraised value and your lender’s maximum LTV or CLTV. In most cases, lenders set tighter limits for investment properties than they do for primary homes.

For investment-property HELOCs and cash-out refinances, many lenders cap borrowing at 70% to 80% LTV or CLTV. Approval also depends on your credit score - often 700+ - along with the property’s rental income.

Is a HELOC better than a cash-out refinance for investors?

It comes down to what you need the money for and how your current mortgage looks today.

A HELOC can make more sense if you already have a low rate on your first mortgage and don’t want to give that up. It also works well if you want flexible, revolving access to cash for things like home updates or short-term cash flow gaps.

A cash-out refinance can be the better fit if you need a large lump sum, prefer a fixed rate, or want the simplicity of having one loan instead of two. The downside is pretty clear: you replace your current mortgage and start over with new loan terms.

Can I qualify if the property is owned in an LLC?

Yes, you may still qualify if the property is owned by an LLC, but the rules can change from one lender to the next.

Many banks and other standard lenders prefer a property to be titled in your personal name. That said, some portfolio lenders and niche lenders will work with LLC borrowers. Since each lender has its own policy, it's smart to ask about entity-ownership rules early in your search.