Cash-Out Refinance for Investment Properties: A DSCR Loan Strategy Guide

If your rental income can cover the new payment, a DSCR cash-out refinance may let you pull equity without using tax returns or W-2s. In most cases, the file comes down to four things: DSCR, LTV, credit score, and reserves.

Here’s the short version:

- You’ll often need a DSCR around 1.15x to 1.25x

- Many 1–4 unit rentals cap cash-out at 75% LTV

- Rates in mid-2026 often land around 7.0% to 9.5%

- Most lenders want 6 to 12 months of PITIA reserves

- Closing costs often run 2% to 4% of the new loan amount

- The deal only works if the cash you pull out can earn more than the new loan cost

A simple example: if your property is worth $400,000 and the program allows 75% LTV, the new loan may top out at $300,000. If your current payoff is $200,000, that leaves $100,000 before costs. After closing costs, your net cash may be closer to $91,000.

What matters most:

- Rent must support the new PITIA payment

- Equity sets the ceiling

- Rate and fees cut into net cash

- Low reserves, weak appraisal, or short seasoning can kill the file

I’d look at this loan as a business math decision, not just a way to pull cash. If the post-refi payment hurts cash flow or the funds will sit unused, the deal can backfire.

This guide breaks down how the loan works, what lenders check, where deals fail, and when cash-out makes sense for an investor.

Approval Requirements: DSCR, LTV, Equity, Credit, and Reserves

DSCR Requirements and How Rental Income Is Measured

Lenders start with one basic check: does the property's rent cover the new PITIA payment?

Here's a simple example. If a property brings in $2,800 per month in rent and the new PITIA is $2,400, the DSCR comes out to 1.17x. In plain English, the rent covers 117% of the payment.

Most cash-out DSCR loans call for a minimum ratio between 1.15x and 1.25x. A higher ratio usually leads to better pricing and can support a larger loan amount.

To verify rent, lenders usually rely on:

- a signed lease agreement

- an appraiser's Form 1007 Rent Schedule

Short-term rentals are handled a bit differently. Most lenders want 12 months of operating history and will often apply a 20% to 30% haircut to gross revenue.

Once the property meets the DSCR floor, the next step is simple: the lender looks at value, available equity, and reserves to size the loan.

LTV Limits and How Much Equity an Investor Can Pull Out

For 1–4 unit investment properties, cash-out is usually capped at 75% LTV. For multifamily, mixed-use, and short-term rental properties, the cap often falls in the 65% to 70% LTV range.

Cash-out is usually calculated like this:

- Maximum new loan: $400,000 × 75% = $300,000

- Subtract existing payoff: $300,000 − $200,000 = $100,000

- Subtract estimated closing costs at about 3%: $100,000 − $9,000 = about $91,000 net cash

That about $91,000 is the estimated cash the investor would receive at closing. Closing costs usually run 2% to 4% of the new loan amount.

So even if the property has plenty of equity, the final cash-in-hand number gets trimmed by payoff amount, LTV caps, and closing costs.

Credit Score, Reserve Requirements, and Borrower Profile Factors

Most DSCR cash-out programs require a minimum FICO score of 620 to 640, while the best pricing usually goes to borrowers with scores of 720 or higher.

Lenders also usually want 6 to 12 months of PITIA in liquid reserves after closing. And they don't always count account balances dollar for dollar. Brokerage balances are often discounted by about 30%, and retirement balances by about 40%.

These loans are business-purpose loans and often close in an LLC. Borrower history can matter, too. Investors with a track record of five or more properties may qualify for seasoning waivers or higher LTV caps.

Put simply, credit score, reserve depth, and investor track record all affect how much cash a borrower can pull from the refinance.

Those same borrower details also affect pricing, which leads into loan terms and underwriting.

sbb-itb-e7c549b

How a DSCR Cash‑Out Refinance Works | Real Deal Breakdown

Loan Terms, Rates, and Underwriting Details That Affect the Deal

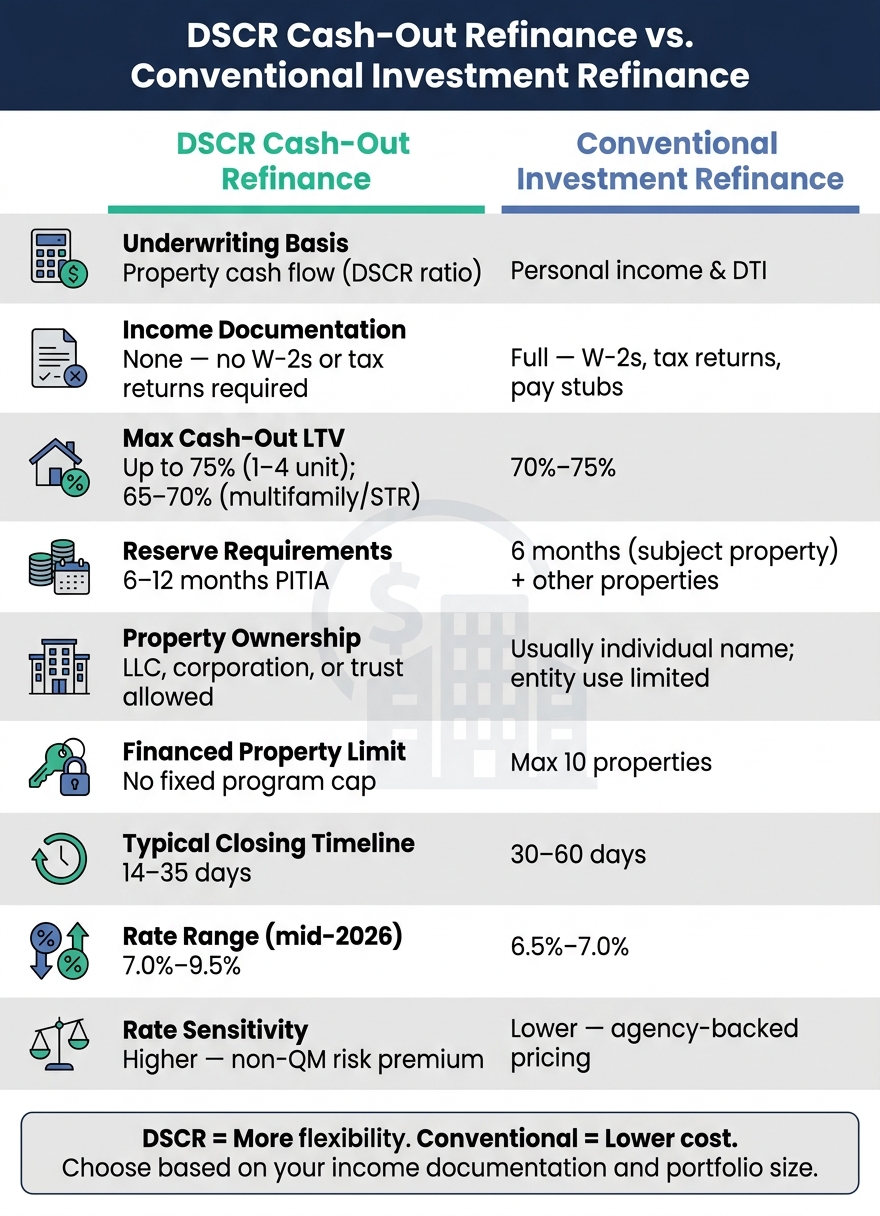

DSCR Cash-Out Refinance vs. Conventional Investment Refinance: Key Differences

Rate Structure, Pricing Adjustments, and Cash Flow Impact

After DSCR, LTV, credit, and reserves, pricing is what decides how much cash you actually walk away with. A loan can clear the DSCR and equity hurdles, but rate, seasoning, and property type still shape the final payout.

DSCR cash-out rates in mid-2026 usually fall between 7.0% and 9.5%. That's about 0.50% to 1.50% higher than conventional investment property rates, which tend to sit around 6.5% to 7.0%. Cash-out deals also come with a 0.25% to 0.75% premium compared with DSCR purchase loans or rate-and-term refinances because lenders see equity withdrawal as a higher-risk move.

A few things can move pricing up or down. A DSCR of 1.25x or higher often gets the best pricing tier. Short-term rental DSCR cash-out rates usually land between 7.75% and 9.25%, while borrowers with FICO scores below 680 should expect rates around 8.25% to 9.0%.

Interest-only (IO) options can help when cash flow is tight. They cut the monthly payment, which improves the DSCR used for approval, though they usually add about 0.25% to the rate. On a $400,000 property with $2,800 in monthly rent, changing from an amortizing loan to an IO structure helped the file reach the 75% LTV cap and increased net cash to the borrower by about $22,800. ARMs, including 5/6 and 7/6 structures, can also help because their starting rates are lower than 30-year fixed loans.

Before you lock anything, compare the new PITIA with the current rent. A higher rate tied to a bigger loan balance can squeeze the DSCR enough to push it below the lender's floor.

Most DSCR loans also come with a prepayment penalty, often in a 3-, 5-, or 7-year step-down format. If you want a shorter penalty period, or want to buy it out, expect another 0.25% to 0.75% added to the rate.

Seasoning Rules, Eligible Property Types, and No-Income-Doc Features

Most lenders follow a tiered seasoning setup. If you've owned the property for less than 6 months, the value may be capped at cost basis. At 6 months, lenders will often use appraised value. Once you get to 12+ months, pricing and LTV are usually at their strongest.

DSCR cash-out programs generally cover 1–4 unit residential properties, warrantable and non-warrantable condos, townhomes, and PUDs. Some niche programs also allow 5+ unit multifamily or mixed-use properties.

One rule doesn't bend: the property must be non-owner-occupied. These are business-purpose loans. If the lender finds signs of personal occupancy, the file will usually be denied on the spot.

Closing in an LLC is usually allowed, and many investors prefer it. In most cases, though, the main member still has to sign a personal guarantee.

Comparison Table: DSCR Cash-Out Refinance vs. Conventional Investment Refinance

The trade-off is pretty straightforward. DSCR gives you more room to work with, while conventional financing usually costs less if you can document your personal income.

| Feature | DSCR Cash-Out Refinance | Conventional Investment Refinance |

|---|---|---|

| Underwriting Basis | Property cash flow (DSCR) | Personal income & DTI |

| Income Documentation | None (no W-2s or tax returns) | Full (W-2s, tax returns, pay stubs) |

| Max Cash-Out LTV | Up to 75% on many 1–4 unit files; lower on multifamily, mixed-use, and short-term rentals | 70%–75% |

| Reserve Requirements | Usually 6–12 months PITIA | 6 months (subject property) + reserves for other properties |

| Property Ownership | LLC, corporation, or trust allowed | Usually individual name; entity use is more limited |

| Financed Property Limit | No fixed program cap | Max 10 properties |

| Typical Closing Timeline | 14–35 days | 30–60 days |

| Rate Sensitivity | Higher (non-QM risk premium) | Lower (agency-backed pricing) |

With the loan structure clear, the next question is whether the cash-out will help the portfolio or put pressure on monthly cash flow.

Best Uses for a DSCR Cash-Out Refinance and Common Approval Obstacles

Using Cash-Out Proceeds to Buy Another Rental, Renovate, or Pay Off Higher-Cost Debt

Once the loan clears underwriting, the next issue is simple: will the cash do more for you than the new debt will cost?

The strongest cases usually come from moving equity into something that can produce a better return. For example, an investor who pulls $75,000 from a stabilized single-family rental at 75% LTV can use that money as a 25% down payment on a new $300,000 rental. That lets the investor grow the portfolio without selling the first property.

Renovation can also make sense when the work lifts income or improves the numbers. In one Miami case, a borrower pulled out $124,500 at 70% LTV and used the funds for renovations that improved the property’s DSCR from 1.03 to 1.27.

Paying off higher-cost debt can work too. In one Houston case, rolling debt into a single 7.375% DSCR loan cut total borrowing cost and freed up $35,750 in liquidity.

The big idea here is straightforward: use cash-out as capital recycling, not spending.

When This Strategy Improves Portfolio Cash Flow - and When It Does Not

This only works if the proceeds earn more than the refinance costs and added interest.

That’s the whole game. If you pull cash out and let it sit, the math can turn against you fast. The money needs to go to work, and it needs to do so soon, or the cost of the refinance starts eating away at the upside.

The new loan can also squeeze DSCR more than some borrowers expect. Since cash-out increases the loan balance and monthly PITIA, a property that covered at 1.10x before the refinance might fall to 0.85x after it. Some programs may still allow a DSCR as low as 0.75x if the borrower can cover the gap, but that often means less breathing room each month on the subject property. That’s why it’s smart to run the post-refinance DSCR before locking in the loan amount.

Closing costs can change the picture too. On a $280,000 refinance with $7,000 in costs and a $260,000 existing balance, the borrower doesn’t walk away with the headline $20,000. The net is $13,000. If you’re counting on that money for a down payment or a rehab budget, that gap matters.

Common Denial Reasons and How to Prepare Before Applying

Even deals that look solid on paper can fall apart when the file misses basic underwriting items.

The usual problem areas are reserves, DSCR, valuation, seasoning, and missing documents.

"Insufficient reserves are the number one reason deals fall apart. A borrower with a 760 credit score and zero reserves will be declined by most lenders, while a borrower with a 680 score and 12 months of reserves is highly fundable." - Mo Abdel, NMLS #1426884

Here’s where borrowers most often run into trouble:

- Reserve shortfalls: These can block approval even when credit and DSCR look good.

- Low DSCR: Higher insurance premiums and property taxes can push ratios down, especially in places like Florida. That can make it harder to qualify for max cash-out even when property values are up.

- Appraisal shortfalls: A lower-than-expected appraisal cuts the amount of cash available, even when the owner seems to have plenty of equity.

- Seasoning gaps: Files that fall short of seasoning rules often lose access to full cash-out proceeds.

- Missing entity or borrower documents: Missing LLC articles of organization, operating agreements, EIN letters, or rent rolls can delay or stop the file.

A cleaner file gives you a better shot. Send in rent proof, payoff figures, reserve statements, and entity documents with the application.

Conclusion: A Checklist for Deciding if a DSCR Cash-Out Refinance Fits Your Plan

Once DSCR, LTV, reserves, and pricing are on the table, this is where you make the call.

A DSCR cash-out refinance lets you turn rental equity into cash without using personal income paperwork. That can be a good fit for self-employed investors, LLC-owned properties, and borrowers who already have too many financed properties for conventional loans.

But this only works when a few things line up. The property needs enough equity. The rent needs to support the new payment at your target DSCR. And the cash-out needs a clear business purpose.

Here’s the plain-English test: if the cash you pull out won’t earn more than the added debt and closing costs, the refinance probably doesn’t make sense.

Key Items to Review Before Moving Forward

Use this table as a last pre-application check.

| Checkpoint | What to Confirm |

|---|---|

| Property value & payoff | Current market value minus existing mortgage balance = available equity |

| LTV ceiling | Max LTV by program and property type; many 1–4 unit rentals cap at 75%, with lower caps for some multifamily, mixed-use, and short-term rental deals |

| DSCR estimate | Gross monthly rent ÷ projected new PITIA; target 1.20x+ for best terms |

| Credit score | 620–640 minimum; 720+ to 760+ for the best pricing tiers |

| Liquid reserves | 6–12 months of PITIA, depending on the program |

| Seasoning | 6–12 months of ownership before the lender uses appraised value from the current valuation |

| Planned use for the funds | Documented business-purpose use |

| Entity documents | LLC Articles of Organization, Operating Agreement, and EIN letter if closing in a business name |

Before you apply, run a simple two-limit test. Compare property value × 0.75 against the loan amount that keeps the new payment inside your DSCR target. The lower number is the one that matters.

That’s the choke point. If it doesn’t leave enough cash-out to cover the higher rate and closing costs, the deal may not pencil out at current rates.

If the numbers pass the checklist, move on to quote and pre-qualification with a full file. Contact LoanGuys.com and bring your estimated property value, current payoff balance, rent documents, and reserve statements. Complete files move faster.

FAQs

How is DSCR calculated on a cash-out refinance?

DSCR is figured by dividing the property’s gross monthly rental income by the new monthly PITIA payment.

DSCR = Monthly Gross Rent / New Monthly PITIA

Here’s the catch: a cash-out refinance increases the loan balance. And when the loan balance goes up, the monthly payment usually goes up too. That can push the DSCR down.

So when you estimate the ratio, use the numbers that matter now:

- Current rent

- Current taxes

- Current insurance

- The expected new monthly payment

If any of those figures are off, your DSCR estimate can be off too.

How much cash can I actually get at closing?

Start with the property’s appraised value, then apply the maximum LTV. For 1–4 unit investment properties, that cap is usually 70% to 75%.

Here’s the basic math:

Estimated cash-out = (Appraised Value × Max LTV) – Existing Loan Balance – Closing Costs

For example, say the property appraises at $800,000 and you still owe $300,000 on the mortgage. At a 75% LTV, the new loan amount would be $600,000. After subtracting the current loan balance and 2% to 4% in closing costs, you may have about $285,000 available.

One catch: that final number also has to meet the required DSCR.

When does a DSCR cash-out refinance make sense?

A DSCR cash-out refinance makes sense when you want to pull equity from a rental property for portfolio growth, renovations, debt consolidation, or extra business liquidity, all without personal income verification.

It can be a good option when standard financing slows you down, especially if you're dealing with the 10-property limit, hard-to-document income, or LLC titling. In most cases, it works best when the property has 25% to 35% equity and a DSCR of 1.20 or higher.