Investor Cash Flow Mortgage: How to Qualify Based on Rental Income Alone

Yes - you can often qualify for an investor cash flow mortgage using the property's rent instead of your W-2s or tax returns. In most cases, the lender checks one number first: DSCR = monthly rent ÷ monthly PITIA. If the result is around 1.00 or higher, the deal may work; if it is 1.25+, terms are often better.

Here’s the short version:

- The property’s rent leads the file, not your personal income

- PITIA means principal, interest, taxes, insurance, and HOA dues

- Lenders often want:

- DSCR of 1.00+

- Credit score of 620 to 680+

- 20% to 25% down

- 3 to 6 months of reserves

- For rent, lenders usually use:

- a signed lease

- a rent roll

- or an appraisal rent schedule like Form 1007 or Form 1025

- For occupied homes, they often use the lower of:

- lease rent

- appraised market rent

- Many loans close in about 21 to 30 days

- Cash-out deals often cap leverage around 70% to 75% LTV

If I were checking a deal fast, I’d focus on five things: the rent, the PITIA payment, my credit score, my down payment, and my post-closing reserves. That tells me, up front, whether the file has a fair shot or whether I need to bring more cash in to make the ratio work.

How to Qualify for a DSCR loan in 2026

sbb-itb-e7c549b

How Rental Income Qualification Works

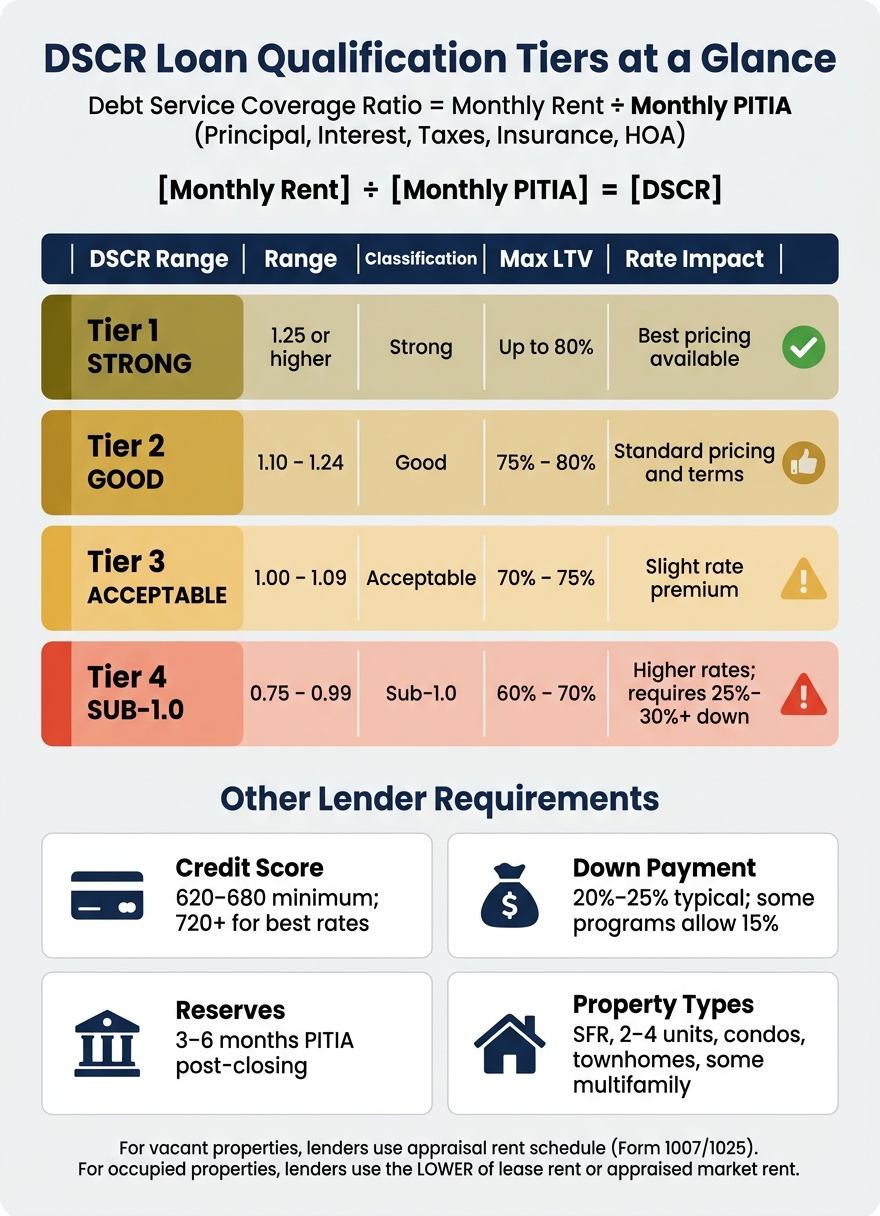

DSCR Loan Qualification Tiers: Ratios, LTV & Rate Impact

With a DSCR loan, the lender looks at the property's rent to qualify the deal, not your personal income.

DSCR Formula and the Minimum Cash Flow Lenders Look For

The formula is simple:

DSCR = Monthly Gross Rental Income ÷ Monthly PITIA

PITIA includes principal, interest, taxes, insurance, and HOA dues.

A DSCR of 1.00 means the rent exactly covers the monthly payment. That's the break-even point and usually the minimum lenders want to see. A ratio of 1.25 or higher is seen as strong and often gets you the best rates and the highest loan-to-value limits.

If the DSCR drops below 1.00, some lenders may still look at no-ratio programs. The catch? Those loans usually come with higher rates. Putting more money down can help, because a smaller loan amount reduces PITIA and improves the ratio.

| DSCR Ratio | Classification | Typical Max LTV | Rate Impact |

|---|---|---|---|

| 1.25+ | Strong | 80% | Best pricing |

| 1.10–1.24 | Good | 75%–80% | Standard pricing and terms |

| 1.00–1.09 | Acceptable | 70%–75% | Slight rate premium |

| 0.75–0.99 | Sub-1.0 | 60%–70% | Higher rates; requires 25%–30%+ down |

After that, the lender needs to confirm how much rent can actually be counted.

How Lenders Determine Qualifying Rent: Leases, Rent Rolls, and Appraisal Schedules

Lenders verify rent with paperwork. That usually means a signed lease agreement, a current rent roll for multi-unit properties, or an appraisal-based market rent schedule.

For single-family rentals, the standard appraisal form is Fannie Mae Form 1007. For 2–4 unit properties, lenders use Form 1025. For occupied properties, underwriters usually use the lower of the lease rent or the appraised market rent. So if a tenant is paying below-market rent, that's the number that can shape the deal. For vacant properties, lenders use the appraisal rent schedule.

Those documents set the qualifying income used in the DSCR calculation.

DSCR Examples for a Purchase and a Refinance

Purchase example - strong cash flow:

A single-family rental in Phoenix, AZ has a proposed PITIA of $2,200/month. The Form 1007 appraisal shows a market rent of $2,800/month.

DSCR = $2,800 ÷ $2,200 = 1.27

That gets above 1.25 and may qualify for top pricing and up to 80% LTV.

Refinance example - tighter cash flow:

An investor refinancing a long-term rental in Atlanta, GA has a current signed lease at $2,100/month. The appraiser's Form 1007 market rent comes in at $2,350/month. Because lenders use the lower of the two, the qualifying income is $2,100/month. The proposed PITIA on the new loan is $2,050/month.

DSCR = $2,100 ÷ $2,050 = 1.02

That usually works, but it often limits LTV to 70%–75% and pushes the rate higher.

Once the rent checks out, lenders still look at credit, equity, reserves, and property type.

Other Approval Standards Lenders Review Beyond Rental Income

A DSCR loan skips W-2s and tax returns. But that doesn't mean the lender stops digging.

Once the DSCR looks good enough, lenders still look at your credit, your cash reserves, and the property itself before they sign off on the loan.

Credit Score, Down Payment, and LTV Limits

Most lenders look for a minimum FICO score somewhere between 620 and 680 for a DSCR loan. If your score is 720 or above, you can usually get the best rates and the highest leverage. First-time investors often face a tougher bar, with many lenders looking for a FICO closer to 700.

For purchases, expect to put down 20% to 25%, which works out to 75% to 80% LTV. Some programs go as low as 15% down or 85% LTV, but those deals usually go to borrowers with strong credit and a DSCR of 1.25 or higher.

Put simply: credit affects your rate and how much you can borrow. Reserves show the lender you can keep making payments after closing.

Reserve Requirements and Cash to Close

Most lenders want to see 3 to 6 months of PITIA in liquid reserves after closing. For jumbo loans or larger portfolios, that often jumps to 6 to 12 months. Retirement accounts may count too, though lenders often discount their value.

Gift funds usually don't work for the down payment on most DSCR programs. And in many cases, your money needs to sit in the account for 30 to 60 days before it can be used.

You'll also want to budget for cash needed at closing, including:

- 2% to 5% of the loan amount for closing costs

- $400 to $1,000 for a full appraisal with a rent schedule, depending on the property type

That means your cash to close is often more than just the down payment. It's the down payment, plus reserves, plus fees.

Eligible Property Types and Program Options

DSCR loans work with a pretty broad mix of investment properties. Most programs cover single-family rentals, 2–4 unit properties, condos that meet lender rules, and townhomes. Some lenders also allow 5–8 unit small multifamily and mixed-use properties, as long as the property is still mostly residential.

Short-term rentals are allowed under many programs, but there's usually a tradeoff: higher rates. Lenders also often apply a 20% reduction to short-term rental gross income before they calculate DSCR.

A few other investor loan programs and features also come up a lot:

- LLC vesting is allowed by many lenders and is often preferred because it helps separate personal and business finances.

- Interest-only options are available on many DSCR loans, usually with a 0.25% rate premium.

If the property checks the right boxes, the file usually moves on to reserve and document review.

Documents You Need and How the Underwriting Process Works

Once the rent math checks out, the file moves into documentation and underwriting. A DSCR loan calls for less income paperwork than a conventional mortgage, but lenders still need proof of rent, reserves, credit, and property eligibility. In plain English, they want to confirm the rent, your cash on hand, and that the property can be insured.

Documents to Prepare for a DSCR Loan File

You’ll usually need four groups of documents: identity, property, income, and assets.

- Identity and credit: A government-issued photo ID or passport, plus authorization for a tri-merge credit report.

- Property: An executed purchase contract for a purchase, or a current mortgage statement for a refinance, along with a property insurance binder or quote.

- Income: For an occupied property, use a signed lease. For a multi-unit property, include a current rent roll. For a vacant property, include the appraisal rent schedule used to support qualifying rent.

- Assets: Provide 2–6 months of bank statements for down payment funds and reserves. Those funds must be seasoned in your account for at least 60 days before closing.

If you’re vesting the property in an LLC, lenders also want the Articles of Organization, Operating Agreement, EIN letter from the IRS, and a Certificate of Good Standing. If the LLC isn’t formed before you apply, closing can slip by 7–14 days.

For short-term rentals, lenders usually ask for a trailing 12-month payout history from the platform or an STR revenue analysis report instead of a signed lease.

Having this paperwork lined up early can make underwriting move with fewer conditions.

From Initial Review to Closing: What the Process Looks Like

After the lender receives the file, the process usually looks like this:

| Phase | Typical Timeline | What Happens |

|---|---|---|

| Initial Review | 24–48 hours | Soft credit pull, preliminary DSCR calculation, and rate quote based on estimated rent |

| Application | After prequalification | Submission of ID, bank statements, purchase contract, and entity documents |

| Appraisal & Rent Survey | 7–10 days | Lender orders a full appraisal with Form 1007/1025 |

| Underwriting | 7–14 days | DSCR confirmed, title commitment reviewed, reserves verified |

| Conditions | Varies | Insurance binder, updated bank statements, and any final items |

| Closing | 21–30 days | Clear to close issued; funds are wired and the deed transfers to the LLC |

Most DSCR loans close in 21 to 30 days, which is about half the time of a conventional investment mortgage. Some well-prepared files close in as little as 14 to 15 days. One thing matters a lot here: fast replies help keep underwriting on track.

Underwriting will compare the lease rent with the appraised market rent and use the lower figure.

When an Investor Cash Flow Mortgage Fits Your Goals

Using This Loan to Buy, Rate-and-Term Refinance, or Cash-Out Refinance

Once you understand the rent math and the main underwriting rules, the next step is simple: decide whether this loan lines up with your investing plan.

You can use this loan to buy, refinance, or pull cash from a rental property without relying on personal income. For a purchase, approval is driven by the property's projected rent. For a rate-and-term refinance, the aim is usually to get a better rate or better loan terms on an occupied rental with steady rent. For a cash-out refinance, lenders often want to see at least 6 months of ownership before using the updated appraised value, and loan-to-value is often capped at 70%–75%. Many investors use a DSCR cash-out refinance to pull capital back out and help pay for the next deal.

That said, the deal still has to work on paper. Approval usually comes down to cash flow, credit, leverage, and reserves.

Key Checkpoints Before You Apply

Before you apply, run your numbers first and check the lender's exact rules. Small details can change the outcome.

- Estimate your DSCR. Aim for a DSCR of 1.20 to 1.25 or higher.

- Confirm rent. Find out whether the lender will use lease rent or appraised market rent.

- Check your credit score. A score of 720+ often gets the best pricing.

- Verify your cash to close. Make sure your down payment, reserves, and closing funds are lined up before you apply.

- Confirm property eligibility. Check that your property type fits the program.

FAQs

What if my DSCR is below 1.00?

A DSCR below 1.00 means the property’s rental income doesn’t fully cover the monthly mortgage payment, including taxes, insurance, and HOA dues.

Some lenders may go as low as 0.75. But getting approved at that level usually means tougher terms, like stronger credit, a lower LTV, higher rates, or larger reserves.

If you want to improve your odds, a few moves can help:

- Increase your down payment

- Lower the property’s costs

- Add more reserves

Can I qualify with a vacant rental property?

Yes. You can qualify for an investor cash flow mortgage even if the property is vacant.

Instead of using your personal income, lenders look at a professional appraisal to estimate market rent. A licensed appraiser completes a 1007 Rent Schedule. If that rent meets the lender’s DSCR requirement, the property can qualify.

Do I need the property in an LLC to apply?

No. You can apply whether the property is in your own name or held in an LLC, corporation, or trust.

If you use an entity, you’ll need to provide the required entity documents. Either way, underwriting stays focused on the property’s rental income, not your personal finances.