Bank Statement Loans for Real Estate Investors: How They Work

If your tax return makes your income look too low, a bank statement loan may help you qualify.

I’d sum it up like this: lenders look at 12 to 24 months of bank deposits instead of tax returns, then use those deposits to estimate monthly income. For many self-employed investors, 1099 earners, LLC owners, and short-term rental hosts, that can make the difference between a denial and a loan approval.

Here’s the short version:

- Best fit: investors whose deposits look stronger than their reported income

- Income method: lender reviews personal or business bank statements

- Common expense cut on business accounts: about 50%, unless a CPA supports a lower ratio

- Credit score floor: often around 620

- DTI cap: often up to 50%

- Down payment: usually 20% to 25% for investment properties

- Reserves: often 3 to 12 months

- Rate range: often about 0.5% to 1.5% above conventional loans

- Close time: about 14 to 21 business days for clean files, but some take 35+ days

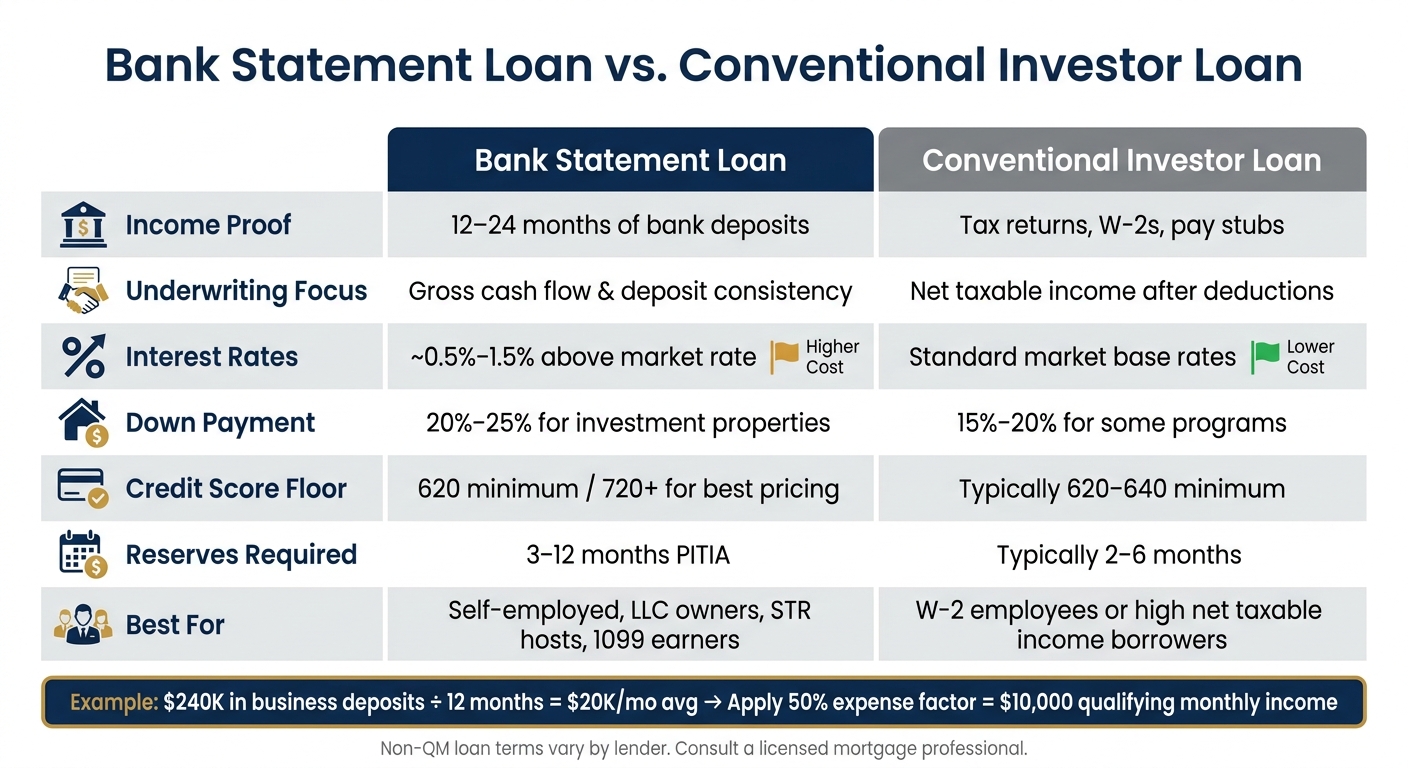

A simple example: if a business account shows $240,000 in eligible deposits over 12 months, that averages $20,000 per month. If the lender applies a 50% expense factor, they may count $10,000 monthly income.

That said, I wouldn’t treat this as the low-cost option. You usually pay more in rate, bring more cash to closing, and deal with tighter deposit review. But if write-offs and depreciation are hurting your borrowing power, this loan type can still make sense.

Quick comparison:

| Item | Bank Statement Loan | Conventional Investor Loan |

|---|---|---|

| Income proof | 12–24 months of deposits | Tax returns, W-2s, pay stubs |

| Main focus | Cash flow into accounts | Taxable income after deductions |

| Down payment | 20%–25% | Often 15%–20% |

| Rates | Usually higher | Usually lower |

| Best for | Self-employed and 1099 investors | Borrowers with strong reported income |

If I were getting ready to apply, I’d start by averaging my last 12 to 24 months of deposits, checking cash reserves, and pulling every page of my statements before sending the file in.

Bank Statement Loan vs. Conventional Investor Loan: Key Differences

Bank Statement Loans Explained: The Real Numbers Behind The Approval.

sbb-itb-e7c549b

What a Bank Statement Loan Is and How It Works

Here’s how lenders turn bank deposits into qualifying income.

A bank statement loan is a non-qualified mortgage (non-QM) that verifies income using 12 to 24 months of bank deposit history instead of tax returns, W-2s, or pay stubs. For investors with strong deposits but low taxable income, this can open doors that a conventional loan may shut. That’s the main underwriting difference.

How Lenders Calculate Income From Bank Deposits

The process starts with full bank statements for the review period. Lenders add up eligible deposits, such as rent, checks, wire deposits, and direct client transfers. Then they remove deposits that don’t show steady business income, like transfers between your own accounts, loan proceeds, and other one-time deposits.

Personal and business accounts are reviewed in different ways. With personal statements, lenders will often count 100% of eligible deposits as qualifying income. With business statements, they apply an expense factor to reflect operating costs. In many cases, that default factor is 50%, but a CPA-certified ratio can come in lower, which means more income may count.

Here’s what that looks like with a business account:

| Step | Description | Example |

|---|---|---|

| 1 | Total 12 months of eligible deposits | $240,000 |

| 2 | Calculate average monthly deposit | $20,000 |

| 3 | Apply 50% default expense factor | $10,000 (expenses) |

| 4 | Monthly qualifying income | $10,000 |

A lower expense factor can make a big difference. If less of the deposit total is treated as business expense, more of it stays in the income calculation.

Once the lender sets qualifying income, the next step is checking whether the borrower meets reserve and down payment rules.

How Bank Statement Loans Differ From Conventional Investor Financing

Conventional lenders look at taxable income after deductions. That number can shrink fast because of depreciation and business write-offs. A bank statement loan looks at gross cash flow instead.

| Feature | Bank Statement Loan | Conventional Investor Loan |

|---|---|---|

| Income Documentation | 12–24 months of bank deposits | 2 years of tax returns, W-2s, pay stubs |

| Underwriting Focus | Gross cash flow and deposit consistency | Net taxable income after deductions |

| Flexibility | High; ignores write-offs and depreciation | Low; strictly follows IRS-reported income |

| Interest Rates | Approx. 0.5%–1.0% higher | Market base rates |

| Down Payment | Typically 20%–25% for investors | As low as 15%–20% for some programs |

| Common Borrower | Self-employed, LLC owners, STR operators | W-2 employees or high-net-income earners |

That price gap matters. But for investors whose deposits show more income than their tax returns, paying about 0.5% to 1.0% more in interest can still make sense.

Those investor loan programs shape what lenders want to see next: cash flow, reserves, and loan-ready paperwork.

Who These Loans Fit and What Investors Need to Qualify

Bank statement loans are a fit for borrowers whose bank deposits show more income than their tax returns. That’s often the case for self-employed investors and business owners who take heavy write-offs. After that, lenders look at your deposit history, credit, reserves, and the type of property you want to finance.

Common Borrower and Cash Flow Requirements

Most lenders want 12 to 24 consecutive months of personal or business bank statements showing steady, traceable deposits. If the statements show gaps, large one-time deposits, or uneven patterns, expect extra questions. Many programs begin at a 620 credit score, while 720 or higher often gets you better pricing and higher loan-to-value options.

DTI still matters here. Most bank statement loan programs cap debt-to-income at 50%. And lenders don’t just glance at deposits - they look closely. Any single deposit that’s more than 50% of your monthly average, or any deposit above $10,000, will usually need to be sourced and documented.

If you clear those hurdles, the next thing lenders focus on is how much cash you’ll need both at closing and after the loan closes.

Down Payment, Reserves, Rates, and Eligible Property Types

For non-owner-occupied properties, investors should expect to put down 20% to 25%, which means a max LTV of 75% to 80%. On top of that, lenders often want 3 to 12 months of reserves to cover principal, interest, taxes, insurance, and HOA dues.

Eligible property types can include:

- Non-owner-occupied single-family rentals

- 2–4 unit properties

- Warrantable and non-warrantable condos

- Townhomes

- Short-term rental properties like Airbnb or VRBO units

Some programs also go well above the loan sizes many investors expect, with limits reaching $3,000,000 to $6,000,000 for qualified borrowers.

Pros and Trade-Offs for Real Estate Investors

The main draw is simple: lenders qualify you based on what’s actually flowing into your accounts, not just what remains after write-offs. For many investors, that can make a big difference.

But there’s no free lunch. That flexibility usually comes with higher rates, more money due at closing, and a more hands-on underwriting process.

| Pros | Trade-offs |

|---|---|

| Qualify without tax returns or W-2s | Interest rates typically 1% to 2% above conventional financing |

| Uses gross deposits, not net taxable income | Down payments often 20% to 25% for investors |

| Flexible for STR hosts, LLC owners, and 1099 earners | Reserves of 3 to 12 months required |

| Access to leverage despite heavy tax write-offs | Manual underwriting and close deposit review |

If your deposits, reserves, and property type line up with the program, the next move is getting your paperwork together for underwriting.

How to Apply for a Bank Statement Loan: Step by Step

Once you know this program works for your cash flow, the next move is simple: build a complete file. That matters because lenders need enough paperwork to turn your deposits into qualifying income. If pieces are missing, underwriting slows down fast.

Documents to Gather Before You Apply

Pull these documents together before you apply. Even one missing page can hold things up.

| Document Type | What to Prepare |

|---|---|

| Bank Statements | 12–24 months of consecutive personal or business bank statements, with every page included |

| Income Verification | A CPA letter supporting business ownership and expense structure |

| Business Documents | Business license, Articles of Incorporation, or LLC documents |

| Asset Statements | 2 months of bank statements showing down payment funds and reserve balances |

| Property Documents | Purchase contract and existing lease agreements for current rentals |

| ID | Government-issued photo ID, such as a driver's license or passport |

If you have large or irregular deposits, be ready to explain them with invoices, contracts, or transfer records.

From Pre-Approval to Closing

The process usually starts with income review, then moves to appraisal, underwriting, and closing. To estimate qualifying income, the lender reviews your deposit history, averages 12–24 months of deposits, and applies an expense factor. If you're using business bank statements, a CPA letter may support a lower expense ratio, which can increase the income figure the lender uses.

Once your documents are in good shape, underwriting can move much faster. After income review, the file goes to property review and final underwriting. For rental properties, the lender may also review a rent schedule to confirm market rent.

At that stage, underwriting may issue a conditional approval and ask for a few follow-ups, such as explanations for overdrafts, NSF activity, or deposits that haven't been sourced. When those conditions are cleared, the loan gets final approval and moves to closing.

Well-prepared files can close in 14 to 21 business days. Files with missing documents can stretch past 35 days, especially when tax returns show less income than the bank deposits suggest.

When a Bank Statement Loan Makes Sense and What to Do Next

If your deposits look stronger than your tax returns, this is the loan to check next. It fits borrowers whose tax returns make their income look lower than the cash flow they actually bring in.

Here’s how that can play out: an LLC investor with $35,000 in AGI qualified for a $500,000 loan by using 24 months of business statements and a 50% expense ratio to show $9,000 in monthly income.

This route can also help when DSCR underwriting doesn’t get you over the line, but your cash flow is still solid. It usually isn’t the lowest-cost choice. Rates tend to run 0.5% to 1.5% above conventional loans. Still, if write-offs are shrinking your borrowing power, that tradeoff may pencil out.

If the numbers line up, the next move is getting your file in order. Start by averaging 12 to 24 months of deposits and pulling together complete statements. Then make sure you have:

- A 15% to 25% down payment ready

- Enough liquid reserves after closing

- A CPA letter if you’re using business accounts

Once that’s done, gather your statements, verify your reserves, and submit a complete non-QM loan file.

FAQs

Can I use personal and business bank statements together?

Yes. Some lenders let you use both personal and business bank statements. It usually depends on your business setup and how money moves through your accounts.

Business accounts are often underwritten with an expense ratio based on gross deposits. A common default is 50%, unless a CPA certifies a lower amount. Personal account deposits, on the other hand, are often counted at 100%.

The right mix comes down to one thing: which accounts give the clearest picture of your qualifying income.

What deposits usually don’t count as income?

Lenders who use bank statements focus on recurring deposits linked to your business or line of work. If money shows up in the account but doesn’t reflect regular business income, it usually won’t count.

That often includes:

- Transfers between your own accounts

- Loan proceeds

- One-time large deposits not tied to regular business activity

- Large irregular deposits that are not sourced or documented

Is a bank statement loan better than a DSCR loan for me?

It comes down to where your finances look strongest.

A bank statement loan often makes more sense if you're self-employed and have steady cash flow that doesn't show up well on your tax returns. Instead of leaning on W-2s or tax forms, the lender looks at personal or business bank deposits to verify income.

A DSCR loan is often a better fit for investment properties because it leans on the property's rental income rather than your personal finances. Go with a bank statement loan if you need funding for a primary residence, or if the property's rental income doesn't stand on its own.