Buying Down Your Mortgage Rate: How Points and Buydowns Work for Investors

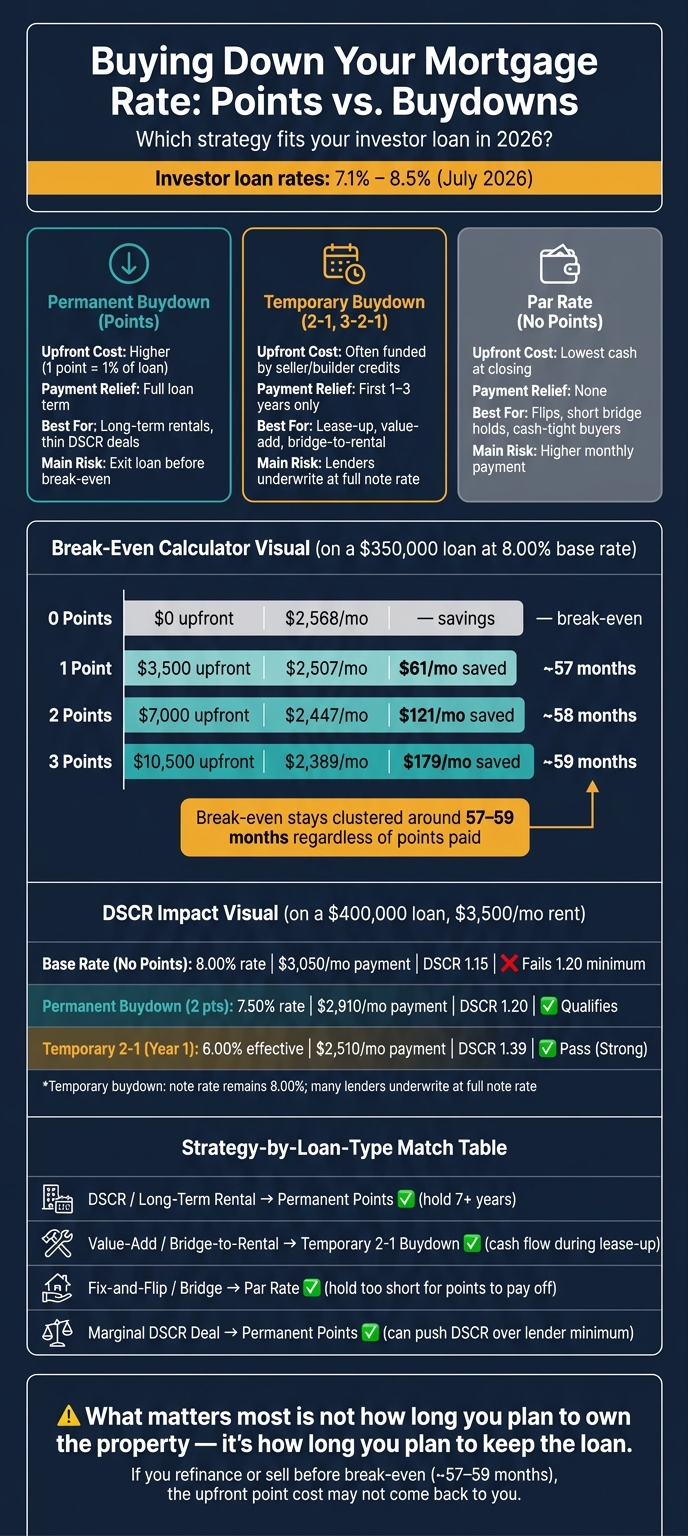

If you won’t keep the loan long enough, paying points usually doesn’t pay off. For many investor loans in July 2026, rates are around 7.1% to 8.5%, so even a 0.25% to 0.50% rate cut can change monthly cash flow, DSCR, and loan approval odds.

Here’s the short version:

- Discount points are an upfront closing cost used to lower the note rate for the full loan term.

- Temporary buydowns lower the payment for the first 1 to 3 years, but the note rate stays the same.

- A point usually costs 1% of the loan amount. On a $350,000 loan, that’s $3,500.

- On a $400,000 loan, a 0.50% rate drop can save about $130 to $138 per month in principal and interest.

- Many permanent point setups hit break-even in about 57 to 59 months.

- For DSCR loans, a lower payment can push a file from not approved to approved.

- For flips and short bridge loans, paying points often makes little sense because the loan ends too soon.

- For long-term rentals, points can work if you expect to keep the loan past break-even.

- For lease-up or rehab deals, a 2-1 buydown may help more because it cuts early payments when cash flow is tight.

What matters most is not how long you plan to own the property. It’s how long you plan to keep the loan. If you refinance or sell before break-even, the upfront cost may not come back to you.

Mortgage Buydown Options for Real Estate Investors: Points vs. Buydowns Compared

Mortgage Points Explained: How and When to Buy Down Your Mortgage Rate

Quick Comparison

| Option | Upfront Cost | Payment Relief | Best Fit | Main Risk |

|---|---|---|---|---|

| Permanent buydown (points) | Higher | Full loan term | Long-term rentals, thin DSCR deals | You exit the loan before break-even |

| Temporary buydown (1-0, 2-1, 3-2-1) | Funded upfront, often with credits | First 1 to 3 years | Lease-up, value-add, bridge-to-rental | Many lenders still underwrite at full note rate |

| Par rate | Lower cash at closing | None | Flips, short bridge holds, cash-tight buyers | Higher monthly payment |

I’d look at this one way: Are the points buying lower payments, better DSCR, loan approval, or none of the above? If the answer is none, keeping the cash may be the better move.

How Points and Buydowns Work on Investor Loans

Before you run the math, get the terms straight.

The note rate is the interest rate written into your loan agreement. That's the full rate you're on the hook for. Discount points are prepaid interest paid at closing to bring that rate down. One point equals 1% of the loan amount. You'll also hear rates discussed in basis points (bps). Here, 100 bps equals 1%, so a 0.25% rate cut is 25 basis points.

That matters because the best setup depends on how long you plan to keep the loan, what you need from monthly cash flow, and how you expect to exit the deal.

A point will often buy about 0.125% to 0.50% of rate reduction, though that changes by lender, loan type, and market. Once those terms are clear, the next choice is simple: pay more upfront for a lower rate over the full term, or use a setup that trims payments for the first few years.

Permanent Buydowns: Paying Points to Lower Your Rate for the Life of the Loan

A permanent buydown means you pay discount points at closing and get a lower note rate for the entire loan term. That lower rate cuts your principal-and-interest (P&I) payment from the start and stays in place for the life of the loan - 30 years, if that's your term.

The tradeoff is pretty straightforward: more cash due upfront in exchange for a lower monthly payment for as long as you keep the loan.

Temporary Buydowns: How 2-1 and 3-2-1 Structures Work

Temporary buydowns reduce early payments without changing the note rate itself. Instead, an upfront subsidy is placed in escrow and used to cover part of the payment during the first 1 to 3 years.

Here’s how the most common setups step down over time:

| Buydown Type | Year 1 Rate | Year 2 Rate | Year 3 Rate | Year 4+ Rate |

|---|---|---|---|---|

| 1-0 Buydown | Note Rate - 1% | Full Note Rate | Full Note Rate | Full Note Rate |

| 2-1 Buydown | Note Rate - 2% | Note Rate - 1% | Full Note Rate | Full Note Rate |

| 3-2-1 Buydown | Note Rate - 3% | Note Rate - 2% | Note Rate - 1% | Full Note Rate |

Most lenders qualify borrowers at the full note rate, not the lower early payment. And if you sell or refinance before the buydown period ends, any unused subsidy usually gets credited to the payoff.

Where Investors Typically See These Options

You'll see both permanent and temporary buydowns across the main investor loan categories.

DSCR rental loans are often a fit for permanent points. Non-QM mortgages may offer similar point setups. Permanent points usually don't make much sense on flips or bridge loans because the hold period is too short. Temporary buydowns tend to line up better with short-term projects, while permanent points are often a better match for long-term rentals.

That choice leads straight into the break-even math.

sbb-itb-e7c549b

Upfront Cost, Monthly Savings, and Break-Even: How to Run the Numbers

How to Calculate Your Break-Even on Discount Points

To find your break-even, divide the upfront cost of the points by your monthly payment savings. That gives you the number of months it takes to earn that money back.

Here’s the part many people miss: break-even should be measured against how long you expect to keep this loan, not how long you plan to own the property. That distinction matters. You might hold the property for 10 years and still refinance or sell the loan out of your life much sooner.

On a $350,000 loan at 8.00%, one point costs $3,500 and lowers the rate to 7.75%, which cuts the payment by about $61 per month. That puts the simple break-even at about 57 months, or a little under five years. Pay two points ($7,000), save $121 per month, and the break-even is almost the same at 58 months.

| Points Paid | Upfront Cost | New Rate | Monthly P&I | Monthly Savings | Simple Break-Even |

|---|---|---|---|---|---|

| 0 Points | $0 | 8.00% | $2,568 | - | - |

| 1 Point | $3,500 | 7.75% | $2,507 | $61 | ~57 months |

| 2 Points | $7,000 | 7.50% | $2,447 | $121 | ~58 months |

| 3 Points | $10,500 | 7.25% | $2,389 | $179 | ~59 months |

Monthly P&I figures are approximate and based on a 30-year fixed term.

That pattern tells you something useful: paying more points does not always mean a much better payback period. In this example, the break-even stays clustered around the same range.

Judge break-even against the time you expect to keep this loan, not the time you expect to own the property. If you refinance before reaching break-even, you won’t earn those points back.

Permanent vs. Temporary Buydowns: A Side-by-Side Comparison

Permanent points cut the payment for the full life of the loan. Temporary buydowns cut it only in the early years, and then the payment steps up to the full note rate.

So this isn’t about one option being better across the board. It’s about fit. One helps if you plan to stay in the loan for a long stretch. The other helps if you want short-term payment relief at the start.

| Feature | Permanent Buydown | Temporary Buydown (2-1 Structure) |

|---|---|---|

| Upfront Cost | Paid by borrower, seller, or builder at closing | Often funded by seller or builder credits |

| Rate Reduction Period | Life of the loan | First 2 years only |

| Monthly Payment Impact | Consistent, moderate reduction | Significant short-term relief; steps up annually |

| Total Interest Effect | Reduces total interest over 30 years | No effect on total interest at the note rate |

| Break-Even Logic | Must keep the loan in place long enough to benefit | Usually seller-funded; no investor break-even |

| Best-Fit Use Case | Long-term buy-and-hold (7+ years) | Value-add, stabilization, or expected near-term refinance |

One more thing to keep in mind: the first point usually gives the biggest rate drop for each dollar spent. After that, the payoff often starts to weaken.

How Lower Payments Affect Cash Flow and Returns

Lower monthly payments don’t just make a spreadsheet look better. They give you more room to operate.

On a $350,000 rental, saving $61 to $121 per month adds $732 to $1,452 per year back into cash flow. That can help cover repairs, build reserves, or give you a little more cushion on debt service.

But there’s a tradeoff. Paying $3,500 to $7,000 at closing ties up cash you might want for your next purchase, a rehab budget, or plain old reserves. For investors trying to grow a portfolio, keeping cash available often matters more than shaving a bit off the monthly payment.

And sometimes the math isn’t just about savings. If the lower payment pushes DSCR above a lender’s minimum, points can help get the deal approved in the first place. In that case, the cash-flow gain matters even more because it also helps with loan qualification.

How Buydowns Affect DSCR, Loan Qualification, and Deal Strategy

How a Lower Payment Can Improve Your DSCR

Once you know how much the payment drops, the next step is underwriting.

What matters here is simple: does the lower payment lift DSCR enough to change the deal? DSCR is monthly rent divided by monthly debt service. So when debt service falls, DSCR moves up.

On a $400,000 loan with $3,500 in monthly rent, that shift can be the whole story. At 8.00%, the estimated monthly principal, interest, taxes, insurance, and HOA dues comes in at about $3,050. That puts DSCR at roughly 1.15, which falls short of a common 1.20 minimum. Pay two points to lower the rate to 7.50%, and the payment drops to about $2,910. That pushes DSCR to 1.20 and gets the loan over the line.

That’s the lens to use: are the points buying approval, better pricing, or nothing at all?

| Scenario | Interest Rate | Monthly Payment (Est.) | DSCR | Qualification Status |

|---|---|---|---|---|

| Base Rate (No Points) | 8.00% | $3,050 | 1.15 | Fails 1.20 minimum |

| Permanent Buydown (2 Pts) | 7.50% | $2,910 | 1.20 | Qualifies |

| Temporary 2-1 (Year 1) | 6.00%* | $2,510 | 1.39 | Pass (Strong) |

*Effective rate for payment calculation only; the note rate remains 8.00%. Many lenders still underwrite temporary buydowns at the full note rate, so the lower payment may not help qualification.

If points are what move a file from “does not qualify” to “approved,” then you’re not just buying a lower rate. You’re buying loan eligibility. In some cases, moving into a higher DSCR tier can also lead to a lower base rate or lower reserve needs.

Which Buydown Option Fits Your Strategy: Rental, Fix-and-Flip, or Bridge-to-Rental

The best buydown depends on how long you plan to keep the loan.

For long-term rental investors with stabilized properties and no near-term refinance plan, permanent points are the clearest fit. The lower payment stays in place for the full loan term, and the DSCR lift stays with it. That only works, though, if the loan will remain in place long enough for the savings to matter.

For value-add and bridge-to-rental deals, a temporary buydown often lines up better. If you’re renovating, leasing units, or waiting for rents to settle in, the first year or two is usually the tightest stretch for cash flow. That’s exactly where a 2-1 buydown helps most. By the time the payment steps up, rents should be in a better spot to carry the full amount. A 2-1 buydown on a $600,000 loan can reduce the monthly payment by more than $700 in the first year. That gives you more breathing room while the property stabilizes.

Fix-and-flip investors usually should pass on permanent points. The hold period is just too short to justify the upfront cost.

When Buying Down the Rate Does Not Make Sense

If your planned hold is shorter than the break-even point, permanent points usually don’t work. If you expect to refinance or sell within 24 to 36 months, you likely won’t recover the upfront cost before you exit.

Liquidity matters just as much. Paying $8,000 in points to save $138 per month may look fine in a spreadsheet, but it’s a different story if that cash leaves you thin on reserves or slows down your next purchase. For investors trying to grow a portfolio, that same $8,000 may do more work in another deal than it will in monthly interest savings.

The choice usually comes back to a short checklist:

- How long you plan to hold the loan

- When the points break even

- How much cash you need to keep in reserves

Applying This Framework to LoanGuys.com Financing Options

Evaluating Points and Buydowns Across DSCR, Non-QM, Bridge, and Rental Loans

Now that the math is clear, the next step is simple: figure out which LoanGuys.com loan type actually makes sense for points.

On DSCR and non-QM loans that are underwritten based on cash flow and credit, points can do more than trim the rate. In some cases, they can help a borrower qualify in the first place.

For DSCR and long-term rental loans, permanent points are usually the best match. The lower payment stays with the loan for its full term, and the DSCR gain stays in place too. If a property is sitting just under the lender’s minimum DSCR, points may help the deal cross the line and become eligible, not just cut interest costs.

For bridge and fix-and-flip loans, that logic usually falls apart. These loans are short-term by nature, so permanent points often don’t have enough time to pay for themselves before the exit. In most cases, it makes more sense to keep that cash available for reserves and rehab.

Bridge-to-rental and value-add deals land somewhere in between. That’s where a temporary 2-1 buydown can make sense. It can lower the payment during renovation and lease-up, then step up to the full note rate once the property is producing income and ready for permanent financing.

One detail matters more than people think: check how much rate relief each point actually buys. If the pricing is weak, staying at par is often the better move.

Key Takeaways Before You Choose Points or a Buydown

This table lines up each loan type with the buydown approach that tends to fit best.

| Loan Type | Buydown Fit | Reason |

|---|---|---|

| DSCR / Long-Term Rental | Permanent points | Best for long-term holds where the payment reduction lasts for the life of the loan. |

| Value-Add / Bridge-to-Rental | Temporary 2-1 | Helps cash flow during renovation and lease-up before refinance. |

| Fix-and-Flip / Bridge | Par rate | The hold period is usually too short to recover point costs. |

| Marginal DSCR Deal | Permanent points | Can help the loan meet the lender's DSCR threshold. |

If points move a deal from a 1.18 DSCR to 1.24 and get the loan funded, they may still make sense even if the plain break-even period looks longer on paper. That’s why it pays to run the numbers before you get to the closing table.

FAQs

How do I know if points are worth it?

Calculate the break-even period by dividing the upfront cost of the points by the monthly payment savings. That gives you the point where the money you paid at closing is matched by what you save each month. If you expect to sell the home or refinance before then, paying for points will likely mean a net loss.

It also helps to look at your loan hold time, opportunity cost, and the way returns taper off. In many cases, points take 5 to 7 years to pay for themselves, and the first point often gives the biggest drop in rate.

Will a buydown help me qualify for a DSCR loan?

Yes. A permanent rate buydown can help you qualify for a DSCR loan because it lowers your monthly mortgage payment. And when that payment goes down, your Debt Service Coverage Ratio can look better too.

That said, the fine print matters. Ask your lender how they handle qualification. A permanent buydown paid through discount points is often accepted for qualifying, while a temporary buydown may still be underwritten using the higher long-term note rate.

Should I choose points or a temporary buydown?

Choose points if you expect to keep the loan past the break-even point and want a lower payment for the long haul.

For many investors, a temporary buydown is mostly about near-term cash flow. The catch? It can lose value if you refinance or sell too soon. Points tend to make more sense when you’re set on a longer hold - often 7+ years, and even more so at 15+ years - and still have enough cash left after closing.