DSCR Loan Prepayment Penalties: Buyout Options, Step-Downs, and How to Avoid Them

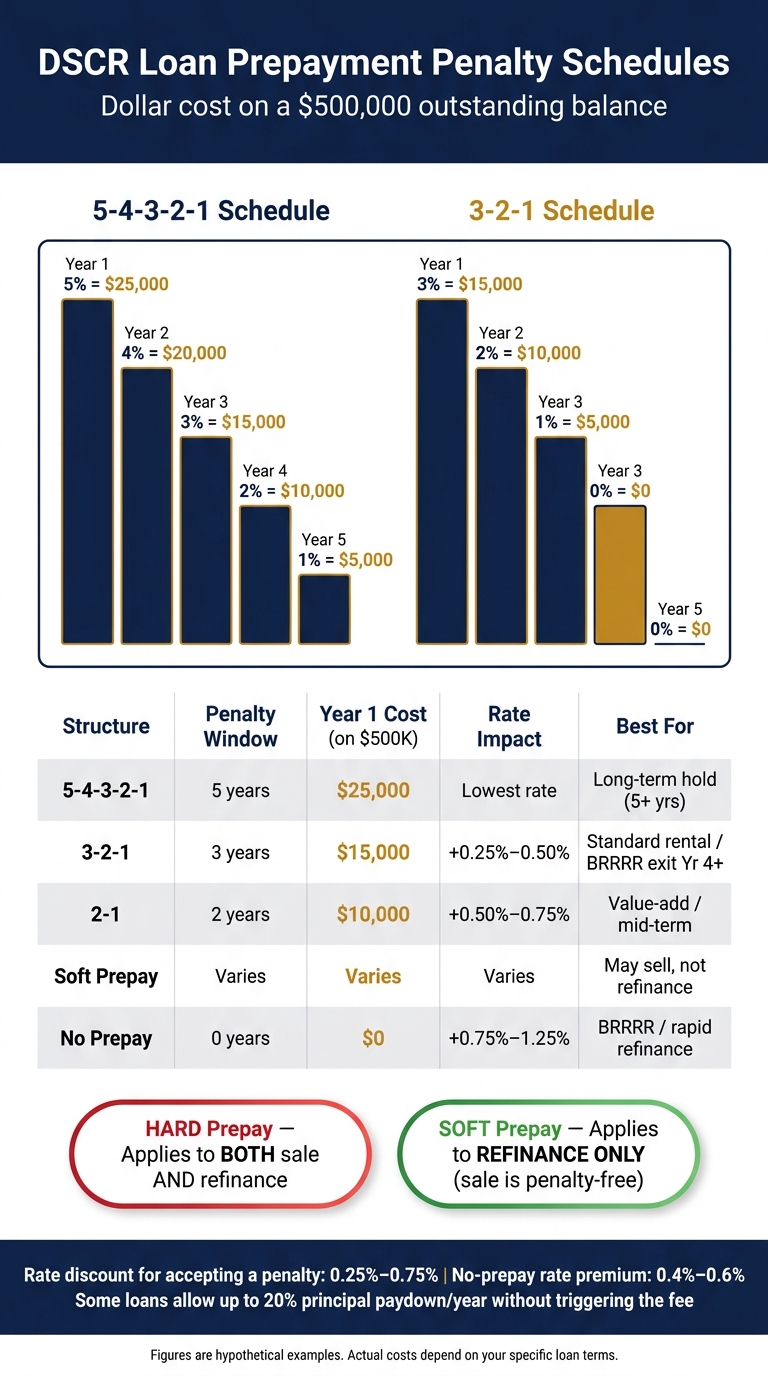

A low DSCR rate can cost you more if you exit early. On a $500,000 loan, a 5-4-3-2-1 prepayment penalty can cost $25,000 in Year 1 and $15,000 in Year 3.

If I were reviewing a DSCR loan, I’d look at one thing first: when I plan to sell or refinance. That’s because the rate discount on a loan with a penalty may be only 0.25% to 0.75%, while the early payoff fee can be 3% to 5% of the unpaid balance. If I expect to exit in 12 to 24 months, I’d price a 3-2-1, 2-1, soft prepay, or no-penalty option before locking the loan.

Here’s the short version:

- Prepayment penalties apply when you sell, refinance, or pay off too much principal early

- Hard prepay usually applies to both a sale and a refinance

- Soft prepay usually applies only to a refinance

- Many DSCR loans use 5-4-3-2-1 or 3-2-1 step-down schedules

- Some notes calculate the fee on the unpaid balance, while others use the original loan amount

- A buyout means paying more up front, or taking a higher rate, to cut or remove the penalty

- A no-prepay option often comes with a rate premium of about 0.4% to 0.6%

- Some loans allow up to 20% principal paydown per year without triggering the fee

DSCR Prepay Penalties | Hard vs Step-Down (What You're Actually Paying)

sbb-itb-e7c549b

Quick comparison

| Option | Penalty window | Year 1 cost on $500,000 | Rate trade-off | Best for |

|---|---|---|---|---|

| 5-4-3-2-1 | 5 years | $25,000 | Lowest rate | Long hold |

| 3-2-1 | 3 years | $15,000 | Slightly higher rate | Hold 3+ years |

| 2-1 | 2 years | $10,000 | Higher rate | Shorter hold |

| Soft prepay | Varies | Depends on note | Varies | May sell, not refinance |

| No prepay | 0 years | $0 | Highest rate/points | BRRRR or early refi |

Bottom line: I wouldn’t judge a DSCR loan by rate alone. I’d match the prepay terms to my exit plan, compare the penalty against any rate savings, and check the note for the exact trigger, formula, and penalty type before closing.

How DSCR prepayment penalties work

A prepayment penalty is a fee you pay if you pay off a DSCR loan before the penalty period ends. In plain English, it’s the lender’s way of protecting its return when a loan gets paid off early.

That can happen in a few different ways:

- You sell the property

- You refinance into a new loan

- You pay off the full balance in cash

- You make a principal paydown that goes past the annual principal prepayment limit, often up to 20% of the balance per year

DSCR lenders use this fee because an early payoff cuts short the interest they expected to earn.

Because DSCR loans are non-QM, they don’t follow the same 3-year cap that applies to many standard residential mortgages. That’s why 5-year penalty windows are common. In many cases, agreeing to a prepayment penalty can also reduce your interest rate by 0.25% to 0.75%. That can help monthly cash flow. But if you refinance or sell before the penalty period ends, those savings can vanish fast. Once you understand that trade-off, the next step is looking at how the penalty drops over time and what that looks like in actual dollars.

Common prepayment penalty structures for DSCR loans in the U.S.

The most common setup for DSCR loans is a step-down schedule. The penalty percentage gets smaller each year, which means your payoff cost drops the longer you keep the loan.

Common DSCR step-down schedules include 5-4-3-2-1 and 3-2-1.

| Penalty Type | How It Works | Best Fit |

|---|---|---|

| Step-down (5-4-3-2-1 or 3-2-1) | Percentage decreases annually | Buy-and-hold investors |

| Flat | Fixed percentage for the full penalty window | Longer hold periods with predictable exit costs |

| Yield maintenance | Formula-based payoff cost | Larger commercial-style DSCR loans |

| No penalty | No fee for early payoff | BRRRR strategies or short-term holds |

You can also choose a no-penalty option, but there’s usually a rate premium of 0.4% to 0.6%.

There’s another detail that matters a lot: soft vs. hard prepayment penalties.

A soft penalty applies only if you refinance. If you sell the property, the fee does not apply. A hard penalty applies to both a sale and a refinance.

What triggers the penalty and how the fee amount is calculated

The penalty is usually triggered by a refinance, a sale, paying off the full balance in cash, or making a principal paydown that goes past the annual principal prepayment limit.

Most lenders calculate the fee based on the outstanding balance at payoff. Some loan notes use the original loan amount instead, which can make the fee higher. That’s a big difference, so it’s worth checking the documents line by line.

Look at the Promissory Note, Loan Estimate, and Closing Disclosure for the exact payoff formula. That formula is what sets up the step-down examples that follow.

Step-down schedules and payoff cost examples

DSCR Loan Prepayment Penalty Structures: Cost & Flexibility Compared

5-4-3-2-1 and 3-2-1 schedules with sample calculations

A step-down schedule cuts the penalty by one point each year. So the date you pay off the loan has a direct effect on what you owe.

Here’s how that plays out on a hypothetical $500,000 outstanding balance under two common schedules.

| Year of Payoff | 5-4-3-2-1 Penalty | Dollar Cost | 3-2-1 Penalty | Dollar Cost |

|---|---|---|---|---|

| Year 1 | 5% | $25,000 | 3% | $15,000 |

| Year 2 | 4% | $20,000 | 2% | $10,000 |

| Year 3 | 3% | $15,000 | 1% | $5,000 |

| Year 4 | 2% | $10,000 | 0% | $0 |

| Year 5 | 1% | $5,000 | 0% | $0 |

All figures are hypothetical examples based on a $500,000 outstanding balance. Actual costs depend on your specific loan terms.

On a 5-4-3-2-1 loan, the difference between paying off in Year 1 and Year 4 is $15,000 on that same $500,000 balance. That’s not small. It should be part of any hold-versus-sell calculation.

Here’s another simple example. Say your loan balance has amortized from $300,000 to $290,000 by Year 2. A 4% penalty would cost $11,600 if the fee is based on the current balance, or $12,000 if it’s based on the original amount.

That sliding payoff curve helps explain why some borrowers look at buyout options instead of waiting for the full penalty period to end.

Longer penalties, shorter penalties, and no-prepay options compared

The trade-off here is simple: rate versus flexibility. Shorter penalty periods can lower your exit risk, but they usually come with a higher interest rate.

| Penalty Structure | Years Covered | Typical Rate Impact | Early Payoff Cost Exposure | Best-Fit Strategy |

|---|---|---|---|---|

| 5-4-3-2-1 | 5 years | Lowest (base rate) | Up to 5% of balance in Year 1 | Long-term buy-and-hold (10+ years) |

| 3-2-1 | 3 years | +0.25% to +0.50% | Up to 3% of balance in Year 1 | Standard rental; BRRRR exit in Year 4+ |

| 2-1 | 2 years | +0.50% to +0.75% | Up to 2% of balance in Year 1 | Value-add or mid-term stabilization |

| No-prepay | 0 years | +0.75% to +1.25% | None | Fix-and-flip or rapid refinance |

A 5-4-3-2-1 setup tends to fit borrowers who expect to keep the property for a long time and want the base rate. A 3-2-1 structure gives up a bit on rate, but it can make more sense for a standard rental plan or a BRRRR exit after Year 3. Go even shorter with 2-1, and you get more room to move, though the rate usually climbs again. At the far end, no-prepay removes the penalty but costs more up front through the rate.

If your exit timing isn’t locked in, the next step is to compare buyout terms with the penalty itself.

Buyout options and ways to reduce prepayment costs

What a prepayment penalty buyout means in practice

If the step-down schedule doesn't line up with your planned hold period, price the buyout before you lock the loan.

A buyout means paying more at closing or taking a higher interest rate in exchange for less payoff risk later. Put simply: you spend more now so you have more room to move when it's time to exit. Soft penalties apply only to refinances. Hard penalties apply to both sales and refinances.

When a buyout makes sense for BRRRR, value-add, or short-hold strategies

This matters most when you expect to exit early.

A buyout usually makes sense when your exit is likely to happen during the penalty window. For BRRRR and value-add investors who plan to refinance within 12 to 24 months, a shorter penalty period or a no-prepay option often fits better. Otherwise, the math can turn against you fast.

Here's the problem: if the refinance happens before the penalty expires, the buyout cost may be less than the penalty you'd face. On a $300,000 DSCR loan refinanced in Year 2, a 5-4-3-2-1 structure can trigger a $12,000 penalty. About 24 months of rate savings may offset only around $3,750, which leaves a net exit cost of $8,250.

Long-term buy-and-hold investors are the main exception. If you expect to keep the property for 5 to 10+ years, the penalty may run out before you sell or refinance. In that case, the lower rate may be worth giving up some flexibility upfront.

How to avoid or reduce prepayment penalties

The best way to avoid a penalty is to match the loan to your exit plan before closing. If you're only a few months away from the next step-down anniversary, waiting can cut the fee or wipe it out altogether.

The table below sums up the main paths:

| Strategy | Upfront Cost | Effect on Monthly Cash Flow | Penalty Risk | Best Use Case |

|---|---|---|---|---|

| 5-4-3-2-1 step-down | Lowest | Highest (lowest rate, least flexibility) | High (5 years) | Long-term buy-and-hold (5+ years) |

| 3-2-1 step-down | Moderate | Moderate (higher rate, more flexibility) | Medium (3 years) | Stabilization or rental hold with a 3- to 5-year exit |

| No-prepay structure | Highest (rate/points) | Lowest (highest rate, full flexibility) | None | BRRRR, value-add, or short-hold refinance |

| Soft penalty | Moderate | Moderate | Low (sale is penalty-free) | Investors who may sell but don't plan to refinance |

Build the penalty into your exit pro forma from day one. Add the expected fee before you close, not after the deal is already in motion.

Choosing the right DSCR loan structure with LoanGuys.com

DSCR loans are underwritten on property cash flow and borrower credit. That means the loan structure matters just as much as the rate. Before you close, line up the terms with your planned exit date so you don't get hit with costs you didn't plan for.

What to check before locking a DSCR loan

Here are the terms worth checking before you lock:

- Step-down schedule. Find out whether the loan uses a 5-4-3-2-1, a 3-2-1, or a no-prepay option. Then compare that schedule to how long you expect to hold the property.

- Penalty basis. Check whether the fee is based on the original loan balance or the unpaid principal balance. Original-balance penalties cost more.

- Lockout period. Some notes have a lockout period that blocks payoff completely. That's separate from the step-down schedule.

- Soft vs. hard language. Make sure you know whether the penalty applies to a sale, a refinance, or both.

- No-prepay availability and its cost. Ask for side-by-side quotes for 5-year, 3-year, and no-prepay options. No-prepay loans usually come with a 0.4% to 0.6% rate premium, and that can push monthly debt service high enough to weaken DSCR.

It's also smart to ask whether the loan lets you make extra principal payments without a penalty. Some DSCR loans allow up to 20% of the balance per year without triggering that fee.

Conclusion: The lowest DSCR rate is not always the cheapest way out

Once the note language is clear, run the payoff cost against your expected hold period. A 5-4-3-2-1 penalty on a $500,000 loan costs $25,000 in Year 1 and $15,000 in Year 3. That's a big expense, and you won't see it in a simple rate comparison.

A longer step-down can work if you plan to hold for five years or more. If your timeline is short, a no-prepay option may fit better. Match the loan to the hold period, and your costs are a lot easier to see coming.

FAQs

How do I know if a buyout is worth it?

A buyout makes sense only if the upside from refinancing or selling is bigger than the penalty you’d owe.

Start with the fine print. Look at the penalty type, whether it’s calculated from the payoff balance, and what event sets it off. That part matters more than most people think.

Then run the math on at least two exit dates. Leaving during the higher-penalty years can wipe out your savings fast. Waiting until the penalty period ends - or even gets shorter - can make the buyout look a lot better.

When should I choose soft prepay over hard prepay?

Choose a soft prepayment penalty if you want more room to sell the property without getting hit with a fee. A hard prepayment penalty can apply if you refinance or sell. A soft penalty, on the other hand, usually kicks in only when you refinance early.

That makes a soft penalty a good fit if you may sell the property during the penalty period but don’t expect to refinance.

Can a prepayment penalty hurt my DSCR on a refinance?

Yes. A prepayment penalty can shrink - or wipe out - the money you’d save from refinancing.

Here’s why: this fee is often based on a percentage of your remaining loan balance. In many cases, lenders charge 3% to 5% during the first few years of the loan. That can turn into a big upfront cost fast.

The smart move is to compare that penalty with the savings you expect over time. That gives you your break-even point - the moment when refinancing starts to pay off instead of costing you more.