12-Month Bank Statement Loans: Requirements, Rates, and Who They're For

If your bank deposits look strong but your tax returns look low, a 12-month bank statement loan may help you qualify when a standard mortgage won’t. I’d sum it up this way: these loans use 12 months of bank deposits instead of tax returns, they usually ask for 620 to 660+ credit, 10% to 25% down, 3 to 12 months of reserves, and rates often land around 7% to 10% as of July 10, 2026.

Here’s the short version:

- Best for: self-employed borrowers, freelancers, 1099 workers, consultants, gig workers, and commission earners

- Income method: lenders average eligible deposits from the last 12 straight months

- What gets removed: transfers, cash that can’t be sourced, loan proceeds, and one-time windfalls

- Personal vs. business statements: personal accounts may count 100% of eligible deposits; business accounts often use a 50% expense factor unless a CPA letter supports a lower one

- Credit range: often 620 to 660 minimum, with better pricing at higher scores

- Down payment: often 10% to 20% for a primary home and 20% to 25% for an investment property

- Reserves: often 3 to 12 months of PITIA

- Main tradeoff: easier income qualifying, but higher rates and tighter cash-to-close rules

- Common red flags: overdrafts, NSF activity, missing statement pages, and large deposits without backup

- Better fit than DSCR when: your personal income is the main strength of the file, not the rental property’s cash flow

A few numbers stand out. The article notes that self-employed households earn about 30% more on average than W-2 households, yet mortgage denials can run 25% to 40% higher. That gap is the whole reason these loans exist: the cash flow may be there even when the tax return does not show it well.

| Topic | What to know |

|---|---|

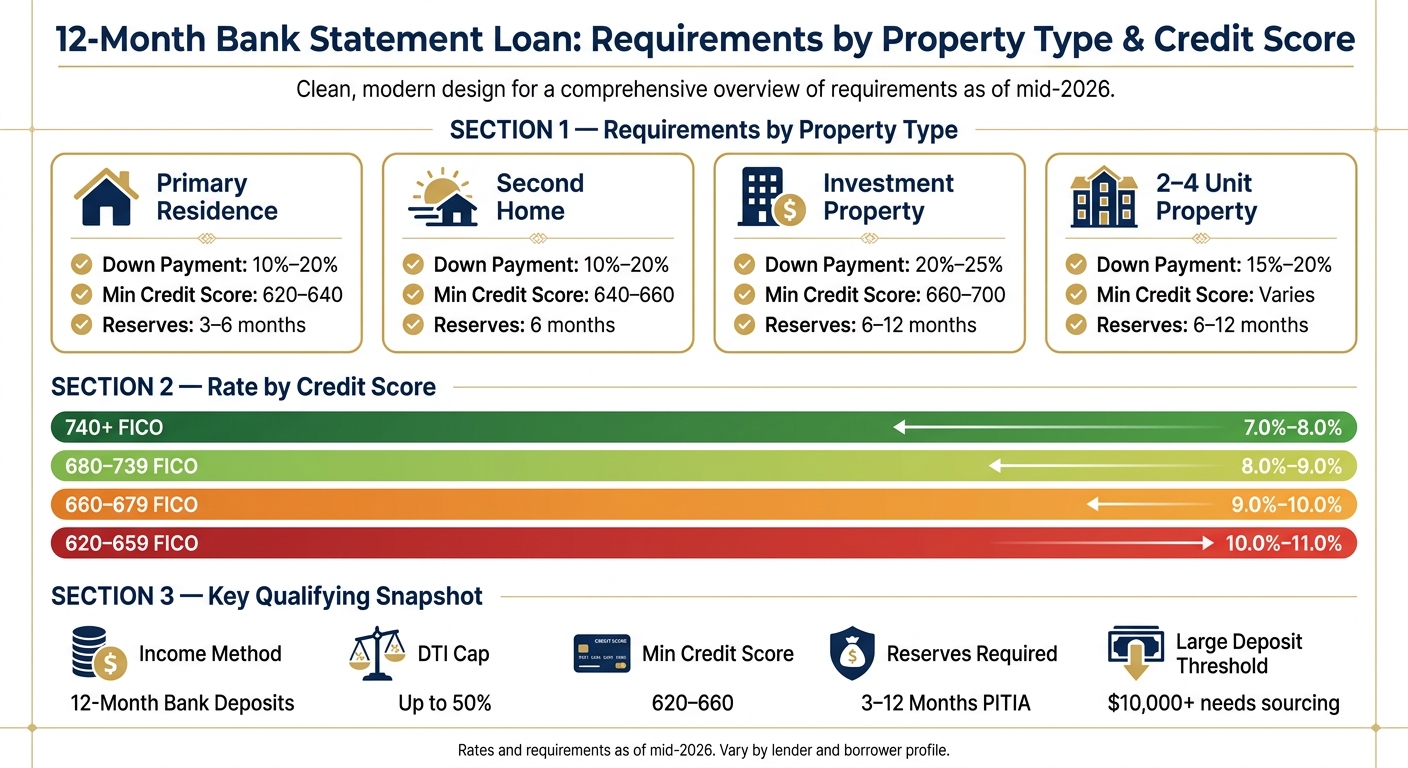

| Income proof | 12 consecutive bank statements, all pages |

| Qualifying income | Eligible deposits averaged over 12 months |

| Rate range | About 7% to 10% |

| DTI cap | Often up to 50% |

| Large deposit review | Often $10,000+ or 50%+ of average monthly deposits |

| Best fit | Borrowers with strong deposits but reduced taxable income |

If I were screening this loan fast, I’d ask three questions: Do your deposits show steady income? Do you have enough for the down payment plus reserves? Is personal income stronger than property cash flow? If the answer is yes, this loan may fit. If not, another program may make more sense.

That’s the core of the article in plain English.

Bank Statement Loans for Self-Employed Borrowers in Texas | Mortgage Mark | Dallas Mortgage Lender

What a 12-Month Bank Statement Loan Is

A 12-month bank statement loan is a Non-QM mortgage that uses bank deposits instead of tax returns to estimate income. It’s built for borrowers whose tax returns show less income than their actual cash flow. That’s the whole point: the loan looks at the money coming in, not just what ends up on a tax form.

These loans can be a good fit when income is strong on paper in your bank account, but write-offs or business deductions make taxable income look lower. Rates, down payment rules, and income math can vary based on your credit profile, property type, and whether the loan is for a primary residence or an investment property.

How Lenders Use 12 Months of Statements to Verify Income

The lender reviews all pages of your last 12 consecutive monthly bank statements. No gaps. No missing pages. They use those statements to estimate income from deposits that count.

Here’s how that usually works:

- They total eligible deposits

- They remove transfers, loan proceeds, windfalls, and unsourced cash

- They divide the final amount by 12

That monthly average becomes your qualifying income.

It sounds simple, but underwriters don’t just look at the total. They also look at the pattern. Overdrafts and NSF events can draw extra attention, so a clean deposit history matters too.

Personal vs. Business Bank Statement Programs

The type of account you use changes the income calculation.

With a personal bank statement program, lenders usually count 100% of eligible deposits as qualifying income. This often works well for sole proprietors or freelancers who deposit earnings into a personal account.

With a business bank statement program, lenders usually apply an expense factor to gross deposits. In many cases, that factor is 50%, unless a CPA letter supports a lower expense ratio.

Same idea, different math.

When Bank Statement Loans Make Sense vs. Property Cash-Flow Programs

A bank statement loan is still an income-based loan. It makes sense when your own earnings are the main strength of the file, like if you’re self-employed, paid on 1099, or running a business with strong cash flow but lower taxable income.

If the deal leans mostly on rental income, a DSCR loan is often the better match. That’s because DSCR loans look at the property’s cash flow, not the borrower’s personal income.

That split affects the credit, reserve, and down payment rules that come next.

Requirements to Qualify

12-Month Bank Statement Loan Requirements by Property Type

Required Documents and Statement Standards

Once the lender figures out which statement type fits your file, the next step is showing income and overall file strength. Since these loans lean on deposit history, underwriters focus on the pattern and quality of cash flow, not just the ending balance.

Lenders want 12 straight months of complete bank statements, with every page included and no missing months. Along with the statements, underwriters usually ask for a government-issued ID, a business license, CPA letter, or similar proof showing at least two years in business, plus proof of liquid reserves such as savings or retirement accounts. Two years in the same line of work is the usual standard, though some programs may look at borrowers with only 12 months of history if they have strong compensating factors.

They also want to see deposits that make sense for your business. If your work is steady, the deposits should look steady too. One-time windfalls, transfers between accounts, and loan proceeds usually don't count as qualifying income.

For business bank statements, lenders often use a default 50% expense factor. If a CPA letter or third-party P&L shows your actual expenses are lower, that can increase your qualifying income. In some cases, the expense ratio can drop to as low as 10% for low-overhead businesses like consulting or tech.

Large deposits get extra attention. Any deposit over $10,000 or more than 50% of average monthly deposits usually needs to be sourced with invoices, wire records, or client contracts. Frequent NSF activity or overdrafts can hurt your chances, while one-off issues usually need a written explanation.

Credit Score, Reserves, and Debt-to-Income Expectations

Most bank statement programs ask for a minimum FICO score from 620 to 660. Some lenders also want 2 to 3 active tradelines, although a strong credit profile can sometimes make up for that. You can still qualify at the lower end of the score range, but better credit usually leads to better pricing and loan terms.

Reserve requirements often land between 3 and 12 months of PITIA in verified liquid reserves after closing. PITIA includes principal, interest, taxes, insurance, and association dues. These reserves are separate from your down payment, which means you need enough cash to close and enough left after closing.

DTI limits on these programs usually go up to 50%, and the calculation is based on averaged bank statement deposits instead of tax-return income.

Down Payment Ranges by Occupancy and Property Type

Occupancy and property type have a big effect on down payment and reserve needs.

| Occupancy / Property Type | Typical Down Payment | Min. Credit Score | Typical Reserves |

|---|---|---|---|

| Primary Residence | 10% – 20% | 620 – 640 | 3 – 6 months |

| Second Home | 10% – 20% | 640 – 660 | 6 months |

| Investment Property | 20% – 25% | 660 – 700 | 6 – 12 months |

| 2–4 Unit Property | 15% – 20% | Varies by lender | 6 – 12 months |

That 10% down option is usually for stronger borrowers, often those with 700+ credit. Investment properties usually need at least 20% down, and that minimum can go up if your credit score is lower or the loan amount is larger. Non-warrantable condos also tend to come with higher down payment needs, higher credit score rules, and more reserves than standard condo terms.

Pricing comes back to the same core pieces: credit, leverage, reserves, and property type.

sbb-itb-e7c549b

Rates, Costs, and What Affects the Price

Typical Rate Ranges and Why They Cost More

Bank statement loans fall into the Non-QM category, which means they don’t follow standard agency rules. Because of that, lenders build in extra risk tied to income review and file complexity. That’s why rates usually come in higher than conventional mortgage rates.

As of mid-2026, bank statement loan rates usually fall between 7% and 10%, based on your credit score, leverage, and overall file strength. In most cases, that puts them about 0.50% to 1.50% above conventional mortgages. Rates can also move from one day to the next as market conditions change and lenders update their programs. After that, the final rate mostly comes down to credit, leverage, reserves, and the property itself.

A 12-month statement program can also cost more than a 24-month option. In many cases, pricing runs 0.25% to 0.50% higher.

The Main Pricing Factors: Credit, LTV, Reserves, and Property Type

The same factors used to qualify you also shape the price. Lenders look at the file as a package. If several risk factors show up at once, the rate usually moves higher.

Credit score is the biggest driver. Borrowers with a 740+ FICO usually get the best pricing available, while borrowers in the 620–659 range tend to see the highest rates. The biggest pricing changes tend to come from credit score alone:

| Credit Score | Estimated Rate |

|---|---|

| 740+ | 7.0% – 8.0% |

| 680 – 739 | 8.0% – 9.0% |

| 660 – 679 | 9.0% – 10.0% |

| 620 – 659 | 10.0% – 11.0% |

LTV matters too. Putting 20% down instead of the 10% minimum can improve pricing by about 0.25% to 0.50%, and a 25% down payment can help even more. Property type also plays a part. Primary residences usually get the best pricing, while investment properties and 2–4 unit homes usually cost more.

If you pick an interest-only payment option, plan on about a 0.25% premium added to the base rate.

Pros and Tradeoffs of 12-Month Bank Statement Loans

The tradeoff here is pretty straightforward: easier income qualification, higher borrowing cost.

These loans can help self-employed borrowers qualify based on actual cash flow instead of lower taxable income. That can be a big deal if write-offs make tax returns look thinner than the business bank account does. But that flexibility usually comes with rates that run 0.50% to 1.50% above conventional mortgages, along with tougher reserve and down payment rules. Those tradeoffs help narrow down who this loan tends to work best for.

Who These Loans Are For and Final Takeaways

Borrower Profiles That Fit Best

Once you get past the credit, reserve, and down payment rules, the next step is simple: does this loan fit your file?

This option tends to work best for borrowers whose current income is stronger than what their tax returns show. That often includes self-employed borrowers, 1099 workers, freelancers, consultants, and commission-based earners.

Investors are a bit different. In many investor files, the main issue is the property's cash flow, not the borrower's personal earnings. So this loan makes more sense when personal income is the stronger part of the file. It can also work well for vacant, renovated, or seasonal properties.

The 12-month look-back window can be a big help when business income has gone up lately. Instead of leaning on older, lower earnings, it focuses more on what you're making now.

What to Check Before Applying

Before you apply, make sure the basics are in place:

- 12 consecutive months of statements - no missing pages and no gaps

- Deposit trends - steady or growing deposits usually help more than erratic activity; a recent decline can hurt your file

- No NSFs or overdrafts - underwriters often treat these as warning signs

- Large deposits documented - any single deposit over $10,000 or more than 50% of your monthly average will likely need backup, such as invoices or contracts

- Down payment and reserves ready - confirm you have enough liquid assets for both the down payment and post-closing reserves

- CPA letter in hand - if you're using business statements and your real expenses are lower than the standard 50% default, a CPA letter showing the actual expense ratio may increase your qualifying income

One more thing matters a lot: figure out whether personal income or property cash flow is stronger in your file. That single point often decides which loan program makes the most sense.

Key Points to Remember

A 12-month bank statement loan qualifies documented cash flow, not tax-return income. The goal is to line up the loan with the strongest part of your file.

That said, this loan can come with higher rates, tighter reserve rules, and close review of every statement in the file. When the loan type matches the actual strength of the application, the process is usually much smoother. When it doesn't, things can get hard fast.

FAQs

Can I qualify with recent overdrafts?

Recent overdrafts can be a red flag. Lenders look at your bank statements to gauge financial stability and cash flow, and frequent or recent overdrafts can make your application harder to approve or lead to stricter requirements.

You should also expect to explain any negative balances in writing. If overdraft activity is still happening, it may affect whether you qualify.

Do I need business or personal statements?

Not necessarily. Most lenders will accept personal or business bank statements, based on where your income lands.

If your business income is deposited into your personal account, personal statements may be enough. In many cases, lenders count personal deposits at or close to 100%.

Business statements can work too, but there’s usually more math involved. Lenders often apply an expense factor to business deposits, and that number is often around 50%.

What if my income increased recently?

If your income has gone up lately, a 12-month bank statement loan can be a smart option. It looks at your most recent 12 months of deposits to work out qualifying income, so it may line up better with what you’re earning now.

That matters if the last two years don’t tell the whole story. Instead of using a 24-month average that pulls in older, lower-income months, this loan can help you qualify based on your current cash flow.