No-Income Verification Mortgage: The Investor's Guide to Qualifying Without W-2s

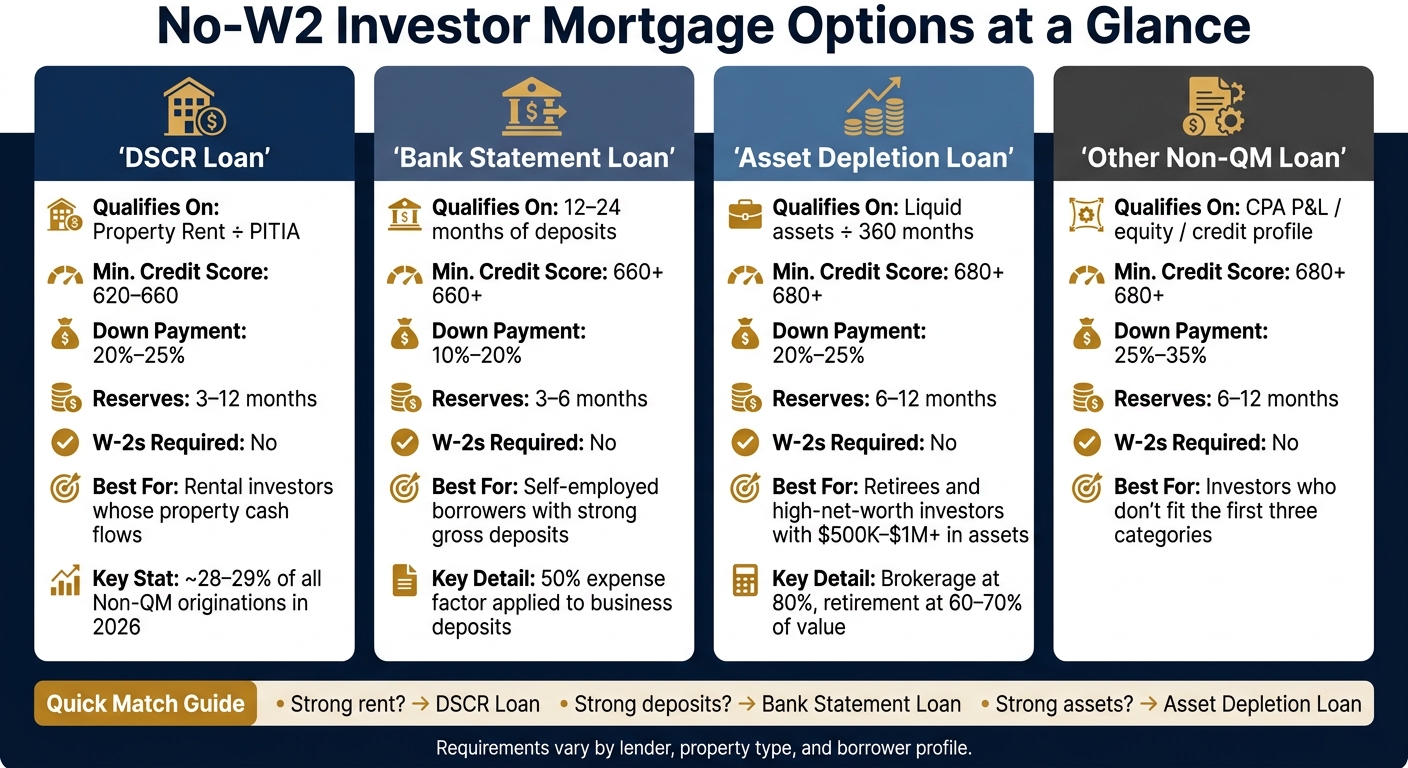

Yes, I can get an investor mortgage without W-2s. In most cases, the loan is based on rent, bank deposits, or liquid assets instead of pay stubs or tax returns. For many investors, the main cutoff points are a 620–680+ credit score, 10%–25% down in some programs, and 3–12 months of reserves.

Here’s the short version:

- DSCR loans use the property’s rent compared with PITIA

- Bank statement loans use 12–24 months of deposits

- Asset depletion loans turn assets into monthly income

- Other Non-QM loans use flexible docs, credit, and equity

If I want the simplest match:

- I pick DSCR when the property cash flows

- I pick bank statement when my deposits look stronger than my tax returns

- I pick asset depletion when I have cash, brokerage funds, or retirement assets

- I look at other Non-QM options when I do not fit the first three

One point matters a lot: this is not “no documents.” It is just a different set of documents. Lenders still check credit, down payment, reserves, lease or rent data, and the appraisal.

No-Income Verification Mortgage Types: DSCR vs Bank Statement vs Asset Depletion vs Non-QM

DSCR Loans Explained: How to Qualify Without a W2 or Tax Returns

sbb-itb-e7c549b

Quick Comparison

| Loan Type | What I Qualify With | Typical Credit Score | Typical Down Payment | Reserves |

|---|---|---|---|---|

| DSCR | Property rent ÷ PITIA | 620–660 | 20%–25% | 3–12 months |

| Bank Statement | 12–24 months of deposits | 620–660+ | 10%–20% | 3–6 months |

| Asset Depletion | Liquid assets ÷ set term | 640–680+ | 20%–25% | 6–12 months |

| Other Non-QM | Flexible docs, credit, equity | 680+ | 25%–35% | 6–12 months |

If I am trying to choose, I start with the part of my file that looks best on paper: rent, deposits, or assets.

The 4 main mortgage options for investors without W-2s

These four paths qualify investors in different ways: property cash flow, business deposits, liquid assets, or flexible Non-QM underwriting.

DSCR loans: qualify using rental income and property cash flow

A Debt Service Coverage Ratio (DSCR) loan comes down to one basic test: does the property pay for itself? Lenders divide the gross monthly rent by total PITIA, which includes Principal, Interest, Taxes, Insurance, and HOA dues. A DSCR of 1.0 to 1.25 is common, and 1.25 often leads to better pricing.

The big draw here is simple. Approval is based on the property's numbers, not your personal income. That's a major reason DSCR loans are so popular with rental portfolio investors. In 2026, they made up about 28% to 29% of all Non-QM loan originations. And while conventional loans usually cap individual investors at 10 financed properties, DSCR loans let investors keep going past that limit.

An investor with 10 conventional rentals used a DSCR loan to buy an 11th property at a 1.23 DSCR with 25% down and no tax returns.

If the property can't support the loan on its own, the next option is often documented business cash flow.

Bank statement and asset depletion loans for self-employed investors

For self-employed investors, the hard part usually isn't earning money. It's proving it on paper. Write-offs and depreciation can shrink taxable income enough to sink a conventional application, even when the borrower is in good shape financially.

Bank statement loans deal with that issue by using 12 to 24 months of personal or business deposits to estimate qualifying income. Lenders often apply a 50% expense factor to gross business deposits. So if a business shows $20,000 per month in deposits, that may count as about $10,000 per month in qualifying income.

If deposits don't look strong enough but assets do, asset depletion may help.

Asset depletion loans turn liquid assets - such as savings, brokerage accounts, and retirement funds - into a projected monthly income figure. Shorter depletion periods mean more qualifying income. Brokerage accounts are often counted at 80% of their value, while retirement accounts are usually discounted to 60% to 70%. This route tends to work best for borrowers with at least $500,000 to $1,000,000 in liquid assets and not much documented monthly income.

Other Non-QM investor loans with flexible documentation

Other Non-QM investor loans can qualify borrowers using CPA-prepared profit and loss statements or other flexible income documentation. These programs work as a catch-all for investors who don't fit DSCR, bank statement, or asset depletion rules. In these cases, underwriting leans more on a mix of property equity, credit profile, and alternative income evidence instead of standard personal income documents.

| Loan Type | Qualifies On | Tax Returns | Typical Credit Score |

|---|---|---|---|

| DSCR | Property rental income | No | 620–660 |

| Bank Statement | 12–24 months of deposits | No | 620–640 |

| Asset Depletion | Total liquid assets | No | 640–680 |

| Other Non-QM | CPA P&L / flexible docs | No | 640 |

Next, compare what lenders actually review, including credit, reserves, leases, and appraisals.

What lenders actually review instead of pay stubs and tax returns

Even without W-2s or tax returns, lenders still check the same core stuff: the property's cash flow, your credit report, and your liquid reserves. Once you pick the loan type, underwriting usually comes down to those three items.

Property income, appraisals, leases, and DSCR calculations

With DSCR loans, the property does most of the talking. Lenders order an appraisal with Form 1007 for single-family rentals or Form 1025 for 2- to 4-unit properties to estimate market rent and value. That rent estimate stands in for your personal income docs.

One detail matters more than many borrowers expect: lenders use the lower of the signed lease rent or the appraiser's market rent estimate. So if your lease shows $2,200 per month but the appraiser comes in at $2,000, the lender runs the DSCR using $2,000. That can be enough to drag a close deal below the minimum mark.

A DSCR of 1.0 means the rent covers PITIA. Get into the 1.20 to 1.25+ range, and pricing often gets better. For short-term rentals, many lenders also trim projected revenue by 10% to 25% before they calculate DSCR.

Credit score, down payment, and cash reserve requirements

Skipping W-2s doesn't mean skipping credit. Lenders still pull a full credit report. Minimum scores often start around 620 to 660, while 720+ may lead to better rates and looser terms.

Down payments on no-income-verification investor loans usually fall in the 20% to 25% range, although some strong borrowers may qualify with 15% down. On top of that, lenders usually want 3 to 12 months of PITIA in liquid reserves, seasoned for 30 to 90 days before closing.

Comparison table: what each loan type uses instead of W-2s

Use the table below to see what each loan type reviews in place of W-2s.

| Loan Type | Primary Approval Driver | Documents Reviewed | Down Payment | Reserves |

|---|---|---|---|---|

| DSCR | Property cash flow | Current lease, Form 1007/1025 appraisal, property insurance quote | 20%–25% | 3–12 months |

| Bank Statement | Average monthly deposits | 12–24 months of personal or business bank statements | 10%–20% | 3–6 months |

| Asset Depletion | Total eligible assets | Checking, savings, brokerage, and retirement statements | 20%–25% | 6–12 months post-close |

For asset depletion loans, lenders divide eligible liquid assets by 360 months to create qualifying income.

With those underwriting pieces in place, the next step is figuring out which loan type fits your borrower profile.

How to pick the right no-income verification loan for your situation

Now that you know what lenders look at, the next step is simple: pick the loan that lines up with the strongest part of your file.

Matching loan type to borrower profile

The best fit usually comes down to one thing you do well on paper: property cash flow, deposit history, or liquid assets.

DSCR loans are a good match for rental purchases or refinances when the property's rent can cover PITIA. They work especially well for LLC purchases and for investors with more than one property.

Bank statement loans tend to fit self-employed borrowers and 1099 earners who show strong gross deposits but take large write-offs that reduce taxable income. Instead of leaning on W-2s or tax returns, lenders usually average 12 to 24 months of deposits.

Asset depletion loans are often the better route for retirees and high-net-worth investors who have large liquid assets but not much steady paycheck income.

Other Non-QM investor loans can work when a deal doesn't meet DSCR standards but the borrower still brings strong credit, strong equity, or both. These programs often call for a larger down payment, usually around 25% to 35%, along with a minimum credit score near 680+.

Documents to gather before applying

Once you know which lane fits, get your paperwork together for that loan type.

Doing this early helps cut delays and gives you a better read on what you may qualify for. In most no-income-verification programs, the main checklist includes:

- Photo ID - a government-issued ID

- Entity documents - if you're closing in an LLC, have your Articles of Organization, Operating Agreement, and EIN letter ready

- Bank or asset statements - 2 to 6 months for reserves and down payment proof, or 12 to 24 consecutive months for a bank statement loan

- Lease agreements or rent rolls - for occupied properties; if the property is vacant, the lender will usually rely on the appraiser's Form 1007 or Form 1025 market rent estimate

- STR income data - for short-term rentals, bring a trailing 12-month booking history or AirDNA projections

- Purchase contract, current mortgage statement, and insurance quote or binder

One small step can save a lot of back-and-forth: make sure your down payment funds have been in your account for at least 30 to 60 days before you apply. Large recent deposits often get flagged, and lenders may ask for a paper trail that can slow the closing process.

Qualification table: estimated requirements by loan type

Use this table as a quick first-pass filter, not a promise of approval. Terms can shift based on the lender and your borrower profile.

| Loan Type | Min. Credit Score | Income Verification Method | Typical Down Payment | Reserves Required | W-2s or tax returns? |

|---|---|---|---|---|---|

| DSCR Loan | 620–660 | Property Rent ÷ PITIA | 20%–25% | 3–12 months | No |

| Bank Statement | 660+ | 12–24 mo. avg. deposits | 10%–20% | 3–6 months | No |

| Asset Depletion | 680+ | Liquid assets ÷ 360 months | 20%–25% | 6–12 months | No |

| Other Non-QM | 680+ | None (equity/credit-based) | 25%–35% | 6–12 months | No |

These ranges are approximate and may change based on the lender, property type, and borrower profile.

Even a score bump can matter here. Moving from 680 to 720 can improve pricing and may also open the door to higher-leverage options across Non-QM programs.

Conclusion: Comparing no-W-2 investor financing options

After looking at these loan types side by side, the choice usually comes down to one thing: what part of your file looks strongest.

Not having a W-2 doesn't shut you out of investor financing. It just changes how you qualify. Instead of W-2 income, lenders may look at property cash flow, bank deposits, or assets.

Here’s the simple way to think about it:

- DSCR loans fit borrowers whose rental income supports the deal

- Bank statement loans fit borrowers with strong deposit history

- Asset depletion loans fit borrowers with enough assets to qualify

The best move is to match the loan to the part of your file that gives you the best shot: rent for DSCR, deposits for bank statements, and assets for depletion. That match is often the fastest path to approval.

At LoanGuys.com, we help investors match DSCR and Non-QM financing to the deal, the credit profile, and the documents they have on hand.

FAQs

Which no-income mortgage fits me best?

The right no-income verification loan comes down to one thing: how the lender plans to qualify you.

Some loans lean on the property's income. Others look at your own cash flow or the assets you have on hand. That difference matters a lot.

- DSCR loan: best for buy-and-hold investors who want speed and simplicity

- Bank statement loan: best for self-employed borrowers or freelancers with strong business deposits

- Asset depletion loan: best if you have major liquid assets but limited taxable income

Can I qualify if the property is vacant?

Yes. You can still qualify even if the property is vacant.

For DSCR loans, lenders usually rely on a professional appraiser’s rental income analysis instead of an existing lease. The appraiser estimates the market rent, and the lender uses that number to calculate your Debt Service Coverage Ratio.

If you already have a signed lease, some lenders may use that figure instead.

What can hurt approval even with no W-2s?

Even without W-2s, approval still comes down to a few key numbers. Most lenders want to see a credit score in the 620 to 660 range, plus enough liquid assets to cover 3 to 6 months of mortgage reserves.

With DSCR loans, the property’s cash flow carries a lot of weight. If the rental income comes in below the lender’s minimum DSCR - usually 1.0 to 1.25 - the application may be denied.