Asset-Based Lending for Real Estate: How to Qualify Without Income Docs

Yes - you can qualify for an investment property loan without W-2s or tax returns. In most cases, lenders look at rent, assets, credit, down payment, reserves, and the property itself instead of job income.

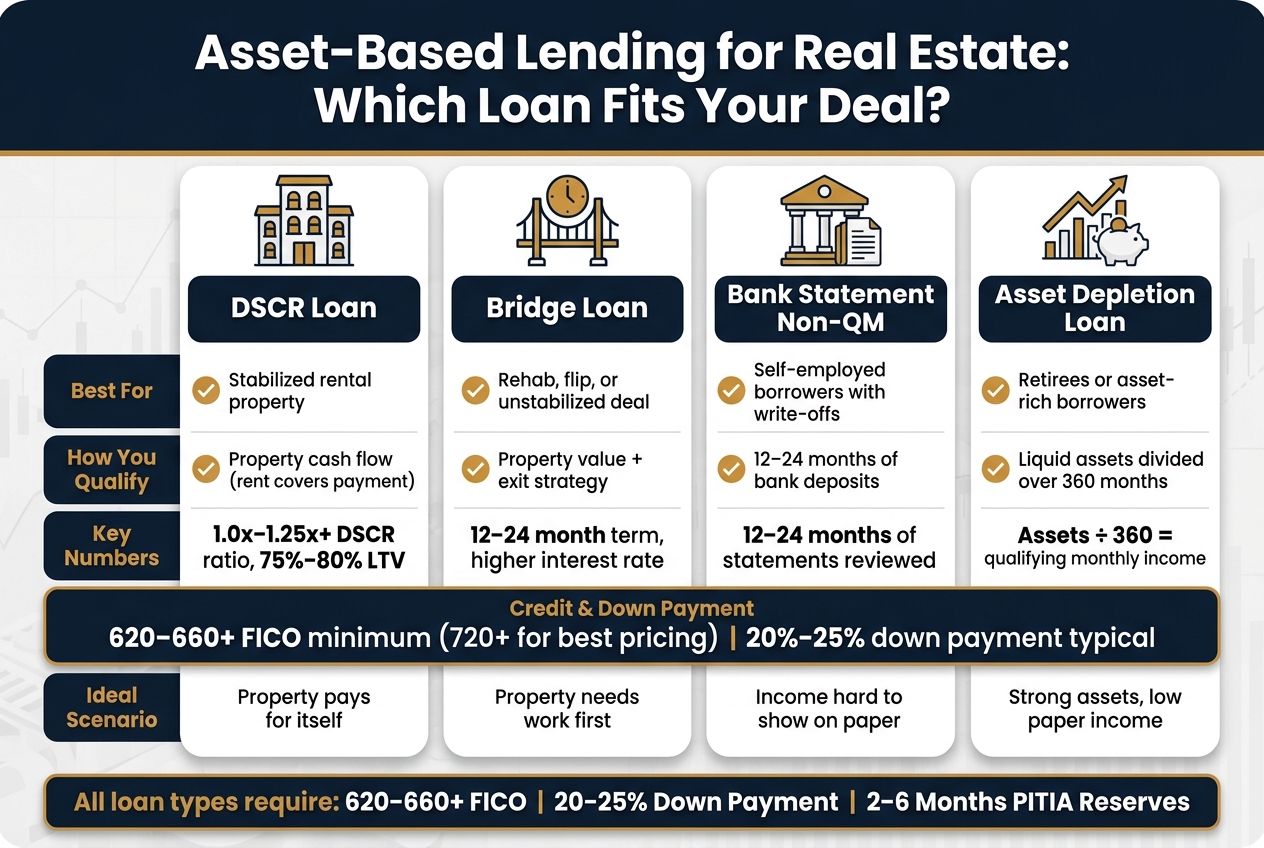

If I had to boil it down, it works like this:

- DSCR loans fit stabilized rentals where rent covers the payment

- Bridge loans fit fix-and-flip or value-add deals with a clear payoff plan

- Non-QM bank statement loans fit self-employed borrowers with strong deposits

- Asset depletion loans fit retirees or borrowers with large liquid funds but low paper income

A few numbers matter right away:

- Many lenders want 620–660+ FICO

- Best pricing often starts around 720+

- Down payments are often 20%–25%

- Many DSCR lenders want 1.0x to 1.25x DSCR

- Reserves often land around 2 to 6 months of PITIA

- Bridge terms are often 12 to 24 months

Asset-Based Loan Types for Real Estate Investors: DSCR vs Bridge vs Non-QM

Top 15 DSCR Loan Questions (No Income, LLCs, Airbnb & More)

sbb-itb-e7c549b

Quick Comparison

| Loan type | Best for | Main way you qualify | Common range to expect |

|---|---|---|---|

| DSCR | Stabilized rental property | Property cash flow | 1.0x–1.25x+ DSCR, often 75%–80% LTV |

| Bridge | Rehab, flip, or unstabilized deal | Property value + exit plan | 12–24 months, higher rate, short term |

| Bank statement non-QM | Self-employed borrower | 12–24 months of deposits | Personal or business statements used |

| Asset depletion | Retirees or asset-rich borrowers | Liquid assets turned into monthly income | Assets divided over a set term, often 360 months |

The short version: if the property pays for itself, DSCR may work. If the property needs work first, bridge may fit. If your income is hard to show on paper, non-QM may be the better path.

I’d use this guide to match the loan to the deal, line up the right documents, and avoid applying for the wrong program first.

Step 1: Learn the main ways to qualify without W-2s or tax returns

The three most common paths are DSCR loans, bridge loans, and non-QM programs. Each one looks at the deal in a different way. Instead of leaning on W-2s or tax returns, lenders focus on the property, your assets, or both. So the best option depends on what you're buying and how your finances are set up.

DSCR and rental property loans based on cash flow

A DSCR loan qualifies you based on the property's income, not your personal income. The formula is simple: Gross Monthly Rental Income ÷ Monthly PITIA (principal, interest, taxes, insurance, and HOA fees). If the result is 1.0 or higher, the property is covering its own debt. Most lenders want to see at least 1.25x if you want their best rates and up to 80% LTV.

These loans are a good match for long-term rentals and, in some cases, short-term rentals. With short-term rentals, lenders often trim the income they count because of seasonality. And if the property is vacant, they may use a rent survey instead of a lease.

If the property isn't stabilized yet, a bridge loan may make more sense.

Bridge loans based on property value and exit strategy

Bridge loans are short-term financing tools, usually 12 to 24 months, for properties that aren't ready for permanent financing yet. This is common with fix-and-flip deals, value-add buys, and other purchases where timing matters.

Here, lenders usually care most about three things:

- Collateral value

- Your project plan

- Your exit strategy - how you'll pay off the loan, either by selling the property or refinancing once it's stabilized

Because the underwriting is centered on the asset and the exit plan, bridge loans can often close fast. The catch is cost. Rates are higher than long-term rental loans, and LTV is usually based on the total project cost, not just the purchase price.

If the problem is complicated income, not a transitional property, non-QM lending is often the better lane.

Non-QM options using bank statements or assets

Non-QM programs are built for borrowers whose tax returns don't show the full picture or who qualify through assets instead of income. For investors in that camp, two options come up again and again.

Bank statement loans are geared toward self-employed borrowers and business owners with heavy write-offs. Rather than using tax returns, lenders review 12 to 24 months of personal or business bank statements and deposits to calculate a qualifying income figure.

Asset depletion loans work differently. If you have large liquid assets - like brokerage accounts, savings, or retirement funds - lenders total the eligible amount and divide it over a set term to create qualifying income. This can work well for self-employed borrowers and retirees whose taxable income looks low on paper even though their finances are much stronger.

Next, look at the credit, down payment, appraisal, and reserve standards lenders use when approving these loans.

Step 2: Know what lenders actually review on no-income-doc investment loans

Each loan type looks at the same basic items, but not every lender puts the same weight on them.

Credit score, down payment, and recent credit events

When W-2s and tax returns aren't part of the file, lenders look much harder at your credit profile. In most cases, minimum FICO scores start around 620 to 660. If you're at 720 or higher, you’ll usually see the best pricing. Down payments are often 20% to 25%, which means 75%–80% LTV.

Some programs will go down to 15% if you have 700+ credit and the property supports a 1.25x DSCR. And yes, recent credit events still count. A strong score helps, but lenders still want to know if there were late payments, bankruptcies, foreclosures, or other recent issues.

Property income, appraisal, and reserve requirements

On these loans, the property does a lot of the heavy lifting. Lenders use an appraisal to estimate market rent, usually with Form 1007 for single-family homes or Form 1025 for 2–4 units.

If there’s a signed lease, underwriters usually use the lower number between:

- the lease rent

- the appraiser’s market rent estimate

That detail matters more than many borrowers expect. If the lease is below market, it can drag down the qualifying rent. That’s one of the main ways the property stands in for income docs.

Most lenders want a DSCR of at least 1.0x. If you’re at 1.25x or higher, approval tends to get easier and pricing tends to improve.

Reserves matter too. Lenders often want 2 to 6 months of PITIA in reserves. For larger loans above $1.5 million, that can jump to 6 to 12 months or more. Funds in checking, savings, and money market accounts can count, and many lenders also count part of retirement or brokerage accounts toward that total.

Once you know these rules, you can line up the loan with the property’s timeline and cash flow instead of guessing your way through it.

Why self-employed and retired borrowers often qualify here

This is one reason these loans appeal to self-employed borrowers, retirees, and people with a lot of assets but uneven paper income.

Retirees and asset-rich borrowers can use asset depletion, which takes net liquid assets and divides them by 360 months to create qualifying income. In plain English, it turns liquidity into a monthly income figure without leaning on tax returns or monthly distributions.

The next step is choosing the loan type that fits the deal.

Step 3: Match the right loan type to your investment plan

With the lender's checklist in hand, the next move is simple: pick the loan that fits both the property's current state and how you plan to get out of the deal.

When to use DSCR or rental property financing

Use a DSCR loan when the property is stabilized and the rent covers the monthly payment. This option makes the most sense for a long-term rental with a signed lease or clear market rent, a down payment of 20%–25%, and enough reserves to meet the lender's rules.

One catch: underwriters often reduce short-term rental income when they size the deal. So if you're working with Airbnb-style rent, use a conservative estimate when you check whether the numbers work.

If the property isn't stabilized yet, bridge financing usually makes more sense.

When a bridge loan is the better fit

Use bridge financing when speed matters or the property's condition knocks it out of the running for permanent financing. If the home needs major rehab or isn't habitable yet, a DSCR lender will likely pass. Bridge loans can close in 7–14 days and can fund renovation costs, which is why investors often use them for auction purchases, distressed acquisitions, and fix-and-flip or buy, rehab, rent, refinance projects.

The main things to look at are:

- Speed of close

- Funding for rehab costs

- Shorter loan term

- A clear exit strategy - sale or refinance once the property is stabilized

If the deal is stabilized but your income is tough to document, shift to a non-QM structure.

When non-QM is the better fit for borrowers with complex income

Sometimes the property's cash flow doesn't tell the whole story. That's where non-QM comes in. A self-employed borrower with strong deposits but heavy write-offs can use 12–24 months of bank statements to show income. A retired investor with a large brokerage account but very small distributions can use asset depletion to create a qualifying income figure.

Put plainly: DSCR works when the property supports the file, bank statement non-QM works when personal cash flow is the main story, and asset-based non-QM works when liquidity is what gets the deal over the line.

Once you've picked the loan type, gather the documents that match that path.

Step 4: Prepare your file and move toward approval

Documents to gather before you apply

Once you’ve picked the loan type, build the file around the lender’s closing checklist. The point here is simple: these documents help prove the property’s income and your available funds without using tax returns.

Here’s what to gather before you apply:

- Government-issued photo ID

- 2 months of bank statements

- Executed purchase contract

- Signed leases for occupied units

- Entity documents if the borrower is an LLC or corporation (Articles of Organization, Operating Agreement, and EIN letter)

- Rent roll or 1007/1025 rent schedule

- Insurance quote or binder

- Title commitment

If it’s a value-add deal, include a detailed renovation budget. If it’s a short-term rental, include 12 months of booking history or an STR income report.

Once the file is in order, the next slow point is often the appraisal.

How appraisal, timeline, and liquidity affect closing

Order the appraisal right away. It’s often the longest part of the closing process.

Reserves carry a lot of weight because they help fill the gap when W-2 income isn’t in the file. Plan for the down payment, closing costs, and reserves. Cash usually gets counted in full, while brokerage and retirement accounts are often discounted.

When the lender sends conditional approval items, reply the same day. A fast response on things like an updated bank statement or an insurance binder can shave days off the closing timeline.

From there, the borrower’s job is pretty straightforward: match the property, the file, and the exit plan.

Conclusion: The clearest path to qualifying without income docs

DSCR works for stabilized rentals. Bridge loans work for properties that need repairs and have a clear exit. Bank statement and asset depletion loans work for borrowers whose income is tough to show on paper. The right loan comes down to the property, available funds, and the exit plan.

FAQs

Can I qualify with a vacant rental property?

Yes. You can qualify for an asset-based loan, such as a DSCR loan, with a vacant rental property.

Instead of relying on an active lease, some lenders use a third-party appraisal that includes a market rent survey. They then use that estimated market rent to calculate the property's debt service coverage ratio.

How do lenders calculate income on an asset depletion loan?

Lenders figure income for an asset depletion loan by turning liquid assets - like checking and savings accounts, stocks, and retirement accounts - into a monthly income number.

Here’s how it works: they add up your qualifying assets and divide that total by a set number of months. Some lenders use 360 months. Others use anywhere from 60 to 120 months.

That final number becomes your monthly income for debt-to-income review.

What can disqualify me from a DSCR or bridge loan?

Even without income paperwork, you can still get turned down if you miss basic property or credit rules.

Common problems include:

- A credit score below 620 to 640

- A property that isn't an investment property

- Rental income that doesn't meet the lender's minimum DSCR

- Not enough down payment

- Not enough liquid reserves to cover PITIA