Stated Income Loans for Real Estate Investors: Are They Still Available?

Yes - but not in the old form. If I’m a real estate investor and I don’t want to use W-2s or tax returns, I can still get financing through DSCR loans, bank statement loans, or asset-based loans.

Here’s the short answer:

- Old stated income loans are gone for standard consumer mortgages after post-2008 rule changes.

- Investor loans still exist that skip W-2s and tax returns, but they are not no-doc loans.

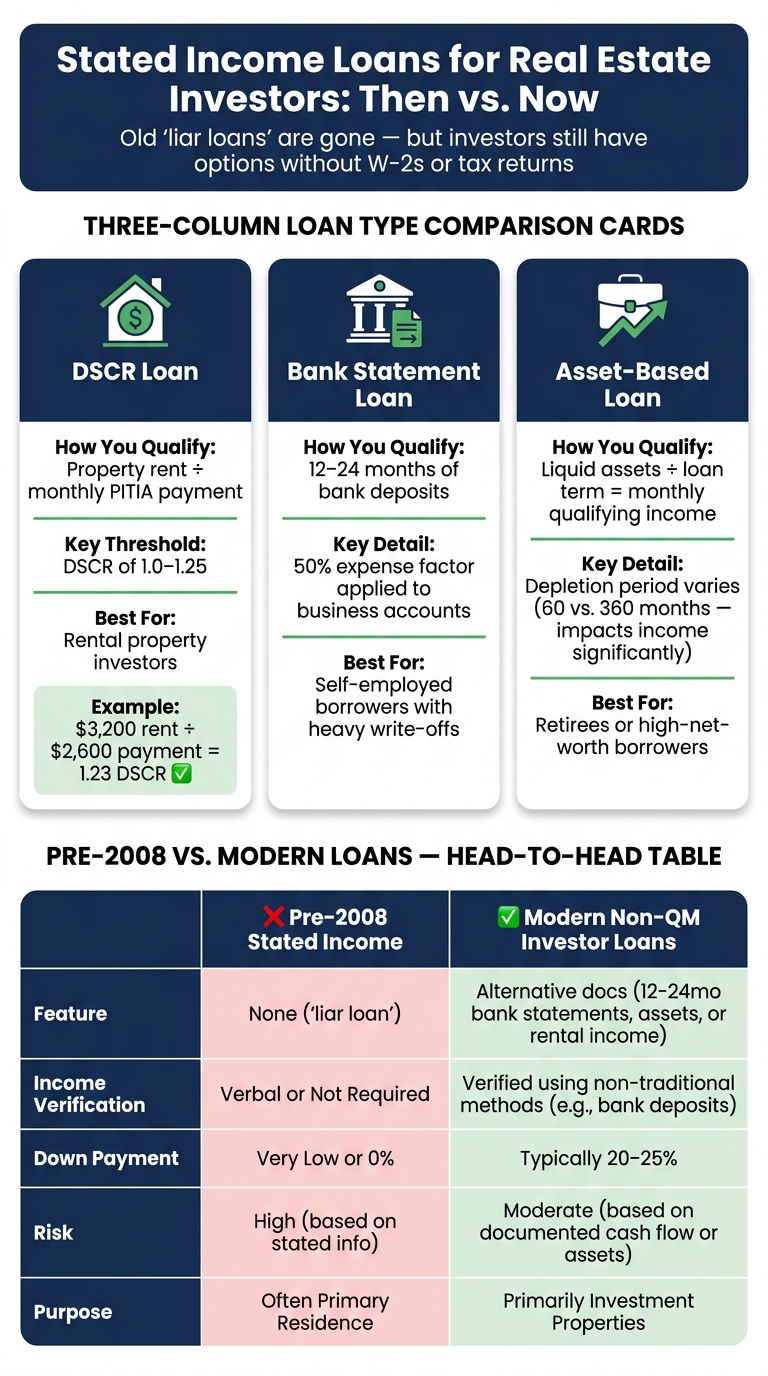

- DSCR loans look at whether the property’s rent covers the monthly housing payment.

- Bank statement loans use 12 to 24 months of deposits to estimate income.

- Asset-based loans use savings, brokerage funds, or retirement accounts to qualify.

- Most lenders still check credit score, appraisal, down payment, and cash reserves.

- Expect 600–680+ minimum credit scores, 20%–25% down, and often 6–12 months of reserves.

- Rates are often 1.5%–3% higher than standard conforming mortgages.

If I want the plain-English version, it’s this: lenders still verify repayment - they just use rent, deposits, or assets instead of pay stubs and tax returns.

A quick side-by-side helps:

| Loan type | How I qualify | Best fit for |

|---|---|---|

| DSCR loan | Property rent vs. PITIA payment | Rental investors |

| Bank statement loan | 12–24 months of bank deposits | Self-employed borrowers |

| Asset-based loan | Liquid assets converted into monthly income | Retirees or high-asset borrowers |

So if I’m asking whether “stated income” still exists, the short answer is no in the old sense, yes in a newer investor-loan form.

Stated Income Loans vs. Modern Non-QM Investor Loans: Side-by-Side Guide

What happened to stated income loans after 2008

How pre-2008 stated income loans worked

Before the housing crash, some lenders offered mortgage products with little to no income proof. Borrowers could state their income with little or no verification. These loans went by names like SIVA (Stated Income, Verified Assets), SISA (Stated Income, Stated Assets), and NINA (No Income, No Assets). Over time, they picked up the label "liar loans" because some borrowers overstated what they earned to qualify for bigger mortgages.

That setup helped inflate loan applications, and defaults climbed. After the crash, Dodd-Frank's Ability-to-Repay rule put an end to true consumer stated-income loans. From there, investor lending moved into a different lane: business-purpose financing.

Why investor loans work differently today

ATR applies to owner-occupied consumer mortgages, not business-purpose loans. Because investment property loans fall under business-purpose lending, they are generally exempt from strict ATR rules.

The big shift wasn't whether lenders check repayment ability. It was how they check it. Today's investor loan programs still require documentation, but not the usual W-2s or tax returns. Instead, lenders may look at rental income, bank deposits, or liquid assets.

That's the link between old stated-income lending and today's non-QM investor loans. Modern investor loans still verify repayment. They just do it with rent, deposits, or assets. So when you hear "no-doc" today, it usually means no personal income documents, not no documentation at all. Lenders still verify the deal, just with different proof.

sbb-itb-e7c549b

DSCR Loans: The Investor Loan Most People Don't Know Exists

What replaces stated income loans for investors now

The modern replacement is non-QM investor financing. That usually means DSCR loans, plus bank statement and asset-based options.

The big shift is simple: lenders now want proof. Instead of taking a borrower's word on income, they look at property cash flow or documented assets. For most investors, DSCR is the first place to look.

DSCR loans for rental properties

The most common replacement is the Debt Service Coverage Ratio (DSCR) loan.

DSCR is calculated by dividing monthly rent by the property's total housing payment, including:

- Principal

- Interest

- Taxes

- Insurance

- Association fees

A DSCR of 1.0 means the property breaks even. Many lenders look for a ratio between 1.0 and 1.25.

Approval usually depends on the lease agreement or a market rent analysis from the appraisal, along with the borrower's credit score, cash reserves, and property type. These loans often close faster because the underwriting centers on the property instead of tax returns.

Bank statement and asset-based loan options

DSCR works for many investors, but not all of them. That's where bank statement and asset-based programs come in.

Bank statement loans are often a fit for self-employed investors whose tax returns don't show their earnings clearly. Lenders review 12 to 24 months of personal or business deposits and use that history to calculate income. For business accounts, they often apply a 50% expense factor.

Asset-based loans, also called asset depletion loans, use a different method. The lender takes total liquid assets, such as savings, brokerage accounts, and retirement funds, and divides them by the loan term to estimate monthly qualifying income.

One detail matters a lot here: not all lenders use the same depletion period. Some use 60 months, while others use 360 months. That can change the qualifying income by a lot.

Old stated income vs. modern non-QM investor loans: side-by-side comparison

Here's how old stated-income loans stack up against today's non-QM options.

| Feature | Pre-2008 Stated Income | Modern Non-QM Investor Loans |

|---|---|---|

| Documentation | None ("Liar Loans") | Alternative (bank statements, rent surveys, asset statements) |

| Main Approval Method | Borrower's word alone | Verified property cash flow or liquid assets |

| Underwriting Style | Unregulated/loose | Dodd-Frank/ATR compliant |

| Common Use Cases | Primary residences and investment properties | Primarily investment for DSCR loans; primary, second home, or investment for bank statement and asset-based loans |

| Risk Controls | Minimal to none | Higher down payments, credit floors, and reserves |

How investors qualify today without W-2s or tax returns

Today, many investor loans are based on property cash flow, deposits, or assets instead of W-2s or tax returns. In plain English, underwriting has shifted away from the borrower's tax file and toward the deal itself.

Documents lenders typically ask for

Most lenders ask for some mix of the items below:

- Government-issued ID - or a passport for foreign national investors

- Purchase contract or payoff statement for a refinance

- Appraisal with a market rent analysis - often Form 1007, the Comparable Rent Schedule, which also serves as the rent estimate when the property is vacant

- Existing lease agreements or rent rolls for properties already generating income

- 12 to 24 months of bank statements for bank statement loan applicants

- Asset account statements (brokerage, savings, retirement) for asset depletion programs

- LLC documents if closing in an entity - typically the Articles of Organization, operating agreement, and EIN letter

- Insurance binder for the property

Key approval factors beyond income paperwork

Once the paperwork is in, lenders usually size the loan around a few hard numbers.

| Factor | What Lenders Look At | U.S. Dollar Example |

|---|---|---|

| DSCR Ratio | Monthly rent versus total PITIA | $3,200 rent ÷ $2,600 payment = 1.23 DSCR |

| Loan-to-Value (LTV) | Loan amount relative to appraised value | Most programs allow 75%–85% LTV |

| Credit Score | Sets rate tiers and max leverage | 720+ unlocks the lowest available rates |

| Cash Reserves | Liquid funds remaining after closing | 6 months on a $2,600 payment = $15,600 required |

Credit score still matters quite a bit. Minimum scores often fall between 600 and 680. If you're in the 720 to 740+ range, you can usually get better pricing and more leverage.

Property type matters too. Lenders tend to like 1–4 unit residential properties that are habitable and rent-ready. If the place is distressed, you may need a bridge loan first.

Pros and cons of flexible-documentation investor loans

These loans can solve a big problem for investors who don't show income in the usual way. But there's no free lunch. The trade-offs matter.

| Advantages | Drawbacks |

|---|---|

| Faster closings: Typically 14–30 days vs. 45–60 for conventional loans | Higher rates: Usually 1.5%–3% above standard market rates |

| Works with tax deductions: Qualification focuses on the property's income rather than tax-return deductions | Larger down payments: Most programs require 20%–25% down |

| No personal DTI test: Underwriting centers on the property, not your debt load | Prepayment penalties: Common step-down structures run 3–5 years |

| Helps portfolio investors grow: Useful for investors who want to move past the 10-financed-property cap | Reserve requirements: Expect to show 6–12 months of liquid PITIA reserves |

That means the fit often comes down to the deal. If speed, scale, or tax write-offs are the issue, a flexible-documentation loan can make sense. If your main goal is the lowest rate, the extra cost and reserve rules may be a sticking point.

When these loan programs make sense and how LoanGuys.com helps

Investor scenarios where non-QM financing is a good fit

These loans work well for investors whose income, assets, or property type don't line up with conventional underwriting.

Self-employed investors with heavy write-offs often have an easier path with bank statement loans than with tax returns.

Portfolio investors getting close to the conventional 10-property limit can use DSCR financing to keep buying rentals.

Short-term rental investors may qualify with AirDNA data or past booking history when the property doesn't have a standard long-term lease.

Retired investors or high-net-worth borrowers with strong assets and limited earned income may be a fit for asset-based loans.

How LoanGuys.com fits into today's investor lending market

Those are the kinds of deals LoanGuys.com is built to fund.

LoanGuys.com offers DSCR loans, non-QM mortgages, bridge loans, fix-and-flip loans, and rental-property financing for 1–4 units, multifamily, and commercial properties. The company focuses on the newer loan options investors use in place of old stated-income mortgages. That includes borrowers who don't fit conventional underwriting, such as self-employed investors, 1099 earners, foreign nationals, and borrowers with recent credit events.

First-time investors are welcome, and no prior real estate experience is required to qualify. LoanGuys.com has funded over 4,000 loans and has more than $100 million in available capital.

Conclusion: the short answer for investors

So, are stated-income loans still available? Not in the old way.

True stated-income loans are gone. The main investor options today are DSCR loans, bank statement loans, and asset-based financing. These programs check repayment ability through rent, deposits, or assets instead of W-2s or tax returns.

FAQs

Can I get a DSCR loan with a vacant property?

Yes. You can often get a DSCR loan for a property that’s currently vacant.

Here’s how it usually works: instead of asking for a signed lease at closing, the lender will often rely on an appraisal that includes a market rent analysis. That analysis estimates what the property should rent for, and the lender uses that number to calculate the debt service coverage ratio.

If you already have a lease in place, some lenders may use it instead, as long as the rent is in line with the local market.

Do DSCR loans work for short-term rentals?

Yes. DSCR loans can work for short-term rentals. Some lenders will use Airbnb or VRBO income to qualify the property. They usually base that number on market rent data or on annualized short-term rental income.

There’s a catch, though: lenders often trim that income before they calculate the debt service coverage ratio. A common move is a 20% reduction to account for vacancy or swings in booking income. And the property must be non-owner-occupied.

Can I close in an LLC?

Yes. With modern investor financing programs like DSCR loans, investors can often close in an LLC.

Because these are business-purpose, non-QM loans, lenders often let you hold title in an LLC, LP, or corporation. You’ll just need to provide the required entity documents at closing.