Bank Statement Loans vs DSCR Loans

If I had to sum it up in one line: bank statement loans qualify you; DSCR loans qualify the rental property.

If your tax returns look low but your bank deposits are strong, a bank statement loan may fit. If the property's rent can cover PITIA and hit a DSCR of 1.00+, a DSCR loan may be the better pick. In most cases, bank statement loans use 12–24 months of deposits and still check DTI, while DSCR loans focus on rent, often need 20%–25% down, and can close in about 15–30 days.

What I’d look at first:

- How you qualify: borrower income vs. property rent

- Income review: bank deposits, CPA letter, or lease/Form 1007

- Cash-flow rule: DTI for bank statement loans vs. monthly rent ÷ PITIA for DSCR

- Down payment: about 10%–20% for bank statement loans vs. 20%–25% for DSCR

- Reserves: often measured in months of PITIA

- Closing time: about 30–45+ days for bank statement loans vs. 15–30 days for DSCR

- LLC use: more common with DSCR loans

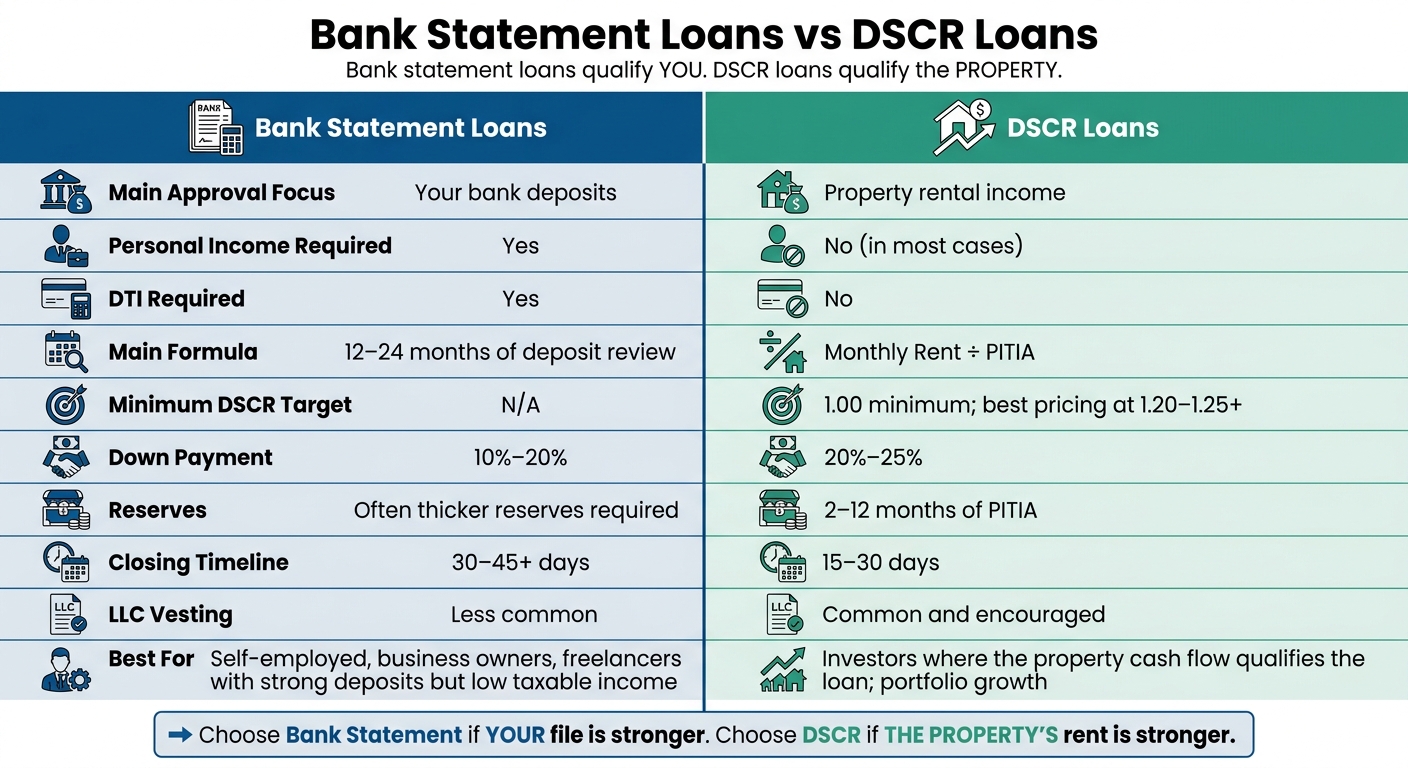

Bank Statement Loans vs DSCR Loans: Side-by-Side Comparison

Bank Statement Loans Explained: The Real Numbers Behind The Approval.

sbb-itb-e7c549b

Quick Comparison

| Factor | Bank Statement Loan | DSCR Loan |

|---|---|---|

| Main approval focus | Your bank deposits | Property rental income |

| Personal income needed | Yes | No in most cases |

| DTI required | Yes | No |

| Main formula | Deposit review over 12–24 months | Rent ÷ PITIA |

| Typical DSCR target | N/A | 1.00 minimum, better pricing around 1.20–1.25+ |

| Down payment | 10%–20% | 20%–25% |

| Reserves | Often more months required | Often 2–12 months of PITIA |

| Closing timeline | 30–45+ days | 15–30 days |

| LLC vesting | Less common | Common |

Bottom line: if your file is stronger than the deal, I’d look at a bank statement loan. If the rent is stronger than your personal income on paper, I’d look at DSCR first.

How Bank Statement Loans Work

A bank statement loan uses the deposits in your personal or business accounts to estimate income. The lender usually reviews 12 to 24 months of statements, then plugs that number into a standard DTI analysis. For rental purchases, the loan is still built around your income, not the property's rent. That's the big split between a bank statement loan and a DSCR loan.

Income Review and Required Documents

When lenders review business bank statements, they usually apply an expense factor to estimate net income. A common number is 50%. Some lenders use a higher factor based on the type of business. If your actual overhead is lower, a CPA letter may help support a lower expense factor, which can increase your qualifying income.

You’ll usually need:

- 12 to 24 months of bank statements

- Credit authorization

- Asset statements for down payment and reserves

- Purchase contract

- Business entity documents if buying through an LLC

- CPA letter or CPA-prepared profit and loss statement (some lenders)

Typical Qualification Standards

Most programs ask for a minimum FICO score of 660 to 680. Down payments for investment properties often start at 20%, though some programs may allow 10% to 15% for strong borrowers. Reserves are measured in months of PITIA, and the amount usually goes up as the loan size increases. Closing often takes 30 to 45 days because the lender has to review the statements by hand.

Next, it helps to compare that borrower-first setup with a loan that looks mainly at property income.

Best Use Cases for Self-Employed Borrowers

This loan tends to work best when your bank deposits show more income than your tax returns do. That happens a lot with business owners who write off costs like equipment and depreciation. On paper, taxable income may look low. In practice, cash flow can still be strong.

Put simply: bank statement loans qualify the borrower, while DSCR loans qualify the property.

How DSCR Loans Work

Bank statement loans qualify the borrower. DSCR loans qualify the property. The lender looks at the rent the property brings in and compares it with the monthly housing payment. Your personal income usually doesn't drive the decision.

DSCR Calculation and Rental Income Review

DSCR is simple:

Monthly rent ÷ monthly PITIA

PITIA stands for principal, interest, taxes, insurance, and HOA dues.

For purchases, lenders often use Form 1007 rent estimates. For properties that are already rented, they usually review the current lease. In many cases, underwriting is based on the lower of the lease rent or the appraised market rent.

Some programs also allow short-term rentals. When they do, lenders may apply a 20% haircut to gross revenue.

That rent-based test is the big difference between DSCR loans and borrower-income loans.

Common DSCR Thresholds and Property Types

A 1.00 DSCR is the usual floor. Most lenders give their best pricing when the ratio is 1.20 to 1.25 or higher. Some programs go as low as 0.75, and a few offer no-ratio options for properties that come in under 1.00.

Eligible property types often include:

- Single-family rentals

- 2–4 unit properties

- Condos

- Condotels

- Modular homes

- Mixed-use properties

DSCR loans also commonly allow LLC vesting.

When DSCR Loans Make the Most Sense

This setup fits investors who want approval based on the asset, not their job income. It's also a solid option for portfolio growth because each property can be reviewed on its own merits.

That becomes a big deal when you start comparing DSCR loans with other loan types, especially around documentation, reserve requirements, and how fast you can get to closing.

Bank Statement Loans vs DSCR Loans: Side-by-Side Comparison

The main difference comes down to how you qualify. And that one difference shapes the paperwork, speed, and loan setup from start to finish.

Qualification, Documentation, and Property Underwriting

Bank statement loans still look at the borrower’s debt-to-income ratio (DTI). DSCR loans don’t. With a DSCR loan, the lender looks at the property’s monthly rent and compares it to PITIA. That’s the qualifying test, and your personal DTI is not part of it at all.

| Factor | Bank Statement Loan | DSCR Loan |

|---|---|---|

| Underwriting Basis | Borrower's bank deposits | Property's rental income |

| Personal Income Required | Yes - 12–24 months of statements + CPA letter | No |

| DTI Analysis | Required | Not applicable |

| Property Cash Flow | Secondary; not the primary qualifying factor | Must meet minimum ratio (typically 1.0+) |

| LLC Vesting | Less common; usually closed in personal name | Standard and encouraged |

That creates a pretty clear split.

With a bank statement loan, the lender is still underwriting you. They want to review deposits, sort out income, and verify that your cash flow supports the loan. With a DSCR loan, the lender is focused much more on the deal itself. If the property rents support the payment, that carries the file.

Down Payment, Reserves, and Closing Speed

Bank statement loans can go as low as 10% down, while DSCR loans usually start around 20% to 25% down. So if you’re trying to conserve cash up front, bank statement financing may look more attractive.

Reserves show up in both loan types, but DSCR loans often call for 2 to 12 months of PITIA. Bank statement loans can also require reserves, and in many cases those reserve expectations are thicker.

DSCR loans are also usually faster. Since underwriting is centered on one property review instead of a manual breakdown of personal deposit history, DSCR loans can close in 15 to 30 days. Bank statement loans often land in the 30 to 45+ day range. If you’re up against a tight contract deadline, that speed can matter a lot.

| Factor | Bank Statement Loan | DSCR Loan |

|---|---|---|

| Down Payment Range | 10% – 20% | 20% – 25% |

| Reserve Requirements | Often thicker reserves required | 2 – 12 months of PITIA |

| Closing Timeline | 30 – 45+ days | 15 – 30 days |

| Underwriting Complexity | High - manual deposit analysis | Low - streamlined property review |

That borrower-versus-property split is usually the biggest factor when deciding which loan fits a given investor.

Which Loan Fits Your Investor Profile

Matching Borrower Types to Each Loan Option

After looking at how each loan works, the next step is simple: which one fits your file?

The answer comes down to where your case is strongest: your own cash flow or the property's rental income.

Bank statement loans make sense for self-employed borrowers, business owners, and freelancers whose tax returns don't show their full earning power. Go with this option when your bank deposits tell a better story than your tax returns or rental income.

DSCR loans make more sense when the property's cash flow can qualify the loan. Use one when the rent can support the loan and you want a repeatable approach for investing. DSCR loans are also a good match for LLC purchases.

In plain English, the choice usually comes down to this: who looks stronger on paper, the borrower or the property?

Final Takeaway for Loan Selection

Choose a bank statement loan when your deposits qualify you. Choose a DSCR loan when the rent qualifies the property.

FAQs

Can I use a DSCR loan if the property is vacant?

Yes. A DSCR loan can work for a vacant property because the loan is based on the property's income potential, not whether someone lives there right now.

Instead of using a current lease, lenders usually look at a market rent schedule or an appraisal report to estimate rental income. If that projected rent meets the required DSCR, the property can qualify.

Which loan is easier for a first-time investor?

It depends on your financial profile, but DSCR loans are often simpler for rental properties. They don't require personal income verification. Instead, the lender looks at whether the property's cash flow can cover the debt.

If you're self-employed and have strong, steady bank deposits, a bank statement loan may be easier to qualify for, especially if the property doesn't yet bring in enough rent.

What if my property's DSCR is below 1.00?

A DSCR below 1.00 means the property brings in less income than it needs to cover monthly debt service (PITIA).

Many lenders want to see 1.00 or higher. But that doesn't always shut the door. Some loan programs will still finance properties with a DSCR under 1.00.

In those cases, you may still qualify if you put more money down, show higher rental income, or use a different loan setup. These programs often come with tighter rules, like a higher credit score, a lower LTV, and smaller loan amounts.